Highlights

- Revised Stage 3 tax cuts are structured to provide greater relief to middle-income earners rather than concentrating benefits at the top end.

- Income between AUD 45,000 and AUD 135,000 is taxed at a flat 30%, reshaping take-home pay outcomes in FY26.

- Workers earning around the national average wage are expected to see annual tax savings exceeding AUD 1,500.

Australia’s Stage 3 tax cuts form part of a long-planned restructuring of the personal income tax system, originally legislated in 2018 and revised by the Federal Government in early 2024. The updated design aims to recalibrate tax relief toward low- and middle-income earners while maintaining progressivity within the system.

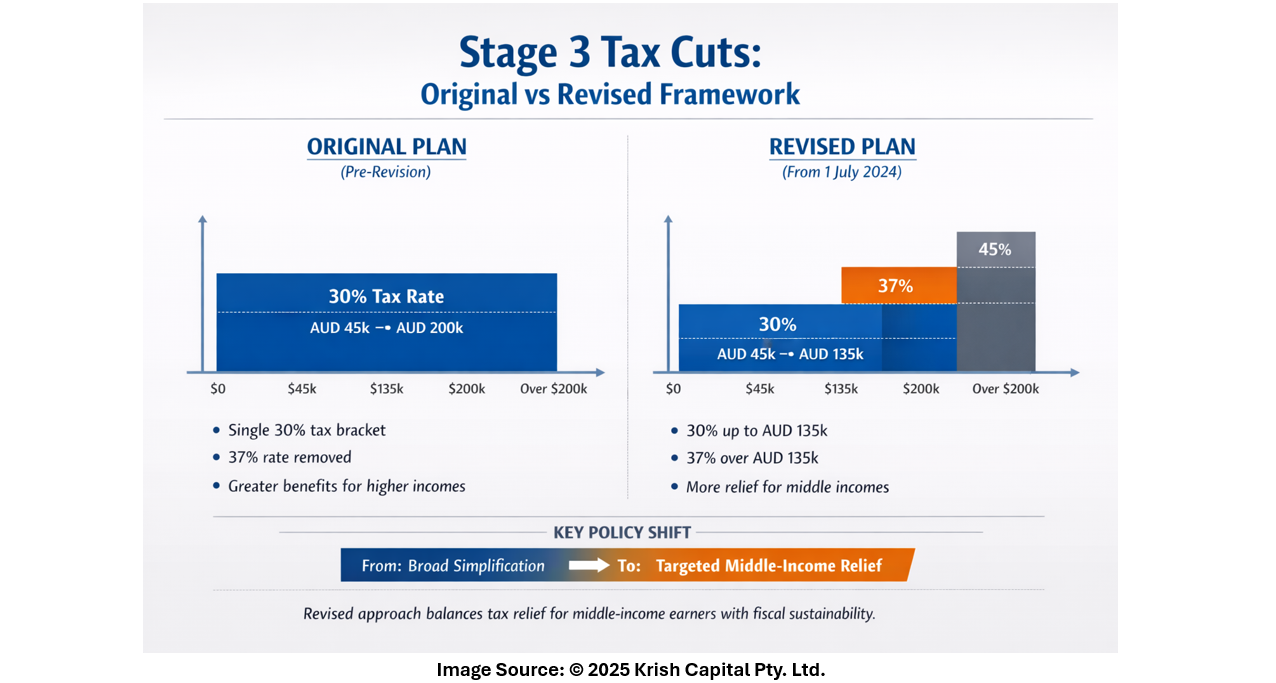

Under the revised structure, income up to AUD 18,200 remains tax-free, while income between AUD 18,201 and AUD 45,000 is taxed at 16%. Earnings from AUD 45,001 to AUD 135,000 are taxed at a flat 30% rate, with the 37% marginal tax rate applying between AUD 135,001 and AUD 190,000. Income above AUD 190,000 continues to attract the top marginal rate of 45%.

These changes were applied from 1 July 2024 and will therefore be fully reflected in individual tax outcomes during the 2025–26 financial year.

Who Benefits Most from the Changes

Middle-income earners—commonly defined as those earning between AUD 50,000 and AUD 130,000 annually—stand to benefit most from the revised tax settings. This group includes a significant portion of Australia’s workforce, particularly professionals, skilled trades, and dual-income households.

For an individual earning close to the average Australian wage of around AUD 73,000, the revised Stage 3 structure translates into tax savings of more than AUD 1,500 per year compared with previous tax scales. Those earning closer to AUD 100,000 may see annual savings exceeding AUD 2,000, improving net income outcomes amid ongoing cost-of-living pressures.

How the Revised Model Differs from the Original Plan

The original Stage 3 framework proposed a broad 30% tax bracket extending from AUD 45,000 to AUD 200,000, effectively removing the 37% marginal tax rate. The revised version reintroduces the 37% bracket above AUD 135,000, reducing the scale of benefits for higher-income earners while redistributing savings toward the middle of the income spectrum.

This adjustment reflects a policy trade-off between tax simplification and fiscal sustainability, ensuring that revenue impacts are moderated while still delivering relief to a wider base of taxpayers.

Why the Changes Matter in FY26

As the revised tax cuts flow through FY26, higher take-home pay is expected to support household consumption and improve financial resilience for middle-income Australians. Policymakers also argue that lower effective tax rates in this income range can support workforce participation and reduce the impact of bracket creep, where inflation erodes real wages while increasing tax liabilities.

Looking Ahead

While the revised Stage 3 tax cuts provide measurable benefits for middle-income earners, broader debate continues around long-term tax reform, revenue adequacy, and the balance between equity and efficiency in Australia’s tax system.

Disclaimer:

This article (“Article”) has been prepared by Kalkine Pty Limited (ABN 34 154 808 312) (Australian financial services licence number 425376) (“Kalkine”) and its related bodies corporate who are authorised to provide general financial product advice. Kalkine.com.au and its associated pages are published by Kalkine.

Any information/advice provided in this article is general in nature and does not take into account your objectives, financial situation or needs. You should therefore consider whether the information is appropriate for your objectives, financial situation and needs before acting upon it.

There may be a Product Disclosure Statement, Information Memorandum or other offer document (“Offer Document”) for the securities or other financial products referred to in Kalkine articles. You should obtain a copy of the Offer Document and consider it before making any decision about whether to acquire the security or financial product.

Kalkine strongly recommends that you seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) before acting on any advice/information in this Article or on the Kalkine website. Not all investments are appropriate for all people.

The information in this Article and on Kalkine website has been prepared from a wide variety of sources, which Kalkine, to the best of its knowledge and belief, considers accurate. Kalkine has made every effort to ensure the reliability of the information contained in its articles (including this Article), newsletters and websites. All information represents our views at the date of publication and may change without notice.

The information in this Article does not constitute an offer to sell securities or other financial products or a solicitation of an offer to buy securities or other financial products.

Kalkine does not issue, sell or deal in any financial products.

This Article may contain information on past performance of particular investments. Please note past performance is neither an indicator nor a guarantee of future performance.

To the extent permitted by law, and excluding any dishonesty or gross negligence by Kalkine, Kalkine disclaims and excludes all liability for any direct, indirect, implied, punitive, special, incidental or other consequential loss or damage arising from the use of or reliance on this Article, the Kalkine website and any information published on the Kalkine website without any warranties or representations by Kalkine to you. To the extent the law prohibits or limits this exclusion, Kalkine limits its liability to the resupply of services.

Please also read our Terms & Conditions and Financial Services Guide for further information.

Employees and/or associates of Kalkine and its related entities may hold interests in the securities or other financial products covered in this Article or on the Kalkine website. Any such employees and associates are required to comply with certain safeguards, procedures and disclosures as required by law.

Some of the images/music that may be used in the Article are copyright to their respective owner(s). Kalkine does not claim ownership of any of the pictures displayed/music used in the Article unless stated otherwise. The images/music that may be used in the Article are taken from various sources on the internet, including paid subscriptions or are believed to be in public domain. We have used reasonable efforts to accredit the source wherever it was indicated or was found to be necessary.

Kalkine Media Pty Ltd, an affiliate of Kalkine Pty Ltd, may have received, or be entitled to receive, financial consideration in connection with providing information about certain entity(s) covered on its website.

Copyright 2026 Krish Capital Pty. Ltd. (ABN 61629651510). All Rights Reserved. No part of this Article, or its content, may be reproduced in any form without our prior consent.

Please wait processing your request...

Please wait processing your request...