Franking credits are one of the most powerful — and often misunderstood — features of the Australian tax system. For investors who hold dividend-paying shares on the Australian Securities Exchange (ASX), franking credits can significantly increase total investment returns.

Australia’s dividend imputation system was designed to eliminate the problem of double taxation on company profits. Under this system, when a company pays corporate tax on its profits, shareholders receive a credit for the tax already paid.

This means:

- Investors may pay less tax on dividend income

- Some investors receive cash refunds from the ATO

- Fully franked dividend stocks can produce higher after-tax returns

For retirees, self-managed super funds (SMSFs), and income investors, franking credits are often a critical component of portfolio strategy.

In fact, many of Australia’s most popular dividend stocks — including major banks and resource companies — distribute billions of dollars in franking credits every year.

This comprehensive guide explains everything investors need to know about franking

credits, including:

- How franking credits work

- How they appear on tax returns

- The 45-day holding rule

- How refunds are paid

- Which investors benefit the most

- Strategies for maximizing franking credit income

Quick Answers: Franking Credits Explained

What are franking credits?

Franking credits are tax credits attached to dividends paid by Australian companies that have already paid corporate tax on their profits.

Why do franking credits exist?

They prevent double taxation, ensuring company profits are not taxed both at the corporate level and again in the hands of shareholders.

Who benefits the most from franking credits?

The biggest beneficiaries typically include:

- retirees

- low-income investors

- self-managed super funds

- dividend income investors

These investors can often receive refunds from the Australian Taxation Office (ATO).

What is the 45-day rule?

To claim franking credits, investors must generally hold shares for at least 45 days

(excluding purchase and sale days) to prove they bear economic risk.

The History of Franking Credits in Australia

The concept of franking credits was introduced in 1987 as part of major tax reforms.

Before that, Australia used a classical taxation system, which created a major problem.

Company profits were taxed twice:

- Once when the company paid corporate tax

- Again when shareholders paid personal income tax on dividends

This double taxation discouraged investment in dividend-paying companies.

To solve this, Australia introduced the dividend imputation system, allowing companies

to pass on tax credits to shareholders.

Key milestones in the evolution of franking credits

- 1987 - Dividend imputation system introduced

- 1997 - Holding period rule introduced

- 2000 - Excess franking credits became refundable

- 2019 - Proposed removal of refunds debated in federal

- election

The 2000 reform was particularly significant because it allowed cash refunds for excess franking credits. This dramatically increased the attractiveness of fully franked dividends for retirees and super funds.

How Franking Credits Work: Step-by-Step Explanation

To understand franking credits, investors must follow the profit journey from company earnings to shareholder income.

- Step 1: Company earns profit

An Australian company generates profit from operations.

Example: Company profit: $100

- Step 2: Company pays corporate tax

The corporate tax rate for most large Australian companies is 30%.

Corporate tax paid: $100 × 30% = $30 tax

After tax profit: $100 − $30 = $70

- Step 3: Company pays dividends

The company distributes the remaining profit as dividends.

Cash dividend paid: $70

- Step 4: Franking credit attached

Because the company already paid $30 in tax, shareholders receive a franking credit for

that amount.

Dividend statement: Cash dividend: $70, Franking credit: $30 Total taxable income: $100

How Franking Credits Appear in Tax Returns

When investors lodge their tax returns, they must declare:

- the cash dividend received

- the franking credit attached

This is known as grossing up the dividend.

Example calculation

- Dividend received: $70

- Franking credit: $30

- Total taxable income: $100

Scenario 1: Investor tax rate 30%, Tax owed: $100 × 30% = $30, Franking credit offset: $30, Final tax payable: $0

Scenario 2: Investor tax rate 45%, Tax owed: $100 × 45% = $45, Franking credit offset: $30, Final tax payable: $15

Scenario 3: Investor tax rate 0%, Tax owed: $0, Franking credit: $30, Refund from ATO: $30

Why Franking Credits Are Extremely Valuable

Franking credits can dramatically increase effective dividend yield.

For example: A stock with a 5% fully franked dividend yield can produce an effective grossed-up yield of about 7.14%.

Grossed-up yield formula

Grossed up dividend yield = Dividend yield ÷ (1 − corporate tax rate)

Example: 5% ÷ 0.70 = 7.14% gross yield

This is why many Australian investors prefer fully franked dividend stocks.

Fully Franked vs Partially Franked Dividends

Not all dividends come with full franking credits.

Companies may issue:

- fully franked dividends

- partially franked dividends

- unfranked dividends

Fully franked dividend

Company paid full corporate tax.

Example: Dividend = $70, Franking credit = $30, Partially franked dividend

Company paid only partial tax.

Example: Dividend = $70, Franking credit = $15, Unfranked dividend

Company paid no Australian corporate tax.

Common examples:

- foreign income

- trust distributions

- REIT dividends

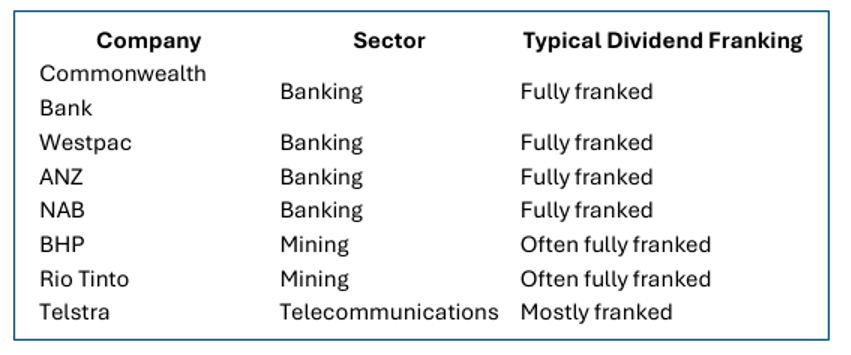

Companies That Commonly Pay Fully Franked Dividends

Some of the most famous fully franked dividend payers in Australia include:

These companies generate significant profits in Australia and therefore accumulate large franking credit balances.

The 45-Day Rule: Eligibility Requirement for Franking Credits

One of the most important conditions for claiming franking credits is the holding period rule. This rule prevents investors from buying shares just before the dividend and selling immediately after.

To claim franking credits:

- Shares must be held at risk for at least 45 days

Exclusions:

- Purchase day not counted

- Sale day not counted

The $5,000 Franking Credit Exemption

Small investors may qualify for an exemption. If total franking credits claimed are below $5,000, the holding rule may not apply. This simplifies tax compliance for retail investors.

Franking Credit Refunds Explained

One of the most unique features of Australia's tax system is the ability to receive cash refunds for excess franking credits. This occurs when the franking credit exceeds the investor’s tax liability.

Who receives refunds?

Common recipients include:

- retirees

- pensioners

- SMSFs in pension phase

- low-income earners

Why Retirees Love Franking Credits

Franking credits are extremely popular among retirees because they provide tax-efficient income.

A retiree holding high-dividend stocks may receive:

- cash dividends

- tax credit refunds

This can significantly boost retirement income.

Strategic Investing with Franking Credits

Many investors build portfolios specifically designed to maximize franking credits.

Common strategies include:

- investing in bank stocks

- holding dividend ETFs

- owning mature blue-chip companies

- focusing on high dividend yield sectors

High Franking Credit Sectors in Australia

Some sectors consistently produce strong franking credit flows.

- Banking sector

- Mining sector

- Telecommunications

Franking Credits vs International Dividends

One limitation of franking credits is that they apply only to Australian company tax. Foreign companies do not provide franking credits. This makes domestic dividend stocks particularly attractive for Australian income investors.

Risks of Chasing Franking Credits

Although franking credits are valuable, investors should avoid focusing solely on them.

Potential risks include:

- dividend cuts

- falling share prices

- sector concentration

- tax rule changes

- A balanced investment strategy is essential.

Key Takeaways

- Franking credits prevent double taxation of company profits

- Investors receive tax offsets attached to dividends

- Some investors receive cash refunds from the ATO

- Shares must generally be held at least 45 days

- Fully franked dividends increase effective investment yield

Franking credits remain one of the most powerful features of the Australian investment system.

Please wait processing your request...

Please wait processing your request...