Highlights

- Relocating can reduce living costs but may introduce new tax considerations.

- Housing decisions—downsizing, renting, or buying—significantly affect long-term cash flow.

- Moving closer to support networks may lower care expenses but raise lifestyle costs.

- Healthcare access, insurance rules, and local service pricing heavily influence retirement budgets.

Relocating after retirement is a major financial decision that can reshape long-term expenses, income stability, and lifestyle costs. Many retirees consider moving for affordability, proximity to family, or lifestyle preferences. However, relocation carries financial trade-offs that need careful assessment. Below is a detailed breakdown of key advantages and disadvantages to help retirees evaluate whether a move aligns with their financial outlook.

Lower Cost of Living: A Major Potential Advantage

One of the strongest financial motivations for relocating is the possibility of reducing day-to-day living expenses. Areas with lower housing costs, cheaper utilities, and more affordable transportation can significantly stretch retirement savings. For retirees living on fixed income sources—such as pensions, superannuation withdrawals, or Social Security—moving to a more economical region can boost purchasing power.

Additionally, some destinations offer lower property taxes, reduced insurance premiums, or community discounts for seniors. These location-specific benefits can lead to meaningful annual savings, especially for those managing rising healthcare or lifestyle costs. However, it is important to calculate the full cost profile, not just headline affordability, before committing to a new location.

Housing Decisions and Long-Term Financial Impact

Housing is often the most influential cost factor in retirement relocation. Downsizing from a family home to a smaller property or apartment may free up equity that can be reinvested or used to supplement income. Renting instead of owning can improve flexibility and reduce maintenance burdens.

However, moving into competitive property markets can introduce higher purchase prices, strata fees, or rental costs that offset expected savings. Renovation needs, stamp duties, and relocation expenses also add to the financial burden. Retirees must evaluate the long-term implications of their housing choice to avoid liquidity constraints or unexpected outflows.

Tax Implications: Potential Savings but Possible Trade-Offs

Changing states or countries may alter tax obligations. Some regions offer tax advantages for retirees through reduced income taxes, favourable treatment of retirement withdrawals, or exemptions for pension income. In contrast, other areas may impose higher taxes on property, inheritance, or investment income.

International relocation adds complexities such as double-taxation rules, currency fluctuations, and compliance with residency requirements. Before moving, retirees should consult financial and tax advisers to ensure that new tax obligations do not diminish projected savings.

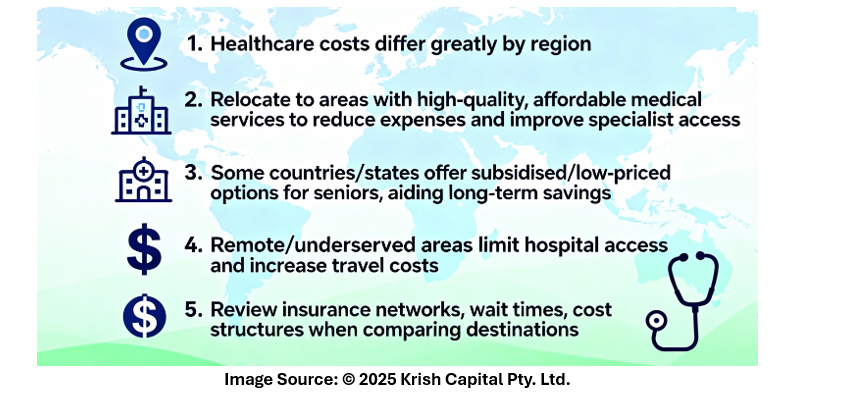

Healthcare Access and Costs Vary by Location

Healthcare is a central consideration in retirement planning, and costs can differ greatly depending on the region. Relocating to an area with high-quality, affordable medical services can reduce out-of-pocket expenses and improve access to specialists. Some countries or states offer subsidised or lower-priced healthcare options for seniors, which can contribute to long-term savings.

However, moving to remote or underserved areas may limit access to hospitals and increase travel expenses for medical appointments. Insurance networks, wait times, and cost structures should all be reviewed when comparing potential destinations.

Social Support, Lifestyle, and Hidden Spending Risks

Retirees who move closer to family often benefit from reduced care costs, shared living arrangements, or informal support. Conversely, relocating to a new community can introduce social adjustment expenses—joining clubs, frequent travel to visit loved ones, or spending more on entertainment to build new networks.

Moving to popular retirement hubs may also elevate lifestyle expenses due to higher demand in sectors like dining, leisure, and healthcare. These hidden costs can accumulate over time and need to be accounted for during budgeting.

Conclusion: A Decision That Requires Holistic Financial Planning

Relocating after retirement can provide cost-of-living advantages, improved lifestyle alignment, and tax efficiencies. Yet it can also introduce new housing costs, healthcare challenges, and unforeseen spending pressures. Careful financial modelling—combined with tax guidance and a clear assessment of long-term needs—can help retirees determine whether moving supports overall financial stability and wellbeing.

_02_02_2026_10_13_51_245554.png)

Please wait processing your request...

Please wait processing your request...