Highlights

- Employers pay Fringe Benefits Tax on non-cash benefits provided to employees and their associates.

- Employers self-assess FBT liability for the FBT year running from 1 April to 31 March.

- Employers calculate FBT using the grossed-up taxable value of fringe benefits.

- Employers apply a fixed 47% FBT rate to determine the final tax payable.

- Employers can claim income tax deductions and GST credits on eligible fringe benefits.

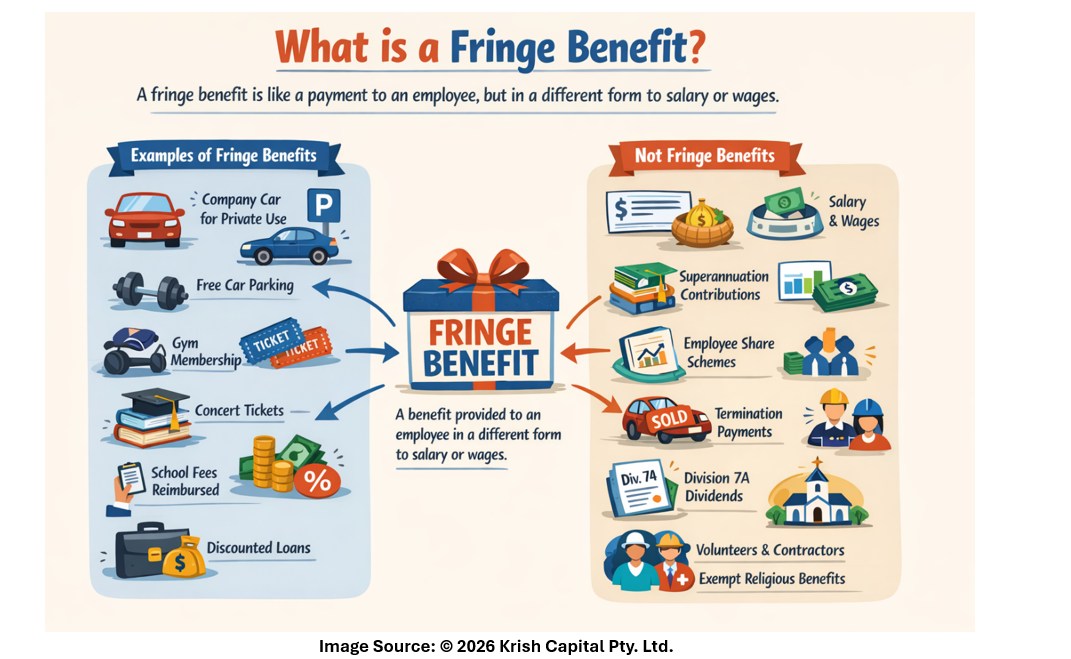

Fringe Benefits Tax (FBT) is a tax paid by employers on certain benefits provided to employees or to employees’ family members and associates. It applies to benefits delivered in a form other than salary or wages.

FBT operates separately from income tax and is calculated based on the taxable value of the fringe benefit. Employers must determine their FBT liability through self-assessment for each FBT year, which runs from 1 April to 31 March. If a liability exists, employers must lodge an FBT return and pay the amount owed.

Who Receives Fringe Benefits?

FBT applies to fringe benefits provided to employees and their related associates, including family members. The term employee covers a broad group for FBT purposes.

An employee includes:

• A current, future, or past employee

• A director of a company

• A beneficiary of a trust who works in the business

Sole traders and partners in partnerships are not considered employees. Benefits provided to themselves are not subject to FBT. Similarly, clients are not employees, and benefits provided to clients, including entertainment, are not subject to FBT.

Employer Bears the Responsibility

The employer pays Fringe Benefits Tax. This responsibility remains with the employer even if a third party provides the benefit under an arrangement with the employer.

Employers must calculate the FBT liability, prepare and lodge an FBT return, and ensure payment is made by the due date. The due date for lodging and paying FBT is generally 21 May.

Understanding the FBT Calculation

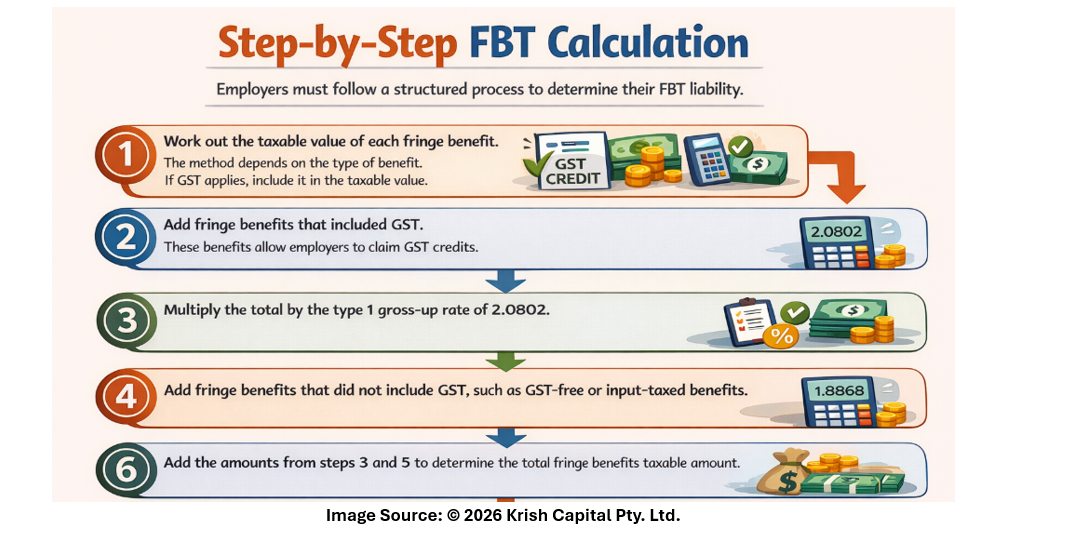

Employers calculate FBT by first working out the taxable value of the fringe benefits provided. The taxable value represents the cost of providing the benefit.

To determine the final FBT liability, employers must “gross up” the taxable value. Grossing up reflects the amount of salary an employee would have to earn at the highest marginal tax rate, including the Medicare levy, to purchase the benefit themselves. The employer then applies the FBT rate of 47% to the grossed-up value.

Example: Gym Membership Benefit

Jenni operates a consulting firm and provides her employee, Anton, with a gym membership costing $1,100, including $100 GST. The gym membership qualifies as a fringe benefit.

Jenni calculates the FBT liability as follows:

• Taxable value of the benefit: $1,100

• Gross-up rate for GST-inclusive benefit: 2.0802

• FBT rate: 47%

The calculation results in an FBT liability of $1,075.46. Jenni must prepare and lodge an annual FBT return and pay the liability. She may also need to calculate and report Anton’s reportable fringe benefits amount in his end-of-year payment information.

As the gym membership is subject to FBT, Jenni can claim an income tax deduction and GST credit for the cost of the membership and claim an income tax deduction for the FBT paid.

Deductions and GST Credits

Employers providing fringe benefits may claim tax deductions and GST credits related to those benefits.

Employers can claim:

• Income tax deductions and GST credits for the cost of providing fringe benefits

• Income tax deductions for the FBT paid

If GST credits can be claimed, the employer claims the GST-exclusive amount as an income tax deduction. If GST credits cannot be claimed, the employer claims the full cost as an income tax deduction.

Employer Compliance Requirements

Employers must self-assess their FBT liability, lodge an annual FBT return, and pay the amount owed by the due date. Employers must also determine whether reportable fringe benefits must be included in employee payment information.

FBT compliance requires employers to maintain records, correctly determine taxable values, and apply the correct gross-up rates and tax rate during the FBT year.

Fringe Benefits Tax requires employers to manage, calculate, and report tax on non-cash employee benefits through a structured self-assessment framework. While FBT strengthens tax fairness and transparency, its technical calculations and compliance obligations can increase administrative complexity for businesses, particularly smaller employers.

Please wait processing your request...

Please wait processing your request...