Highlights

- Not all debt is bad, understanding the difference between good debt and bad debt can change how you borrow.

- Choosing between the snowball and avalanche repayment strategies depends on your personality and financial goals.

- Paying only the minimum on credit cards is risky: high interest can make debt spiral.

- Boosting your credit score involves managing payments, utilization, and credit history thoughtfully.

Debt is a double-edged sword. If used smartly, it can be a powerful tool. But left unchecked, it can lead you into stress, financial traps, and long-term problems. Here, we’ll break down what “good” vs “bad” debt means, how to pay off debt fast, common credit card mistakes, how interest rates really work, and practical ways to improve your credit score.

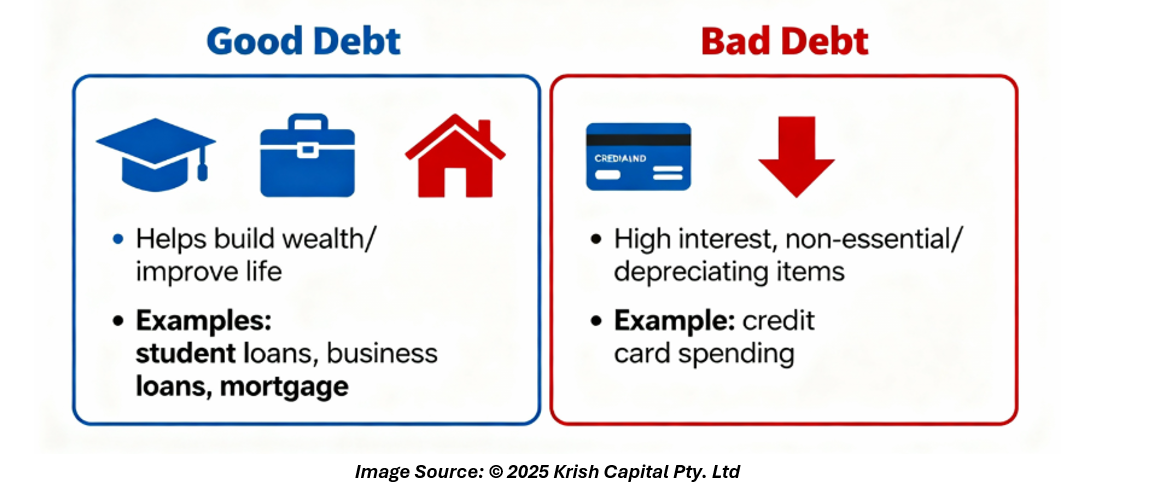

Good Debt vs. Bad Debt

First, not all debt is evil. Some loans can actually help you build wealth or improve your life. This is often called good debt. Good debt is typically used for things that increase in value or generate income — such as taking a student loan to get an education, borrowing to start a business, or taking a mortgage to buy a home.

On the flip side, bad debt usually involves high interest and purchases that don’t help you grow financially. Think of credit card balances used for non-essential spending, or loans for depreciating items.

If a loan doesn’t help you build anything — or worse, drains your cash — it’s likely bad debt.

How to Pay Off Debt Fast: Snowball vs. Avalanche

Having a strategy to pay off debt can make all the difference. Two of the most popular approaches are the snowball method and the avalanche method.

- Snowball Method

- List your debts from smallest balance to largest.

- Pay minimums on all except the smallest one; put all your extra money into clearing that first.

- Once the smallest is paid off, roll over its payment amount toward the next smallest. It feels like a snowball growing as you go.

- Why choose it? It gives you quick wins, which can be motivating.

- Avalanche Method

- Order your debts by highest interest rate to lowest.

- Pay the minimum on all debts but focus all additional money on the one with the highest interest.

- When the highest-rate debt is done, move to the next one, while continuing the pattern.

- Why choose it? It’s the most cost-efficient — you save the most on interest over time.

Both strategies help; the best one is the one you’ll stick with reliably.

Credit Card Mistakes to Avoid

Credit cards can quickly become a debt trap if you’re not careful. Here are some common pitfalls:

- Paying only the minimum: Credit card companies calculate interest daily, and when you pay just the minimum, the balance can linger for years and cost a lot more.

- Using credit for lifestyle purchases: Charging non-essential things like vacations or luxury goods without a plan to pay them off can turn into bad debt.

- Ignoring high APRs: If your card’s interest rate is very high, the cost of carrying a balance may outweigh any benefit of immediate spending.

Understanding Interest Rates

Interest rates are how lenders make money — and how debt can grow dangerously.

- Credit card rates (APR) are usually quite high compared to secured loans.

- Some rates are fixed, others are variable, which means they can go up or down.

- The longer you carry a balance, the more you pay in interest, especially if you're only making minimum payments.

Understanding how your interest works helps you decide which debt to prioritize and why paying more than the minimum is often critical.

How to Improve Your Credit Score

A good credit score can save you thousands by getting you lower rates. Here are simple, practical ways to make it better:

- Pay on time, every time

Your payment history often has the biggest impact on your score. - Keep your credit utilization low

This is how much of your available credit you're using. Try to stay below 30%; lower is better. - Maintain old accounts

The age of your credit history matters — older cards help your score. - Be careful with new credit applications

Opening many new accounts in a short time can hurt your score. - A mix of credit types helps

Having a mix like a credit card + a small loan can be beneficial.

Avoiding Debt Traps

Debt traps are situations where you’re borrowing more just to stay afloat:

- Avoid payday loans or very high-interest short-term loans, which can spiral.

- Don’t treat credit as “free money”; always have a repayment plan.

- If you’re overwhelmed, consider talking to a credit counsellor or using a debt management plan before things worsen.

In Summary

Debt isn’t inherently bad — when used wisely, it can support your goals. But bad debt can drain your finances and create unnecessary stress. To stay on top, know whether your debt is good or bad, so you can prioritize what truly matters. Pick a repayment method that realistically fits your lifestyle — the snowball method for quick motivation or the avalanche method for long-term savings. Avoid risky credit card habits such as carrying high balances or paying only the minimum, and make sure you clearly understand how interest rates work, so you’re aware of the real cost of borrowing. At the same time, actively work on improving your credit score through timely payments, responsible usage, and mindful borrowing habits.

With discipline, a strategy, and some financial awareness, you can turn debt into something manageable — or even productive.

_02_19_2026_11_50_21_592067.png)

_02_11_2026_07_58_30_526403.png)

Please wait processing your request...

Please wait processing your request...