Highlights

- Buying a home for comfort and buying property for returns require completely different decision frameworks.

- Emotional value often masks the true cost of ownership and lowers real investment performance.

- Yield, capital growth, and liquidity—not sentiment—determine an investment’s success.

- Separating lifestyle goals from financial goals leads to smarter property decisions.

For generations, property has symbolised safety, status, and long-term wealth. But the same house cannot always serve two masters. A home is first a place of shelter—an emotional anchor tied to family, stability, and personal identity. An investment property, on the other hand, is a financial instrument that must be judged by numbers, not feelings. Confusing these roles often leads to overpaying, underperforming assets, and misplaced expectations.

Understanding the difference between buying for lifestyle and buying for returns is the first step toward making smarter real estate decisions.

Property as Shelter: The Emotional Premium

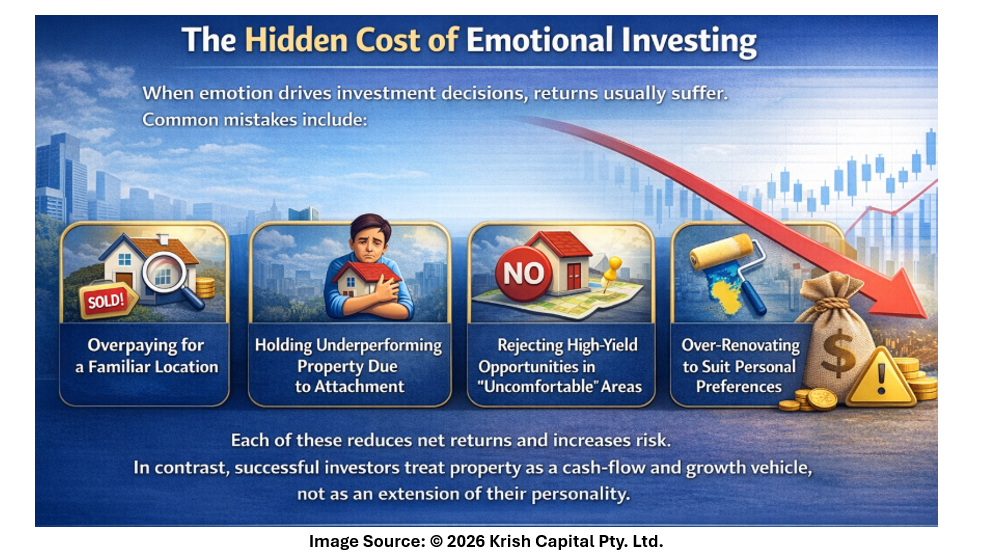

When purchasing a primary residence, logic often takes a back seat. Buyers prioritise good schools, proximity to work, neighbourhood familiarity, interior aesthetics, and even sentimental attachment to a location.

These factors are valid—but they come at a cost:

- Paying extra for a “dream home” in a premium suburb

- Choosing larger spaces than financially optimal

- Investing heavily in interiors and renovations that don’t increase resale value

From a financial perspective, many of these decisions generate consumption value, not investment return. The comfort, pride, and sense of belonging are real—but they are not measurable in yield or capital appreciation.

In simple terms, a self-occupied home behaves more like a lifestyle expense than a high-performing asset.

The most profitable investment properties are often not the ones people want to live in. They may be:

- In emerging or less glamorous locations

- Smaller and more functional

- Chosen for rental demand rather than personal taste

This is where investors struggle—because emotionally, they want to “like” the property. Financially, that preference is irrelevant.

Opportunity Cost: The Silent Wealth Killer

Money locked into a self-occupied home often delivers low or non-existent income returns. The same capital, if allocated differently, could generate:

- Rental income from higher-yield locations

- Diversified market investments

- Greater liquidity for future opportunities

This doesn’t mean owning a home is wrong—it means its primary return is emotional security, not financial performance.

Striking the Right Balance

Striking the Right Balance means recognising that the goal is not to choose between lifestyle and wealth creation, but to clearly separate the two. Your home should be optimised for affordability, stability, and long-term comfort, with the understanding that its primary return is emotional security rather than financial gain. Investment properties, in contrast, must be approached with complete objectivity—setting aside personal taste and focusing purely on data, rental demand, growth prospects, and overall returns. When each purchase is guided by its true purpose, you avoid overpaying for sentiment, make more disciplined financial decisions, and allow both your living space and your investments to perform successfully in their own distinct roles.

Conclusion: Redefining What “Return” Means

A home that gives peace of mind, stability, and happiness is delivering a powerful return—just not a financial one. An investment property that produces strong cash flow and capital growth may never feel emotionally satisfying, but it builds wealth. The mistake is expecting one property to do both.

When buyers clearly separate shelter decisions from investment decisions, they gain clarity, avoid overpaying, and create a more balanced and effective long-term financial strategy.

Disclaimer:

This article (“Article”) has been prepared by Kalkine Pty Limited (ABN 34 154 808 312) (Australian financial services licence number 425376) (“Kalkine”) and its related bodies corporate who are authorised to provide general financial product advice. Kalkine.com.au and its associated pages are published by Kalkine.

Any information/advice provided in this article is general in nature and does not take into account your objectives, financial situation or needs. You should therefore consider whether the information is appropriate for your objectives, financial situation and needs before acting upon it.

There may be a Product Disclosure Statement, Information Memorandum or other offer document (“Offer Document”) for the securities or other financial products referred to in Kalkine articles. You should obtain a copy of the Offer Document and consider it before making any decision about whether to acquire the security or financial product.

Kalkine strongly recommends that you seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) before acting on any advice/information in this Article or on the Kalkine website. Not all investments are appropriate for all people.

The information in this Article and on Kalkine website has been prepared from a wide variety of sources, which Kalkine, to the best of its knowledge and belief, considers accurate. Kalkine has made every effort to ensure the reliability of the information contained in its articles (including this Article), newsletters and websites. All information represents our views at the date of publication and may change without notice.

The information in this Article does not constitute an offer to sell securities or other financial products or a solicitation of an offer to buy securities or other financial products.

Kalkine does not issue, sell or deal in any financial products.

This Article may contain information on past performance of particular investments. Please note past performance is neither an indicator nor a guarantee of future performance.

To the extent permitted by law, and excluding any dishonesty or gross negligence by Kalkine, Kalkine disclaims and excludes all liability for any direct, indirect, implied, punitive, special, incidental or other consequential loss or damage arising from the use of or reliance on this Article, the Kalkine website and any information published on the Kalkine website without any warranties or representations by Kalkine to you. To the extent the law prohibits or limits this exclusion, Kalkine limits its liability to the resupply of services.

Please also read our Terms & Conditions and Financial Services Guide for further information.

Employees and/or associates of Kalkine and its related entities may hold interests in the securities or other financial products covered in this Article or on the Kalkine website. Any such employees and associates are required to comply with certain safeguards, procedures and disclosures as required by law.

Some of the images/music that may be used in the Article are copyright to their respective owner(s). Kalkine does not claim ownership of any of the pictures displayed/music used in the Article unless stated otherwise. The images/music that may be used in the Article are taken from various sources on the internet, including paid subscriptions or are believed to be in public domain. We have used reasonable efforts to accredit the source wherever it was indicated or was found to be necessary.

Kalkine Media Pty Ltd, an affiliate of Kalkine Pty Ltd, may have received, or be entitled to receive, financial consideration in connection with providing information about certain entity(s) covered on its website.

Copyright 2026 Krish Capital Pty. Ltd. (ABN 61629651510). All Rights Reserved. No part of this Article, or its content, may be reproduced in any form without our prior consent.

_02_19_2026_11_50_21_592067.png)

_02_11_2026_07_58_30_526403.png)

Please wait processing your request...

Please wait processing your request...