Image source: © 2025 Krish Capital Pty.Ltd

Highlights

- People are living longer, making retirement planning more important than ever.

- Government pensions alone often don’t provide enough income for a comfortable retirement.

- Countries like Canada, New Zealand, the UK, Australia and India offer unique pension systems, but none are complete solutions on their own.

- Starting early, diversifying savings, and staying aware of policy changes are key to building long-term financial security.

- Retirement planning today is about combining public benefits with personal and employer savings to stay financially confident.

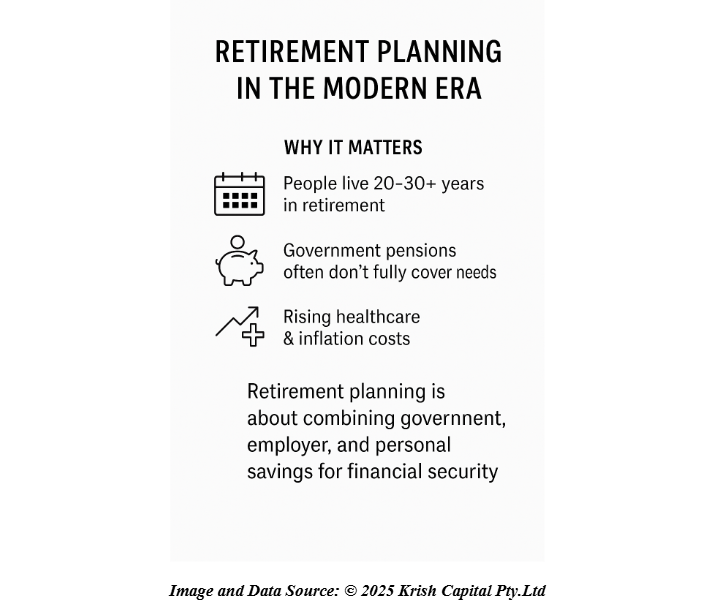

Retirement planning has always been an essential part of financial well-being, but in today’s world, it has become non-negotiable. Unlike previous generations who relied heavily on government or employer pension schemes, today's workforce must take greater personal responsibility for securing their retirement.

Without proper planning, many risk reaching their later years without sufficient savings, leaving them financially vulnerable. At the same time, global trends such as increased life expectancy, rising healthcare costs, and evolving pension systems are reshaping how we think about retirement.

Consider the following:

- Longer lifespans mean retirement could last 20–30 years or more. For example, Canada’s life expectancy at birth rose to 81.7 years in 2023, and New Zealand’s most recent period life tables show ~80.1 years for men and ~83.5 years for women (2022–2024).

- Government pensions don’t always cover everything. Replacement rates and public coverage have been under pressure in many countries; relying only on a state pension often leaves a gap.

- Pension assets are substantial but unevenly distributed. At end-2023, OECD countries had about USD 63.1 trillion earmarked for retirement — up roughly 10% from 2022 — showing both the scale and importance of pension long-term savings.

In short, hoping things will “work out” isn't a strategy. A solid, flexible plan is essential.

Retirement-Options Across Key Markets

No matter which country you’re in, retirement planning generally includes a mix of the following:

- Government / Public Pensions

- Funded through payroll taxes (social security, national insurance, etc.).

- Usually provide a basic income in retirement.

- Limitation: Often not enough for a comfortable standard of living.

- Employer-Sponsored Retirement Plans

- Defined Benefit (DB) Plans – traditional pensions (guaranteed payout, but less common now).

- Defined Contribution (DC) Plans – employer + employee contribution, but final benefit depends on investment performance.

- Personal / Individual Retirement Accounts

- Self-managed, tax-advantaged savings vehicles.

- Contributions are voluntary and may receive tax benefits.

- Private Savings & Investments

- Beyond formal pension systems, people rely on personal wealth-building:

- Equity investments (stocks, mutual funds, ETFs).

- Bonds and fixed-income products.

- Real estate.

- Gold and commodities (especially in emerging markets like India).

- Alternative assets (private equity, crypto – though risky).

- Provides flexibility and growth potential but also risk.

- Insurance-Based Products

- Products designed for retirement income and security such as Annuities (guaranteed income for life), Endowment / Pension Insurance Plans, and Long-Term Care Insurance (to cover healthcare in old age).

- Hybrid & Voluntary Systems

- Some countries encourage a three-pillar system:

- State Pension (public)

- Employer-based Pension

- Private Savings / Investments

How to do Retirement Planning right:

- Start early — The sooner you begin, the more time compounding gives your money to grow.

- Diversify your sources — Don’t rely solely on the government pension. Combine public, employer, and personal savings.

- Understand contribution levels and fees — What percentage of your salary goes in? What are the fees in your pension fund? These affect how much you’ll end up with.

- Adjust risk over time — Early in your career, you can take more investment risk. As you get closer to retirement, move toward safer options to protect what you have.

- Stay informed about policy changes — Laws change. Pension ages can shift. Benefit amounts may adjust. Awareness helps you adapt.

- Plan for healthcare and inflation — Retirement costs often rise with age. Budget for unexpected health costs. Inflation erodes savings.

Conclusion

Retirement planning in the modern era isn’t optional, it’s essential for everyone working, no matter where they are. To do it right, you need to combine what exists with personal savings, make smart decisions, and adapt as things change. With good planning, you can look forward to your retirement years with confidence instead of worry.

Please wait processing your request...

Please wait processing your request...