Highlights

- Individuals must rely on savings, investments, and government support when pensions are unavailable.

- Estimating future expenses helps retirees align lifestyle goals with financial resources.

- Diversified portfolios play a key role in building long-term retirement income.

- Sustainable withdrawal strategies ensure savings last throughout retirement.

- Healthcare planning and lifestyle adjustments help retirees manage financial uncertainty.

For previous generations, retirement planning often relied on employer-funded pensions that guaranteed a fixed income for life. Today, however, traditional pensions are far less common, leaving many individuals responsible for building their own retirement security. While this shift offers more flexibility and control, it also demands proactive planning, disciplined saving, and a thoughtful strategy. If you’re preparing for retirement without a guaranteed pension, understanding the key components of a self-built retirement plan can help you make confident, informed decisions.

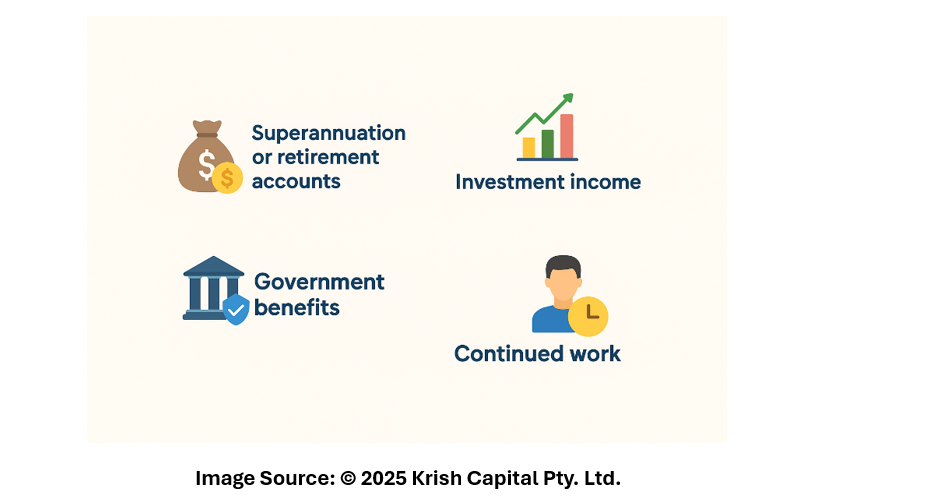

- Understand Your Income Sources Beyond Pensions

Without a pension, your retirement income will likely come from a mix of personal savings, investments, government programs, and part-time earnings. Key sources may include:

- Superannuation or retirement accounts: Your employer contributions and voluntary top-ups form the core of your retirement savings.

- Investment income: Dividends, interest, rental income, or systematic withdrawals can help cover living costs.

- Government benefits: Programs like Australia’s Age Pension or Social Security in the U.S. may offer partial support depending on your income and assets.

- Continued work: Many retirees choose part-time or flexible work to supplement income and stay active.

Mapping out these sources early helps you understand your starting point and identify gaps.

- Estimate Your Retirement Costs Realistically

Without a pension’s guaranteed monthly payment, it becomes crucial to calculate your expected expenses. Consider:

- Housing costs (rent, mortgage, downsizing)

- Healthcare and insurance

- Utilities, groceries, and everyday spending

- Travel and leisure

- Unexpected expenses such as home repairs or medical emergencies

Create a budget that reflects the lifestyle you want to maintain in retirement. A clear understanding of your spending needs helps you determine how much income you’ll require and whether your current savings trajectory aligns with those goals.

- Build a Diversified Investment Portfolio

Investments take on greater importance when you don’t have a pension. A diversified portfolio, spread across equities, bonds, cash, property, and potentially alternative assets, can help balance risk and growth. Your investment strategy should evolve over time:

Using index funds, ETFs, or managed funds can offer broad market exposure without the complexity of picking individual stocks. Many individuals benefit from a disciplined, set-and-forget approach based on their risk tolerance and time horizon.

- Develop a Sustainable Withdrawal Strategy

When you retire without a pension, your accumulated savings become your income source. Determining how much to withdraw, and when, is critical. Common strategies include:

- The 4% rule, which suggests withdrawing 4% of your portfolio in the first year and adjusting for inflation.

- Bucket strategies, where your savings are divided into short-term, medium-term, and long-term buckets for spending and investing.

- Dynamic withdrawals, which adjust based on market performance.

The goal is to ensure your savings last throughout your retirement years while supporting your lifestyle needs.

- Consider Downsizing and Lifestyle Adjustments

Housing costs often take up a significant portion of retirement spending. Downsizing to a smaller home, relocating to a more affordable area, or reducing discretionary expenses can extend the life of your savings. Lifestyle choices, such as reducing travel frequency, prioritising essential spending, or embracing low-cost activities, can also contribute to long-term financial stability.

- Prepare for Healthcare and Long-Term Care Costs

Healthcare is one of the most unpredictable costs in retirement. Without a pension, it’s essential to plan ahead by maintaining adequate insurance, setting aside funds for medical needs, and exploring whether supplemental coverage makes sense. Those expecting long-term care, or support in later life, should incorporate these costs into their planning early.

- Seek Professional Guidance When Needed

Financial advisers and retirement planners can offer personalised support, especially when managing complex portfolios or projecting long-term needs. Even a one-time consultation can help clarify your financial direction and identify strategies you may have overlooked.

Planning for retirement without a traditional pension requires foresight, discipline, and adaptability. While the responsibility has shifted from employer to individual, the tools and opportunities for building a secure retirement have expanded. By understanding your income sources, investing wisely, managing spending, and preparing for unexpected costs, you can create a retirement plan that supports both financial security and quality of life.

_02_02_2026_10_13_51_245554.png)

Please wait processing your request...

Please wait processing your request...