Image source: © 2025 Krish Capital Pty.Ltd

Highlights

- Division 293 tax applies when combined income and concessional contributions exceed AUD 250,000.

- The tax is calculated at 15% of taxable super contributions or the excess over the threshold.

- One-off income events may cause Division 293 liability for a single financial year.

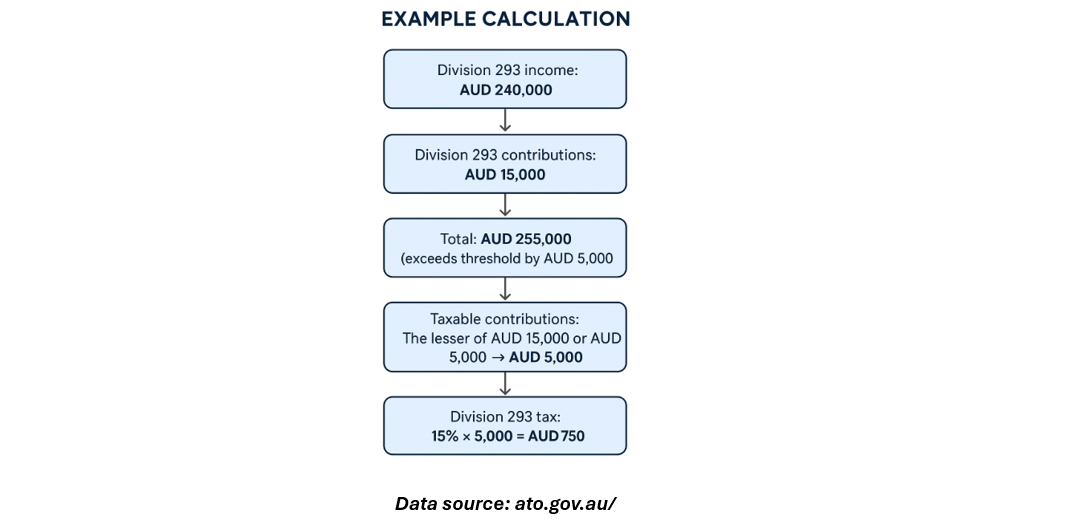

Division 293 tax is an additional tax that reduces the concessional treatment of superannuation contributions for high-income earners. It applies when the sum of an individual’s Division 293 income and concessional contributions exceeds AUD 250,000 in a financial year. The tax is charged at 15% of either the amount above the threshold or the taxable super contributions, whichever is lower.

Identifying Liability

The Australian Taxation Office (ATO) issues a Division 293 notice once both the individual’s tax return and their superannuation contribution data have been received.

- If lodging a tax return using myTax, the notice is delivered to the myGov inbox.

- Taxpayers who prefer their tax agent to receive the notice must update their communication preferences.

- A reminder is provided when preparing the tax return if the reported income suggests potential Division 293 liability.

Calculating Division 293 Tax

The assessment uses:

- Division 293 income: Determined from the tax return data.

- Division 293 super contributions: Reported by the super fund.

If there are multiple funds, late reporting by one fund may lead to an amended Division 293 assessment.

Understanding Division 293 Income

Division 293 income is calculated similarly to the income used for the Medicare Levy Surcharge, excluding reportable super contributions. Components include:

Impact of One-Off Events

Division 293 tax may apply for only one financial year due to exceptional income events. Examples include:

- Receiving an eligible termination payment

- Realising a significant capital gain

- Temporary increases in income

These events can raise an individual’s income above the AUD 250,000 threshold even if they typically fall below it.

Division 293 Super Contributions

The contributions counted include concessional contributions such as:

- Employer contributions

- Superannuation Guarantee contributions

- Salary sacrifice contributions

- Deductible personal contributions

If carried-forward concessional cap amounts are used, they are also included for Division 293 purposes.

Taxable Super Contributions

Taxable super contributions are the lower of the Division 293 super contributions and the amount exceeding the AUD 250,000 threshold. This ensures the additional tax only applies to the relevant portion of contributions.

Division 293 tax is an additional 15% tax on concessional super contributions for high-income Australians whose combined income and contributions exceed AUD 250,000 in a financial year. Calculated on the lesser of the excess over the threshold or total contributions, it applies even for one-off income events. While necessary to maintain fairness in super tax concessions, the tax can feel penal for those with temporary income spikes, highlighting the need for careful contribution planning.

_02_19_2026_11_50_21_592067.png)

_02_11_2026_07_58_30_526403.png)

Please wait processing your request...

Please wait processing your request...