Highlights

- Lithium prices surge after Zimbabwe suspends exports, raising supply concerns.

- Spodumene price recovery boosts sentiment among ASX-listed lithium producers.

- EV adoption and energy storage continue to drive long-term lithium demand.

- ASX lithium leaders maintain strong balance sheets and operational performance.

- Strategic joint ventures and resource optimisation underpin growth prospects.

Lithium prices have surged following the suspension of exports by Zimbabwe, one of the world’s leading producers of the battery material, raising concerns over a potential supply crunch amid booming demand. Zimbabwe, which contributed around 10% of global lithium production last year and is a major supplier to China, has halted exports of lithium concentrate to encourage domestic processing and curb illegal shipments. While Chinese lithium refineries have secured stockpiles expected to last until mid-to-late April, supply is likely to tighten from May, as the average shipping time from Zimbabwe to China is approximately two months, according to Mysteel.

The rebound in spodumene prices has further bolstered sentiment among ASX-listed lithium producers. Growth in electric vehicle adoption and energy storage continues to underpin long-term demand for lithium, while tightening supply conditions and rising long-term price forecasts are driving renewed investor interest.

Market Forecast and Investment Insights

According to Reuters, Morgan Stanley projects a deficit of 80,000 metric tons of lithium carbonate equivalent (LCE) in 2026, while UBS estimates a smaller deficit of 22,000 tons, compared with an anticipated surplus of 61,000 tons in 2025. Three other Chinese analysts expect the lithium market to post a narrower surplus this year.

Global lithium demand is forecast to increase by 17% to 30% in 2026, while supply is expected to rise by 19% to 34%, based on estimates from four unnamed analysts who are not authorised to speak to the media.

Analysts predict lithium prices will range between 80,000 and 200,000 yuan ($11,432–$28,580) per ton in 2026, up from 58,400–134,500 yuan per ton in 2025.

In this context, Australian lithium miners are gaining attention not only for their production but also for strategic asset management, operational efficiency, and downstream exposure.

Leading ASX Lithium Producers

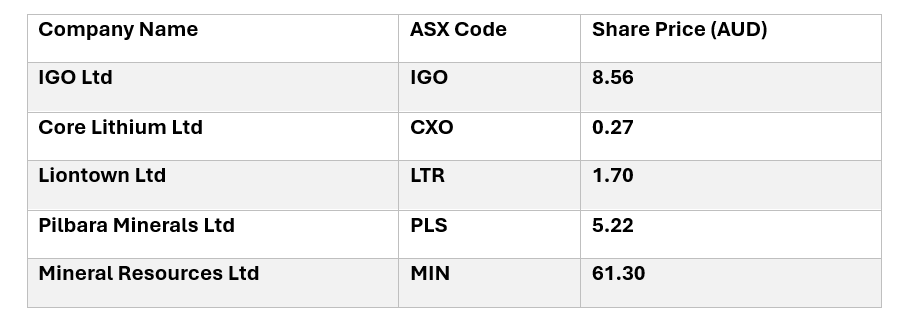

Data source: ASX as of 27 February 2026

Pilbara Minerals Ltd (ASX:PLS) leads as one of Australia’s largest independent hard-rock lithium producers, operating the high-grade Pilgangoora lithium operation. The company recently signed a supply deal with a Chinese battery maker. Pilbara Minerals maintains a strong balance sheet with ~A$1B cash, providing flexibility for investment, returns, or patient growth. Its FY26 interim half-year results included 446.0kt in sales at US$965/t, underlying EBITDA up 40% versus H1 FY25, and NPAT of A$33M.

Liontown Resources Ltd (ASX:LTR) operates the Kathleen Valley Lithium Operation in Western Australia, supplying foundation offtake partners and strategic spot market sales. The project hosts 150Mt @ 1.3% Li₂O and 130ppm Ta₂O₅ and is located 375 km from Kalgoorlie. Fully transitioned to underground operations, Kathleen Valley achieved a 148% increase in underground production YTD FY25.

Core Lithium Ltd (ASX:CXO) is advancing the Finniss Lithium Operation in the Northern Territory, a multi-mine, low-cost hard-rock project with modern processing facilities. The company progressed its Finniss Restart Plan, supported by technical, design, and engineering work. An updated Carlton Ore Reserve was declared in September 2025, with an Exploration Target of 1.2–1.8Mt at 1.2–1.4% Li₂O, complementing an existing Mineral Resource of 48.5Mt @ 1.26% Li₂O and additional BP33 and Blackbeard exploration targets.

Mineral Resources Ltd (ASX:MIN) reported record first-half results for FY26, with revenue of A$3.1B and EBITDA of A$1.2B. Free cash flow reached A$293M after A$587M in capital expenditure, strengthening liquidity to A$1.4B and reducing net debt by A$471M to A$4.9B. A binding agreement with POSCO Holdings to acquire 30% of Wodgina and Mt Marion JVs for US$765M is expected to accelerate deleveraging and support ongoing operations.

IGO Ltd (ASX:IGO) maintains exposure to lithium through its 24.99% stake in the Greenbushes lithium operation, achieving a 61% EBITDA margin in 1H26. With ~A$300M in cash, IGO is focused on optimising the life of mine at Greenbushes and generating value from strategic exploration targets.

Other notable ASX lithium and spodumene names include Lepidico Ltd (ASX:LPD), Global Lithium Resources Ltd (ASX:GL1), Power Minerals Ltd (ASX:PNN), Patagonia Lithium Ltd (ASX: PL3), and Premier1 Lithium Ltd (ASX:PLC), representing smaller or exploration-stage projects with spodumene potential. These companies are frequently highlighted by market brokers and investment analysts for growth opportunities.

Rising lithium prices, supply constraints, and strong long-term demand from EVs and energy storage are driving renewed investor focus on ASX-listed lithium producers. Companies such as Pilbara Minerals, Liontown, Core Lithium, Mineral Resources, and IGO are benefiting from high-grade spodumene operations, strategic joint ventures, and strong operational performance. Smaller exploration-stage companies provide additional growth potential, making the Australian lithium sector a key area for market attention.

FAQs

Q1: What is driving spodumene price recovery?

Benchmark prices have rebounded due to supply tightening, rising demand from EVs and energy storage, and renewed investor interest in lithium projects.

Q2: How does geographic concentration affect critical minerals?

Between 2020 and 2024, the top three refining nations captured 86% of production for key energy minerals, highlighting concentration risk in asset supply chains.

Q3: Why are joint ventures important for ASX lithium companies?

Joint ventures such as Wodgina, Mt Marion, and Greenbushes provide strategic production exposure and access to long-term lithium supply.

Q4: What are the main challenges for lithium producers?

High operating expenses, extended timelines from discovery to production, and evolving global demand pressures can impact financial performance.

Please wait processing your request...

Please wait processing your request...