Highlights

- Insurance safeguards assets by reducing financial shocks and aiding recovery after unforeseen events.

- Understanding coverage, exclusions, and policy limits is critical to avoid underprotection.

- Effective insurance requires active management, regular review, and integration with broader risk strategies.

In a climate of economic uncertainty and increasing environmental risks, protecting personal and business assets has become a top financial priority. Insurance provides a structured way to manage the financial impact of unexpected events such as natural disasters, theft, or accidents. According to the Australian Government’s MoneySmart guidance, choosing appropriate insurance and understanding what each policy covers or excludes is central to building financial resilience. Whether for individuals or businesses, insurance ensures that long-term investments remain secure and that recovery from adverse situations is achievable without major financial setbacks.

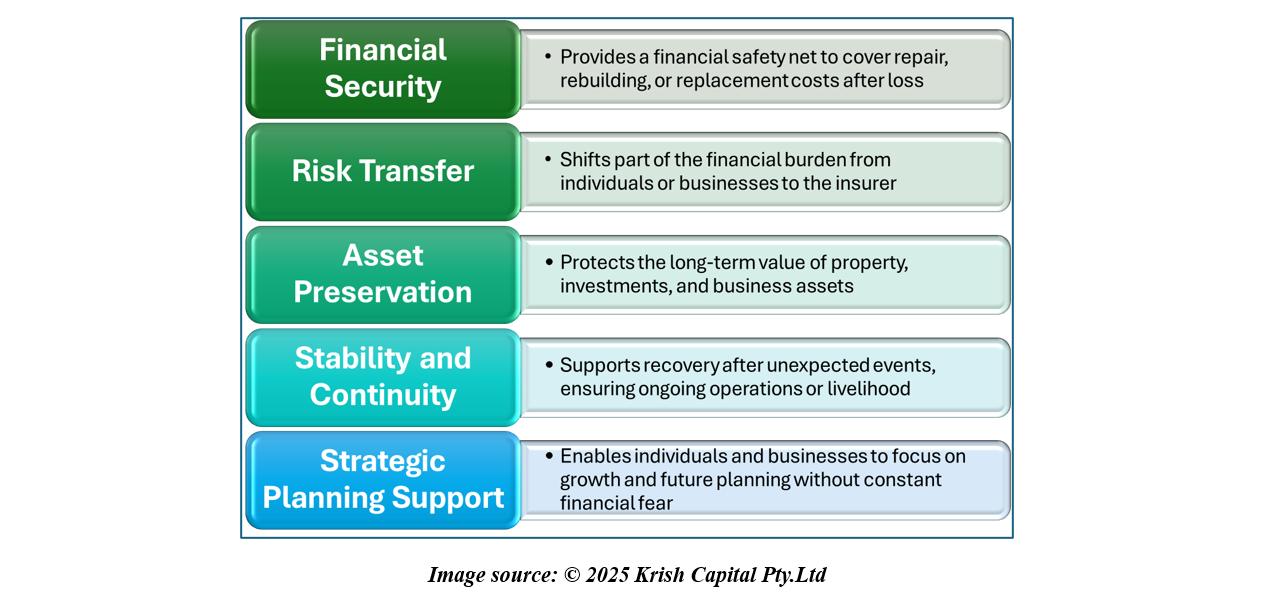

Potential Benefits and Advantages

Risks, Challenges, and Drawbacks

Despite its strengths, insurance is not without limitations. Underinsurance remains a widespread issue, where policyholders underestimate the cost of replacing assets, resulting in insufficient coverage when claims arise. Exclusions and policy conditions can also create challenges if claims fall outside defined limits or disclosure requirements are not met. Rising premiums in high-risk areas, particularly those affected by climate events, can place financial strain on households and businesses. Furthermore, some people rely too heavily on insurance, neglecting preventive measures like maintenance or risk reduction. Regularly reviewing policies and updating coverage ensures that protection remains relevant and adequate over time.

Regulatory and Policy Landscape

Australia’s insurance system is governed by a robust regulatory framework designed to protect consumers and ensure industry stability. The Australian Prudential Regulation Authority (APRA) sets prudential standards for insurers, focusing on solvency, governance, and operational soundness. The Australian Securities and Investments Commission (ASIC), through MoneySmart, provides guidance to help consumers make informed insurance choices. The Department of Finance also issues frameworks for government and public-sector entities to manage insurance risk effectively. Together, these institutions maintain public confidence by ensuring insurers remain financially secure and policyholders are treated fairly.

For individuals and investors seeking to protect their wealth, effective asset protection begins with accurate assessment of risk exposure and asset value. Reviewing policies annually ensures that coverage keeps pace with changes in property value, business growth, or market conditions. Comparing policies carefully, beyond just premium costs helps identify differences in inclusions, exclusions, and excess levels. Risk management should extend beyond insurance to include asset maintenance, security improvements, and contingency planning. Maintaining detailed records of policies, valuations, and claims supports transparency and faster resolution when claims arise. Ultimately, insurance is an evolving component of sound financial planning, designed to preserve wealth, maintain stability, and provide confidence to face uncertain times.

Disclaimer:

This article (“Article”) has been prepared by Kalkine Pty Limited (ABN 34 154 808 312) (Australian financial services licence number 425376) (“Kalkine”) and its related bodies corporate who are authorised to provide general financial product advice. Kalkine.com.au and its associated pages are published by Kalkine.

Any information/advice provided in this article is general in nature and does not take into account your objectives, financial situation or needs. You should therefore consider whether the information is appropriate for your objectives, financial situation and needs before acting upon it.

There may be a Product Disclosure Statement, Information Memorandum or other offer document (“Offer Document”) for the securities or other financial products referred to in Kalkine articles. You should obtain a copy of the Offer Document and consider it before making any decision about whether to acquire the security or financial product.

Kalkine strongly recommends that you seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) before acting on any advice/information in this Article or on the Kalkine website. Not all investments are appropriate for all people.

The information in this Article and on Kalkine website has been prepared from a wide variety of sources, which Kalkine, to the best of its knowledge and belief, considers accurate. Kalkine has made every effort to ensure the reliability of the information contained in its articles (including this Article), newsletters and websites. All information represents our views at the date of publication and may change without notice.

The information in this Article does not constitute an offer to sell securities or other financial products or a solicitation of an offer to buy securities or other financial products.

Kalkine does not issue, sell or deal in any financial products.

This Article may contain information on past performance of particular investments. Please note past performance is neither an indicator nor a guarantee of future performance.

To the extent permitted by law, and excluding any dishonesty or gross negligence by Kalkine, Kalkine disclaims and excludes all liability for any direct, indirect, implied, punitive, special, incidental or other consequential loss or damage arising from the use of or reliance on this Article, the Kalkine website and any information published on the Kalkine website without any warranties or representations by Kalkine to you. To the extent the law prohibits or limits this exclusion, Kalkine limits its liability to the resupply of services.

Please also read our Terms & Conditions and Financial Services Guide for further information.

Employees and/or associates of Kalkine and its related entities may hold interests in the securities or other financial products covered in this Article or on the Kalkine website. Any such employees and associates are required to comply with certain safeguards, procedures and disclosures as required by law.

Some of the images/music that may be used in the Article are copyright to their respective owner(s). Kalkine does not claim ownership of any of the pictures displayed/music used in the Article unless stated otherwise. The images/music that may be used in the Article are taken from various sources on the internet, including paid subscriptions or are believed to be in public domain. We have used reasonable efforts to accredit the source wherever it was indicated or was found to be necessary.

Kalkine Media Pty Ltd, an affiliate of Kalkine Pty Ltd, may have received, or be entitled to receive, financial consideration in connection with providing information about certain entity(s) covered on its website.

Copyright 2026 Krish Capital Pty. Ltd. (ABN 61629651510). All Rights Reserved. No part of this Article, or its content, may be reproduced in any form without our prior consent.

_02_19_2026_11_50_21_592067.png)

_02_11_2026_07_58_30_526403.png)

Please wait processing your request...

Please wait processing your request...