Highlights

- Retirement works best when couples dream, plan, and save together.

- Aligning goals and managing joint assets ensures a smoother, stress-free future.

- Regular check-ins and open communication keep both finances and relationships healthy.

Planning for retirement as a couple is more than just stacking up savings—it’s about two people aligning their dreams, their mindset, and their assets so they can enjoy the next chapter together. Whether you’re decades away or just around the corner from retiring, synchronising goals and managing joint assets can make a big difference. Here’s a guide designed for couples: helping you move through this process together.

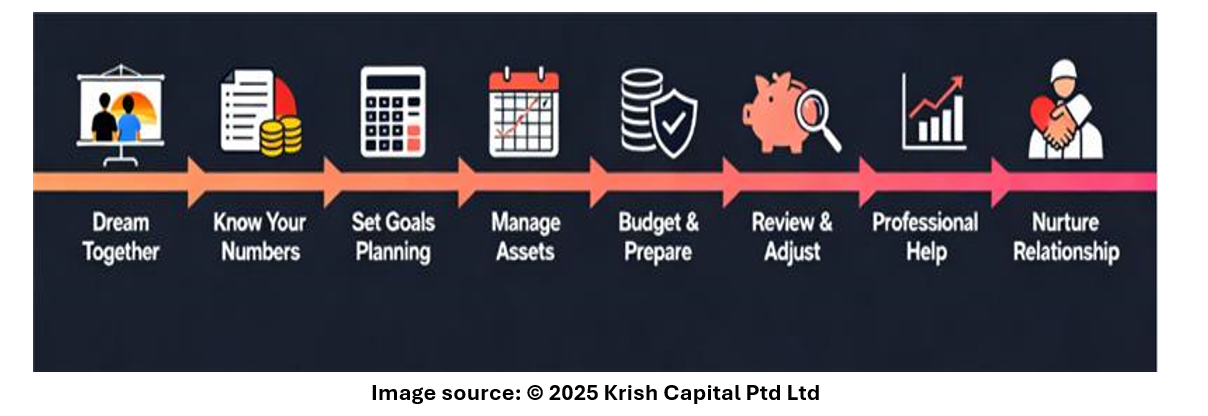

- Dream Together: Paint Your Shared Picture

Before you talk numbers, start with vision. What does retirement look like for both of you? Maybe one partner imagines travelling the world, the other wants to volunteer locally. Maybe you envision a quieter life with hobbies and grandchildren. The important part: talk about it openly. Couples who discuss their retirement dreams tend to have clearer, more purposeful plans. By aligning your vision, you create a foundation for everything else that follows.

- Be Honest About Where You Are

Once you have the vision, it’s time for a reality check. Sit down together and review:

- What are your combined assets—pension plans, savings, investments?

- What are your debts and ongoing expenses?

- What are each of you expecting when you retire (income, lifestyle, travel)?

Research in the U.S. found that retirement planning is often done as a “household” concern rather than strictly individual. Yet many couples are still treating the accounts separately—so one may not fully know what the other is holding. Knowing each other’s financial standing builds trust and transparency.

- Set Joint & Individual Goals

One of the tricky parts is that you bring two sets of hopes and circumstances. So:

- Set shared goals, for example: retire at age 65 together; travel for six months; downsize to a smaller home.

- Also honor individual goals, say, partner A wants to start a small business in retirement; partner B wants weekly painting classes.

Having separate and together goals helps both feel their personal identity is respected while being part of the team.

- Bring Your Timelines into Focus

When will each of you stop working? Will you retire at the same time, or stagger? Research shows that although many couples plan to retire together, in reality, many do not. For instance, one study found only 11% couples retired at the exact same time.

Deciding on timing is important because it affects income, benefits, healthcare, and lifestyle. If one partner retires earlier, you’ll need a plan for how that affects joint spending and savings.

- Manage Joint Assets Smartly

When you pool assets, things like pensions, savings accounts, investments, and housing all become part of the plan. Some key checks:

- Review whose names the accounts are in; sometimes only one person’s name holds a retirement account—yet both lives are affected.

- Coordinate savings and contributions. In a U.S. study, 24 % of couples failed to coordinate retirement contributions, and therefore missed out on employer matching and other benefits.

- Agree on how you’ll draw income in retirement: sources like pensions, investments or part‑time work.

- Budget for Living & Unexpected Turns

Your retirement budget is different from your working years. As a couple you’ll want to estimate:

- What kind of lifestyle do you want? Travel, hobbies, or home upgrades?

- What fixed costs will you have—housing, utilities, healthcare?

- Are you prepared for scenarios like one partner needing long‑term care, or you living longer than expected?

Many couples forget to build in those “what ifs.” Risk and uncertainty are part of the package.

- Review & Adjust Regularly

Life changes: health, jobs, markets, family needs. That means your retirement plan should not be “set and forget.” Good couples schedule at least one annual check‑in to ask: Are we still aligned? Have our dreams shifted? Are our assets still performing as expected? Staying engaged prevents surprises at the eleventh hour.

- Seek Help When Needed

When the numbers, choices, or strategies feel complex, it’s wise to bring in a professional. Financial planners who understand couples’ dynamics can help you: optimise pension benefits, plan taxes, manage joint vs individual accounts.

Getting guidance can ease stress and keep you both confident in the plan.

- Nurture Your Relationship Through It

Beyond numbers and accounts, retirement planning is a relational process. It’s about making decisions together—and avoiding money becoming a source of tension. Communicating well, being transparent and respecting each other’s views matters just as much as the math.

In fact, some sources say couples who co‑plan are more likely to feel secure and ready.

Final Thoughts

When you plan retirement together, you craft not just a financial path—but a shared future. Spend the time now talking, aligning and planning. Focus both on your joint life and your individual aspirations. Organise your assets as a team and revisit your plan regularly. With open communication and joint effort, you’ll be setting yourselves up not just for “enough money,” but for a retirement you genuinely look forward to—together.

Please wait processing your request...

Please wait processing your request...