Highlights

- Inflation reduces the purchasing power of money held in savings over time.

- The Consumer Price Index (CPI) is the most widely used measure of inflation.

- Core inflation provides insights into long-term price trends by excluding volatile items.

- Keeping inflation within a 2–3 per cent target helps protect savings and supports economic stability.

Inflation refers to the rise in prices for goods and services over a specified period. It can be measured broadly, such as the general increase in the cost of living, or narrowly, for specific goods or services like food, personal care, or housing. Regardless of the method used, inflation reflects the extent to which the cost of a particular set of items has increased, usually over a year.

How Inflation Influences Daily Life

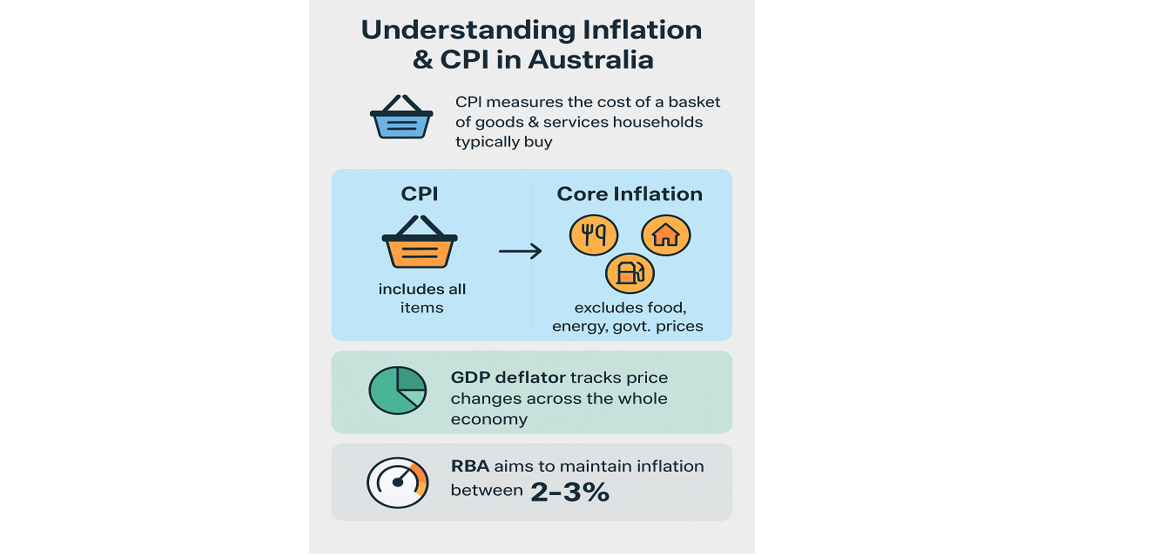

Household living costs depend on the prices of a wide variety of goods and services, along with the proportion each category represents in a typical budget. To track these changes, government agencies conduct surveys and establish a “basket” of commonly purchased items. Tracking the cost of this basket over time forms the basis of the Consumer Price Index (CPI).

The Connection Between Inflation and Savings

Savings are funds set aside for future use. As inflation rises, the purchasing power of saved money declines because it can buy fewer goods and services. For instance, if inflation is 3 per cent, an item costing AUD 100 today would cost AUD 103 next year. Unless savings earn a return higher than the inflation rate, their real value diminishes.

This is particularly relevant for long-term savings, such as retirement funds. Even moderate inflation, compounded over the years, can significantly reduce the effective value of savings if steps are not taken to protect against it.

Measuring Inflation

The CPI is the most widely recognised measure of consumer inflation. It monitors the cost of a basket of goods and services that households typically purchase, including housing, transport, food, and healthcare. Comparing the current cost of this basket to a base year provides the percentage change, which represents consumer price inflation.

To better capture persistent trends, core inflation excludes more volatile items like food and energy, as well as government-regulated prices. Broader measures, such as the GDP deflator, track price changes across the entire economy, providing a more comprehensive view.

Inflation Targets and Policy

In Australia, the Reserve Bank, in consultation with the Government, aims to keep annual consumer price inflation between 2 and 3 per cent. This target seeks to prevent savings from losing value due to high inflation, while also avoiding deflation, which can discourage spending and investment.

A predictable inflation environment supports the preservation of money’s value over time and aids in planning for households, businesses, and governments alike.

Long-Term Impact on Savings

Even moderate inflation can have a noticeable effect over the long term. For example, AUD 10,000 held in savings would only have the purchasing power of approximately AUD 8,200 after ten years at a 2 per cent annual inflation rate if no interest is earned. This demonstrates why monitoring inflation is crucial for savers and policymakers.

Conclusion

Inflation is a key factor in determining the future value of savings. It gradually reduces purchasing power unless returns on savings exceed the rate of inflation. Tracking indicators such as the CPI and core inflation helps in understanding these effects. Maintaining inflation within the 2–3 per cent target assists in protecting savings and contributes to a more predictable economic environment.

Disclaimer:

This article (“Article”) has been prepared by Kalkine Pty Limited (ABN 34 154 808 312) (Australian financial services licence number 425376) (“Kalkine”) and its related bodies corporate who are authorised to provide general financial product advice. Kalkine.com.au and its associated pages are published by Kalkine.

Any information/advice provided in this article is general in nature and does not take into account your objectives, financial situation or needs. You should therefore consider whether the information is appropriate for your objectives, financial situation and needs before acting upon it.

There may be a Product Disclosure Statement, Information Memorandum or other offer document (“Offer Document”) for the securities or other financial products referred to in Kalkine articles. You should obtain a copy of the Offer Document and consider it before making any decision about whether to acquire the security or financial product.

Kalkine strongly recommends that you seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) before acting on any advice/information in this Article or on the Kalkine website. Not all investments are appropriate for all people.

The information in this Article and on Kalkine website has been prepared from a wide variety of sources, which Kalkine, to the best of its knowledge and belief, considers accurate. Kalkine has made every effort to ensure the reliability of the information contained in its articles (including this Article), newsletters and websites. All information represents our views at the date of publication and may change without notice.

The information in this Article does not constitute an offer to sell securities or other financial products or a solicitation of an offer to buy securities or other financial products.

Kalkine does not issue, sell or deal in any financial products.

This Article may contain information on past performance of particular investments. Please note past performance is neither an indicator nor a guarantee of future performance.

To the extent permitted by law, and excluding any dishonesty or gross negligence by Kalkine, Kalkine disclaims and excludes all liability for any direct, indirect, implied, punitive, special, incidental or other consequential loss or damage arising from the use of or reliance on this Article, the Kalkine website and any information published on the Kalkine website without any warranties or representations by Kalkine to you. To the extent the law prohibits or limits this exclusion, Kalkine limits its liability to the resupply of services.

Please also read our Terms & Conditions and Financial Services Guide for further information.

Employees and/or associates of Kalkine and its related entities may hold interests in the securities or other financial products covered in this Article or on the Kalkine website. Any such employees and associates are required to comply with certain safeguards, procedures and disclosures as required by law.

Some of the images/music that may be used in the Article are copyright to their respective owner(s). Kalkine does not claim ownership of any of the pictures displayed/music used in the Article unless stated otherwise. The images/music that may be used in the Article are taken from various sources on the internet, including paid subscriptions or are believed to be in public domain. We have used reasonable efforts to accredit the source wherever it was indicated or was found to be necessary.

Kalkine Media Pty Ltd, an affiliate of Kalkine Pty Ltd, may have received, or be entitled to receive, financial consideration in connection with providing information about certain entity(s) covered on its website.

Copyright 2026 Krish Capital Pty. Ltd. (ABN 61629651510). All Rights Reserved. No part of this Article, or its content, may be reproduced in any form without our prior consent.

_10_01_2025_11_14_31_245252.jpg)

_02_19_2026_11_50_21_592067.png)

_02_11_2026_07_58_30_526403.png)

Please wait processing your request...

Please wait processing your request...