Views Expressed Disclaimer:

You are reading a free article with opinions that may differ from the recommendation given by Kalkine in its paid research reports. Become a Kalkine member today to get access to our research reports, in-depth technical and fundamental research.

Highlights

- Australia’s gold sector is experiencing a powerful boom in 2026, driven by record-high gold prices and strong investor demand for safe-haven assets.

- Northern Star Resources stands out as a large, financially strong producer delivering stable production and consistent shareholder returns through dividends.

- Perseus Mining offers higher growth potential with strong profitability and long-life projects, making it attractive for investors seeking greater upside.

As of late February 2026, the Australian gold sector has entered a historic "super-cycle." With the AUD spot gold price shattering records to trade above $7,200 per ounce, the market is witnessing a massive reallocation of capital into high-scale producers. While the broader ASX 200 faces resistance at the 9,125 mark, the Gold Index (XGD) has broken out, fueled by a "perfect storm" of geopolitical trade surcharges and sticky domestic inflation.

For investors looking to capitalize on this momentum, two stocks emerge as the clear strategic choices: Northern Star Resources (ASX:NST) for its industrial-scale stability, and Perseus Mining (ASX:PRU) for its high-margin efficiency.

1. Northern Star Resources (ASX:NST): The Institutional Powerhouse

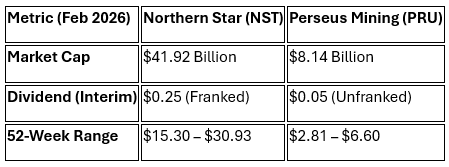

Northern Star is currently the "crown jewel" of the Australian materials sector. Trading at AUD 29.78 as of February 24, 2026, the company is reaping the rewards of its aggressive expansion strategy at the Kalgoorlie Consolidated Gold Mines (KCGM).

The Fundamental Buy Case

- Operational Scale: NST is on track for its FY26 guidance of 1.6M – 1.7M ounces of gold production.

- KCGM Growth Engine: The mill expansion at Kalgoorlie is nearing operational readiness. Analysts expect this to drive All-In Sustaining Costs (AISC) down toward the lower end of the $2,450 – $2,650/oz range by year-end.

- Capital Returns: The company recently declared a fully franked interim dividend of $0.25 per share, signaling management’s confidence in its $1.17 billion cash and bullion reserves.

Technical Chart of NST

Support - 27.20- 25.70

Resistance - 32.50-35

2. Perseus Mining (ASX:PRU): The High-Margin Specialist

While NST offers stability, Perseus Mining provides superior value and margin. Currently trading at $5.77, PRU has successfully navigated the complexities of West African mining to become one of the most profitable mid-tier miners on the ASX.

The Fundamental Buy Case

- Profitability Despite Volume Dips: Although H1 FY26 production volumes were softer, PRU doubled its interim dividend to 5 cents per share. This was made possible by a 38% increase in realized gold prices, which more than offset rising unit costs.

- Project Pipeline: The Nyanzaga project in Tanzania has seen its reserve life increased to 16 years. This expansion is critical, as it secures the company’s production profile through the 2030s.

- Valuation Gap: Morningstar and other analysts suggest a fair value around $3.00, but the market is currently pricing in a "higher-for-longer" gold environment. With a P/E ratio of ~15x, PRU remains cheaper than its domestic peers.

Technical Chart

Support - 4.95-4.14

Resistance - 6.70- 7.5

Strategic Comparison: Which One Should You Buy?

The Bottom Line for Investors

The macro environment in 2026—marked by central bank de-dollarization and a potential 15% global trade surcharge—favors gold as the ultimate "safe-haven" asset.

Northern Star (NST) is the preferred choice for conservative portfolios looking for exposure to the KCGM expansion and reliable franked dividends. Perseus Mining (PRU), meanwhile, offers a compelling opportunity for those who believe the gold price will sustain its $5,000+ USD level, allowing the company to leverage its low-cost African operations for outsized returns.

Please wait processing your request...

Please wait processing your request...