Highlights

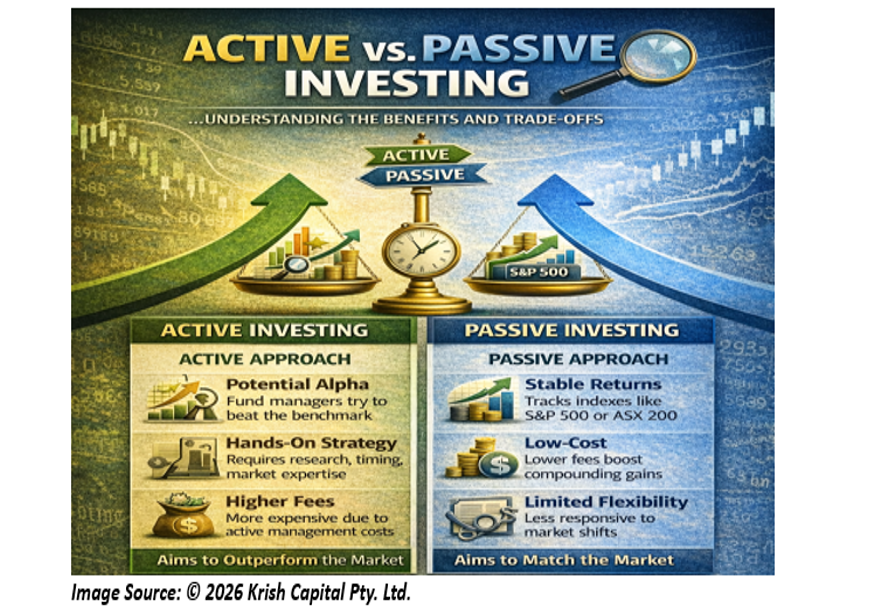

- Active investing aims to outperform the market, while passive investing seeks to match it at lower cost.

- Research consistently shows that most active fund managers struggle to beat benchmark indices over time.

- Over the past year, the S&P 500 delivered a return of 15.70%, while Australia’s S&P/ASX 200 gained 10.62%, highlighting the power of broad market exposure

- Passive investing benefits from lower fees and long-term compounding, especially in steady bull markets.

- Active strategies may offer flexibility during volatile or declining market conditions.

- Many investors now adopt a blended approach to balance cost efficiency with tactical flexibility.

Markets reward discipline over drama. Yet when it comes to building wealth, investors are often pulled between two very different philosophies. One prioritises strategic decision making, research and timing. The other relies on broad exposure, patience and cost efficiency. Both aim to grow capital, but they approach risk, opportunity and market cycles in fundamentally different ways.

Active investing revolves around selection and timing. It involves researching companies, identifying undervalued opportunities, and adjusting portfolios in response to economic signals. The objective of active investing is to outperform a benchmark index

Passive investing, by contrast, removes that competitive layer. Instead of trying to identify winners, investors buy an index fund that mirrors a market benchmark. The objective is not to outperform the market, but to move in line with it.

How Active Investing Works in Practice?

Active investing depends heavily on judgement and skill. Fund managers assess corporate earnings, leadership quality, sector trends and macroeconomic conditions. They increase exposure to companies they believe will outperform and trim those that appear overvalued or vulnerable.

In volatile markets, this flexibility can be appealing. During economic slowdowns or geopolitical shocks, active managers can reduce risk, hold cash temporarily or shift into defensive sectors.

However, skill is unevenly distributed. Data over many years has shown that a majority of active large-cap funds underperform broad market indices. Even when managers outperform in one year, maintaining that edge consistently proves difficult.

Also, in the Active investing it would be difficult to outperform the benchmark when the markets are strong form efficient, means the investor won’t be able to generate alpha (extra returns over the benchmark) consistently. Active investing can work where markets are weak form efficient or semi strong form efficient.

Active investing also carries higher costs. Research teams, portfolio managers and frequent trading contribute to higher expense ratios. Over time, these fees compound — quietly reducing net returns.

The Passive Advantage: Cost, Consistency and Compounding

Passive investing takes a different route. Rather than attempting to identify tomorrow’s winners, it seeks to replicate the structure of a benchmark index.

For example, an index fund tracking the S&P/ASX 200 or S&P 500 owns the same companies in roughly the same proportions as the index itself. If the index rises, the fund rises. If it falls, the fund falls.

This simplicity produces a structural advantage: lower costs. Without the need for research analysts or constant trading, passive funds typically charge significantly lower fees. Even a 1% difference in annual cost can materially affect long-term wealth accumulation.

Market performance over the past year illustrates this strength. The S&P 500 generated a 15.70% one-year return, while Australia’s S&P/ASX 200 delivered 10.62% as on 25 February 2026. Investors who simply tracked these indices participated directly in those gains without needing to select individual stocks.

Over extended periods, broad indices have historically averaged close to 10% annually, reinforcing the argument that matching the market can be more effective than attempting to outguess it.

Bull Markets: Where Passive Often Shines

In periods of steady economic expansion and rising equity markets, passive investing tends to perform favourably.

When markets trend upward broadly, diversification works in the investor’s favour. Instead of needing to identify which individual companies will outperform, passive investors capture gains across sectors.

Lower fees further amplify results. In strong bull markets, consistent exposure and cost efficiency often outweigh the potential benefits of tactical positioning.

Bear Markets and Volatility: The Case for Flexibility

Market downturns present a more complex picture.

When indices decline sharply, passive funds will inevitably mirror those losses. They cannot sidestep structural market risk. Investors must rely on eventual recovery.

Active managers, however, have the option to reposition portfolios. They may tilt towards defensive industries, reduce exposure to highly leveraged companies or temporarily increase cash holdings.

In theory, this flexibility can add value during volatile or uneven markets. In practice, success depends entirely on the manager’s timing and judgement, both of which are difficult to execute consistently.

Volatility often widens the gap between strong and weak businesses, creating opportunity. But identifying those opportunities in real time remains challenging.

The Psychology Factor

Beyond performance statistics, investor behaviour plays a critical role.

Active investors sometimes buy after prices have surged and sell after declines, reacting emotionally to market swings. Passive investing, built around long-term holding, reduces the temptation to time markets.

By removing constant decision-making, passive strategies can help investors maintain discipline a hidden advantage that often goes overlooked.

Blended Strategies: A Middle Ground

For many investors, the debate is not binary.

A blended approach, allocating a core portion of the portfolio to passive index funds while reserving a smaller allocation for active strategies allows participation in broad market growth while retaining flexibility.

For example, an investor might place 80–90% of assets in low-cost index funds tracking benchmarks like the S&P 500 or S&P/ASX 200 and actively manage a smaller allocation to explore specific themes or sectors.

This structure limits overall costs while providing room for tactical insight.

Choosing the Right Approach

The choice between active and passive investing ultimately depends on time horizon, engagement level and tolerance for variability.

Passive investing may suit those seeking steady participation in global growth with minimal oversight and lower fees. Also, the passive investing is generally preferred when the markets are strong form efficient.

Active investing may appeal to those willing to invest time, accept higher costs and pursue potential outperformance knowing that consistent success is difficult. Active investing is useful when the markets are weak form or semi-strong form efficient.

Market conditions matter. In broad, rising markets, passive exposure has historically delivered competitive outcomes. In turbulent or fragmented environments, active management may offer opportunities though without guarantees.

For most investors, the objective is not to win every year. It is to build sustainable wealth over time. Whether through disciplined indexing, selective active positioning or a combination of both, success often depends less on prediction and more on patience.

Please wait processing your request...

Please wait processing your request...