Highlights

- Franking credits attach tax paid to dividends distributed by Australian companies.

- Eligible investors may offset tax liabilities or receive cash refunds.

- Fund structures determine how franking benefits are passed to unit holders.

- Policy and tax settings can alter the value of franking credits over time.

Franking credits are a feature of Australia’s dividend imputation system and play a measurable role in shaping returns for equity-focused funds. The system was introduced to reduce the double taxation of corporate profits by allowing shareholders to receive a credit for tax already paid at the company level. For investors in managed funds and exchange-traded funds (ETFs), franking credits can influence reported income, tax outcomes, and total return calculations.

Under the imputation system, when an Australian company pays corporate tax on its profits and later distributes those profits as dividends, it may attach franking credits to the dividend. These credits represent the tax already paid by the company. Investors who receive franked dividends can use the credits to offset their own tax liabilities. If the credits exceed the tax payable, eligible investors may receive a refund, subject to prevailing tax rules. The extent to which dividends are franked depends on the company’s tax position and the proportion of profits derived from Australian taxable income.

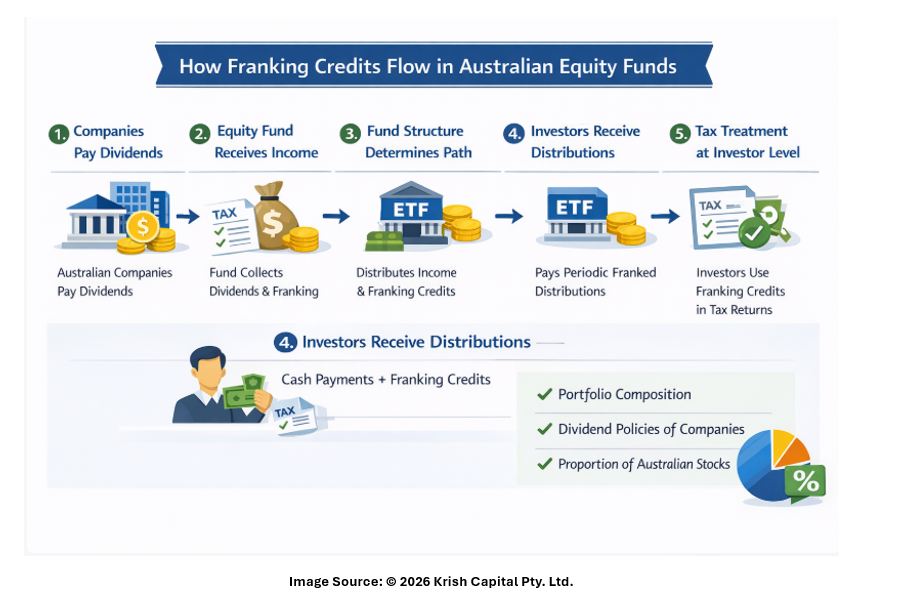

How Franking Credits Flow Through Funds

For Australian equity funds, franking credits are collected at the fund level and can be passed through to investors as part of distributions. The mechanism differs by structure. Unit trusts and some managed funds typically distribute income and franking credits to investors, who then apply the credits in their personal tax returns. ETFs tracking Australian equity indices often distribute franked income on a periodic basis, reflecting the dividends received from underlying holdings. The level of franking available to investors therefore depends on the composition of the portfolio and the dividend policies of the companies held.

The Impact on Reported and After-Tax Returns

The impact of franking credits on fund returns can be observed in income yields and after-tax outcomes. Funds with higher exposure to fully franked dividend payers, such as large domestic banks, insurers, and certain industrial companies, may report higher distributable income once franking is included. However, reported pre-tax performance figures may not fully reflect the value of franking credits, as standard total return metrics often focus on price movements and cash distributions. For taxable investors, the after-tax return may differ from the pre-tax return depending on their marginal tax rate and eligibility to use or receive refunds for excess credits.

Who Benefits Most From Franking Credits?

Investor eligibility and tax circumstances are central to the value derived from franking credits. Australian resident taxpayers can generally apply franking credits to reduce tax payable on dividend income. Superannuation funds in the accumulation phase may use credits to offset tax liabilities within the fund, while funds in the pension phase, subject to current rules, may be eligible for refunds of excess credits. Non-resident investors typically cannot use franking credits, which means the benefits are largely confined to domestic investors. As a result, the effective yield of Australian equity funds may differ between resident and non-resident unit holders.

Portfolio Choices and Distribution Timing

Fund managers may also consider franking levels when managing portfolios, though investment mandates and benchmark tracking constraints limit the extent to which portfolios can be positioned specifically for franking outcomes. Index-tracking funds mirror the franking profile of their benchmarks, while active managers may adjust exposures based on income objectives, sector allocations, and dividend sustainability considerations. Turnover within portfolios can affect the franking credits passed through to investors, as holding periods and ex-dividend timing influence entitlement to credits under Australian tax rules.

Policy Shifts and Market Cycles Matter

Policy and regulatory settings can alter the treatment and value of franking credits over time. Changes to corporate tax rates, dividend payout practices, and tax refund rules can all influence how much value investors derive from franking. Market conditions also matter: during periods when companies reduce dividends, the pool of available franking credits across the market may decline, affecting income distributions from Australian equity funds.

In summary, franking credits form an integral component of the return profile for Australian equity funds, particularly for domestic taxable investors. Their impact is most visible in after-tax outcomes rather than headline performance figures. Understanding how franking credits flow through different fund structures, and how eligibility varies by investor type, helps in interpreting income distributions and total returns from Australian-focused investment funds.

Please wait processing your request...

Please wait processing your request...