Highlights

- Australia has implemented the OECD/G20 Pillar Two Global Anti-Base Erosion (GloBE) Rules.

- The framework introduces a 15% global and domestic minimum tax for large multinational groups.

- Primary and subordinate legislation were enacted in December 2024.

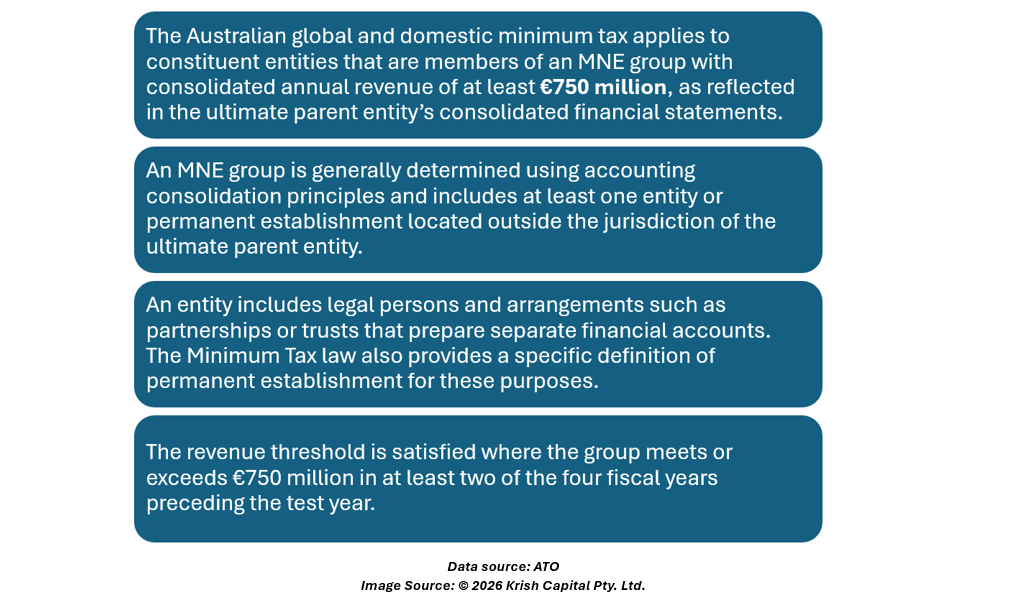

- The rules apply to multinational groups with consolidated revenue of at least €750 million.

Australia has implemented the Global Anti-Base Erosion Model Rules (GloBE Rules) through the introduction of a global and domestic minimum tax. These rules form part of the OECD/G20 Two-Pillar Solution, designed to address tax challenges arising from the digitalisation of the global economy. The framework ensures that multinational enterprise (MNE) groups are subject to a minimum effective tax rate of 15% in each jurisdiction in which they operate.

Legislative Framework

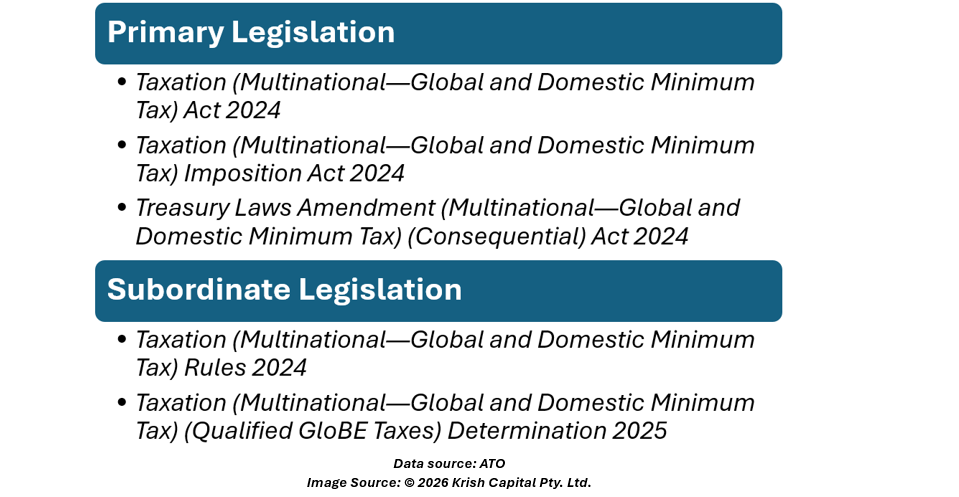

Primary legislation implementing the GloBE Rules in Australia received royal assent on 10 December 2024. This legislation also includes consequential amendments that integrate the administration of top-up tax within Australia’s existing tax administration framework, consistent with the GloBE Rules.

On 23 December 2024, subordinate legislation containing detailed computational and operational rules was registered as a legislative instrument and is now in force.

Components of the Global and Domestic Minimum Tax

Australia’s minimum tax framework comprises both global and domestic elements.

Global Minimum Tax

The global minimum tax operates through two interlocking rules:

- Income Inclusion Rule (IIR):

This primary rule allows Australia to impose top-up tax on multinational parent entities located in Australia where the group’s effective tax rate in another jurisdiction is below 15%. - Undertaxed Profits Rule (UTPR):

This backstop rule enables Australia to apply top-up tax to Australian constituent entities where low-taxed profits are not brought into charge under an IIR.

Domestic Minimum Tax

Australia has also introduced a domestic minimum tax that operates consistently with the GloBE Rules. This measure allows Australia to claim priority taxing rights over low-taxed profits arising in Australia, ahead of the application of the IIR and UTPR.

Australian Pillar Two Legislation

Australia’s global and domestic minimum tax is implemented through the following legislation, collectively referred to as the Minimum Tax law.

The Minimum Tax law is to be interpreted consistently with OECD guidance materials, including the GloBE Model Rules, commentary, and agreed administrative guidance.

Scope of Application

Domestic Minimum Tax Coverage

The domestic minimum tax broadly applies to Australian constituent entities within MNE groups that are subject to the global minimum tax framework.

Excluded Entities

Certain entities are excluded from the operation of the Australian global and domestic minimum tax. These GloBE excluded entities include, among others:

- Government entities

- International organisations

- Non-profit organisations

- Certain service entities

- Pension funds

- Ultimate parent entities that are investment funds or real estate investment vehicles

A subsidiary of an excluded entity is not automatically excluded and must be assessed independently. Entities must retain records supporting their classification as excluded entities.

Consequences of Exclusion

Where an entity is classified as a GloBE excluded entity, it:

- Has no obligation to lodge returns under the global and domestic minimum tax regime

- Is not liable for top-up tax under the IIR, UTPR, or domestic minimum tax

If an MNE group consists entirely of excluded entities, the group is fully outside the scope of the regime. Where a group includes both excluded and non-excluded entities, certain obligations may still apply, including revenue inclusion for threshold testing and disclosures in the GloBE Information Return.

Operation of the Rules

Top-up tax applies where an entity has an IIR, domestic minimum tax, or UTPR liability. The calculation broadly involves three steps:

- Effective Tax Rate (ETR) Calculation:

Net income and attributable taxes of constituent entities within a jurisdiction are determined using financial accounting data with GloBE-specific adjustments. - Top-Up Tax Determination:

Where a jurisdiction’s ETR is below 15%, top-up tax is calculated based on the difference between the minimum rate and the actual ETR. - Allocation of Liability:

The jurisdictional top-up tax is allocated to relevant entities according to rules set out in the Australian Minimum Tax Rules. Domestic top-up tax applies where Australia’s ETR is below 15%, while IIR or UTPR may apply for low-taxed foreign jurisdictions.

Top-up tax may also arise in respect of certain joint arrangements and stateless constituent entities.

Special Rules and Entity Classification

Special rules apply to particular entities, groups, and arrangements to account for differing tax treatments and structures. These may affect jurisdictional location, ETR calculation, income and tax attribution, and allocation of top-up tax liability.

These rules can apply to permanent establishments, flow-through entities, joint ventures, investment entities, minority-owned entities, and multi-parented groups.

Please wait processing your request...

Please wait processing your request...