Highlights

- Tracking error shows how closely an index fund really mirrors its benchmark.

- Even “passive” funds can deviate due to fees, cash drag, and rebalancing delays.

- Tracking difference measures the average gap; tracking error measures the consistency of that gap.

- Low tracking error equals efficient fund management, whereas high error translates to unpredictable performance.

- Smart investors check historical tracking errors to capture maximum benchmark returns.

Index funds are widely regarded as the simplest way to “own the market.” Designed to mirror the performance of a benchmark, such as the ASX 200, S&P 500, or MSCI World Index, these funds aim to deliver returns that closely track those of the index. Yet, in practice, an index fund’s performance almost always diverges slightly from its benchmark. This difference is known as tracking error and understanding it is key to assessing how efficiently an index fund is managed.

The Invisible Gap: Understanding Tracking Error

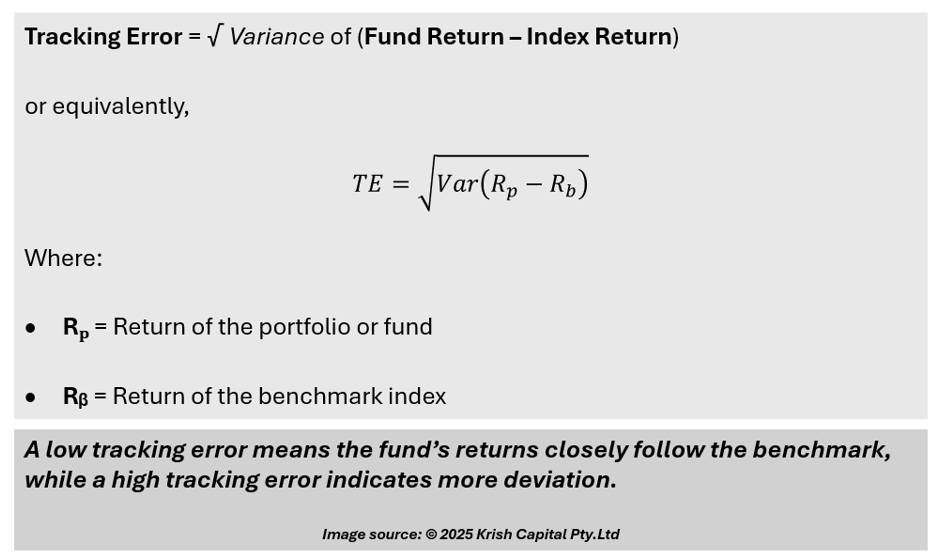

Tracking error measures how consistently an index fund replicates its benchmark’s returns over time.

It is typically calculated as the standard deviation of the differences between the fund’s returns and those of the benchmark.

Example:

If the NASDAQ 50 gains 10% in a year while a NASDAQ index fund earns 9.6%, the 0.4% gap represents the tracking difference. If that gap fluctuates over time, the volatility of those deviations reflects the tracking error.

From Fees to Fluctuations: Why Tracking Errors Occur

Even though index funds are designed to be “passive,” perfect replication is rarely possible. A range of operational, structural, and market-related factors introduces small discrepancies.

- Expense Ratios and Management Fees

All index funds charge a management fee (expense ratio) to cover operational costs. Since benchmarks do not bear such expenses, fund returns are naturally slightly lower. - Cash Drag

Funds typically hold small cash reserves to manage investor inflows and redemptions. This uninvested cash can slightly reduce returns when markets rise. - Dividend Timing and Reinvestment Delays

Benchmarks assume immediate dividend reinvestment, but funds may experience a lag between receiving and reinvesting dividends, creating minor short-term differences in returns. - Portfolio Rebalancing and Turnover

When an index updates its constituents, funds must rebalance their portfolios. However, timing differences, transaction costs, and liquidity challenges can prevent perfect synchronization. - Sampling vs. Full Replication

For broad or complex indices (like MSCI World or Nifty Next 50), many funds use sampling, holding a representative subset rather than every constituent. This reduces costs but can introduce return variation. - Currency Movements and Withholding Taxes (for Global Funds)

International index funds face currency fluctuations and foreign dividend taxes, factors that affect fund performance but not the benchmark directly.

Difference or Deviation? Making Sense of Tracking Errors

These two terms are often confused but represent distinct concepts:

- Tracking Difference → The average gap between the fund’s returns and the benchmark’s returns (usually due to costs and fees).

- Tracking Error → The volatility of that gap over time (consistency of replication).

A fund might have a small tracking difference, but a large tracking error, meaning it occasionally outperforms or underperforms its benchmark unpredictably, indicating inconsistency.

Why Investors Should Care About Tracking Error

Tracking error serves as a key indicator of a fund’s replication efficiency.

- A low tracking error signals disciplined management and precise execution.

- A high tracking error suggests inefficiencies, higher costs, or structural challenges that may reduce long-term performance.

Institutional investors pay close attention to tracking errors because it reflect how closely a fund actually delivers the index exposure it promises.

For context:

- A Nifty 50 ETF with tracking error below 0.10% is considered highly efficient.

- Small-cap or global ETFs may exhibit higher tracking error (0.5–1.0%) due to liquidity and currency factors.

Practical Ways to Limit Your Fund’s Tracking Error

Investors can improve their outcomes by choosing funds with efficient replication and low tracking errors.

- Review Historical Tracking Errors: Check out the fund’s reported tracking error over time to gauge consistency.

- Compare Expense Ratios: Lower costs generally lead to smaller performance gaps.

- Evaluate Rebalancing Discipline: Funds with transparent, rule-based rebalancing track their benchmarks more closely.

- Assess Fund Size and Liquidity: Larger more liquid funds typically achieve better replication accuracy.

- Consider Fund Structure: ETFs often maintain lower tracking errors than index mutual funds due to their in-kind creation and redemption mechanism.

Efficiency Over Perfection: The Smart Investor’s Approach

No index fund will ever perfectly match its benchmark every day, but perfection isn’t the point. The real goal is minimising tracking errors so that investors can capture as much of the benchmark’s performance as possible, net of fees and frictions.

In today’s world, where passive investing dominates global markets, understanding tracking error helps investors distinguish between cheap exposure and true efficiency. Over time, that subtle difference can have a profound impact on wealth creation.

Please wait processing your request...

Please wait processing your request...