Highlights

- The 15% global minimum tax remains the universal floor, with clearer implementation timelines and mechanisms.

- New OECD guidance refines deferred tax assets, domestic top-up rules, and information-sharing, increasing compliance complexity.

- Countries are implementing top-up taxes differently, phasing in the IIR and UTPR at varied speeds.

- Major powers’ positions (including the U.S.) and G7-level (Group of Seven) discussions continue to evolve, adding uncertainty to how “global” the reform becomes.

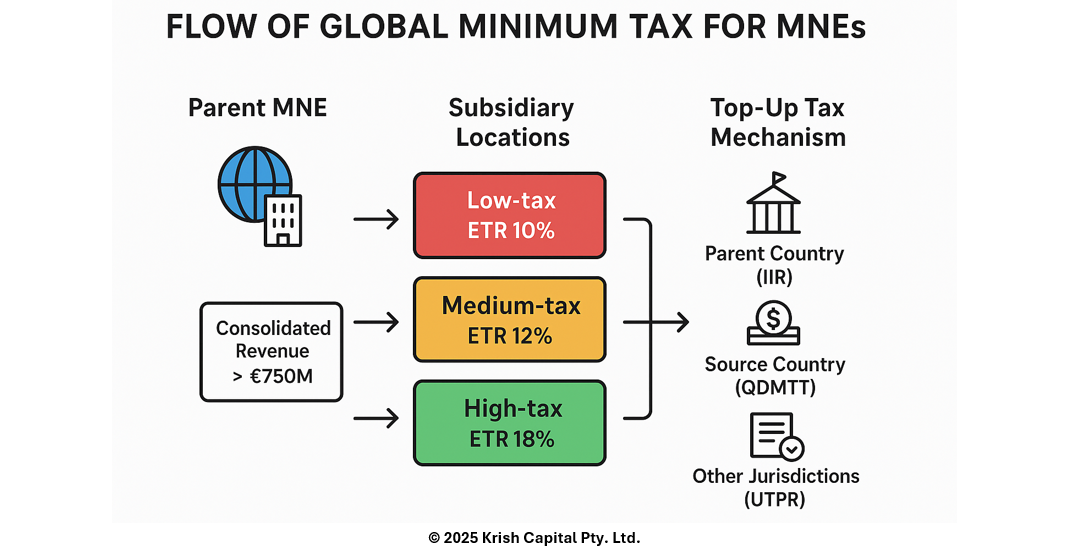

The global minimum tax remains a coordinated OECD/G20 effort to place a floor under corporate tax competition. Under the GloBE (Global Anti-Base Erosion) rules, MNEs (Multinational Enterprises) with revenues above EUR 750 million face a 15% minimum effective tax rate in each jurisdiction.

Implementation has become more concrete: the Income Inclusion Rule (IIR) began applying in many countries from January 2024, while the Undertaxed Profits Rule (UTPR) is rolling in more slowly, generally for fiscal years starting 2025. Several jurisdictions are also introducing Qualified Domestic Minimum Top-Up Taxes (QDMTTs) to ensure they collect the top-up themselves rather than leaving it to foreign authorities.

Three Key Reasons Behind This Historic Reform

Stopping Companies from Shuffling Profits Offshore

Updated OECD guidance has made the top-up system more precise, especially around calculating effective tax rates and “Covered Taxes.” New 2025 rules also clarify how deferred tax assets are treated, excluding certain deferred tax expenses from Covered Taxes under specified conditions.

No More Slashing Taxes to Win Business

The global minimum tax reduces incentives for countries to cut taxes aggressively. Whether top-up goes to the home country or the source country depends on whether the jurisdiction has implemented a QDMTT or relies on IIR/UTPR rules. OECD projections suggest that around 90% of in-scope MNEs will face the minimum rate in most jurisdictions by the end of 2025, even if implementation is uneven.

Making Sure Every Country Gets Its Fair Share

QDMTTs strengthen source countries’ ability to collect taxes where business activity actually occurs. OECD estimates suggest the global minimum tax could generate USD 150–200 billion per year in additional revenue for governments worldwide.

From Higher Taxes to Complex Compliance: What Firms Face

Low-tax jurisdictions are less attractive than before, especially where local QDMTTs neutralize tax holidays or very low nominal rates. Compliance demands have risen sharply: the OECD released a GloBE Information Return XML schema and finalized a multilateral framework for exchanging GloBE data.

Substance now plays a larger role. The substance-based income exclusion and safe-harbour rules mean that genuine activities — employees, tangible assets, and real operations — can shield some income from top-up obligations. At the same time, firms must run more sophisticated forecasts, as top-up outcomes vary depending on whether a jurisdiction applies to the IIR, QDMTT, or UTPR.

Overall, companies must track more granular data, including deferred taxes, tax credits, and cross-border allocations, especially given the new administrative guidance released in early 2025.

Will Tax Holidays Still Work?

Tax holidays still exist, but their value is diminishing. If the local tax rate drops too far below 15%, another jurisdiction may collect the top-up. Countries with QDMTTs can preserve investment incentives more effectively by ensuring the minimum tax is collected locally rather than abroad.

Companies must now model not only current tax savings but also how deferred tax positions reverse in future years, since the OECD’s recent guidance directly affects how temporary differences are treated under GloBE.

Who’s In, Who’s Out, and When It Kicks In

In scope: MNEs with consolidated revenue above EUR/USD 750 million.

Minimum rate: 15% globally.

In the works since:-

- IIR: widely effective from 2024

- UTPR: phased in for 2025 fiscal years

- QDMTT: expanding as many countries adopt domestic top-up taxes aligned with OECD rules

Strategies Multinationals Can Use to Navigate the New Tax Landscape

- Know Where You Stand: Recalculate ETRs for each jurisdiction and incorporate expected top-up liabilities.

- Maximize Substance: Strengthen real operations to benefit from exclusions and safe harbours.

- Forecast Multiple Scenarios: Model obligations under IIR, QDMTT, and UTPR pathways.

- Reassess Jurisdictions: Low-tax hubs may remain viable only when paired with strategic operational benefits.

- Prepare for Reporting: Build systems that can handle GIR requirements and detailed deferred-tax tracking.

- Engage Regulators: Many jurisdictions are still shaping domestic rules; early engagement can mitigate uncertainty.

A New Era in Global Corporate Taxation

The 15% global minimum tax marks a pivotal shift. With countries actively legislating, the OECD releasing dense administrative rules, and new reporting frameworks coming online, the reform is no longer theoretical. It limits profit shifting and harmful tax competition while increasing certainty — though at the cost of significantly more compliance. As implementation deepens through 2025 and beyond, multinationals must adapt strategy, structure, and reporting to operate effectively in this evolving global tax environment.

Please wait processing your request...

Please wait processing your request...