Highlights

- SIPs are the retail form of dollar-cost averaging — investing small amounts regularly will build wealth over time.

- They remove guesswork and emotional timing from investing, helping many people stick to a plan.

- SIPs are especially popular in emerging markets (notably India), though the underlying idea is used worldwide (401(k)s, payroll plans, ETFs).

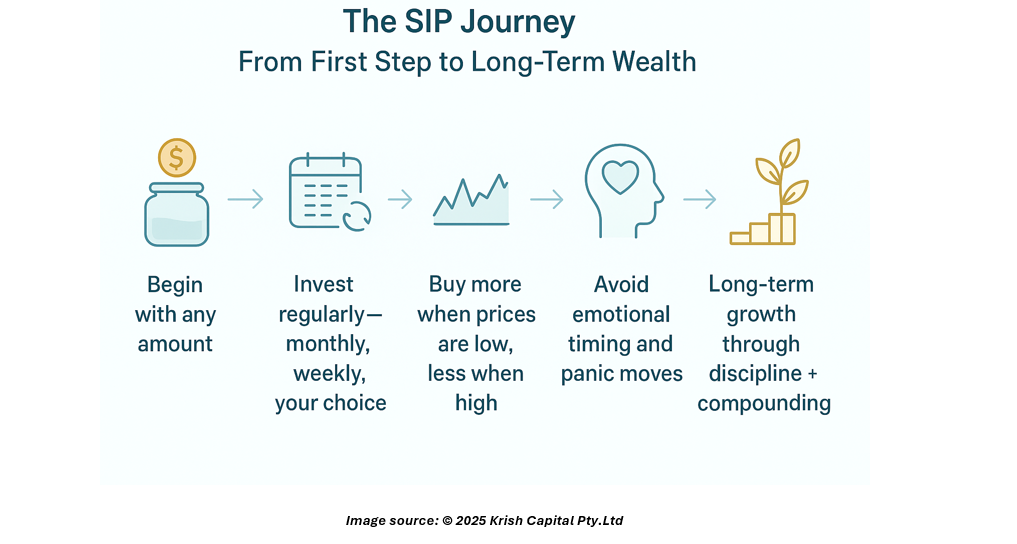

Imagine turning the habit of saving into a simple machine: every month a little money leaves your bank and quietly buys pieces of a fund for you. That’s a Systematic Investment Plan (SIP) — an automated way to invest a fixed sum at regular intervals into mutual funds, ETFs, or other pooled vehicles. The concept is the same as “dollar-cost averaging” (DCA): you buy more units when prices are low and fewer when prices are high, which can lower your average purchase cost over time.

Why people choose SIPs

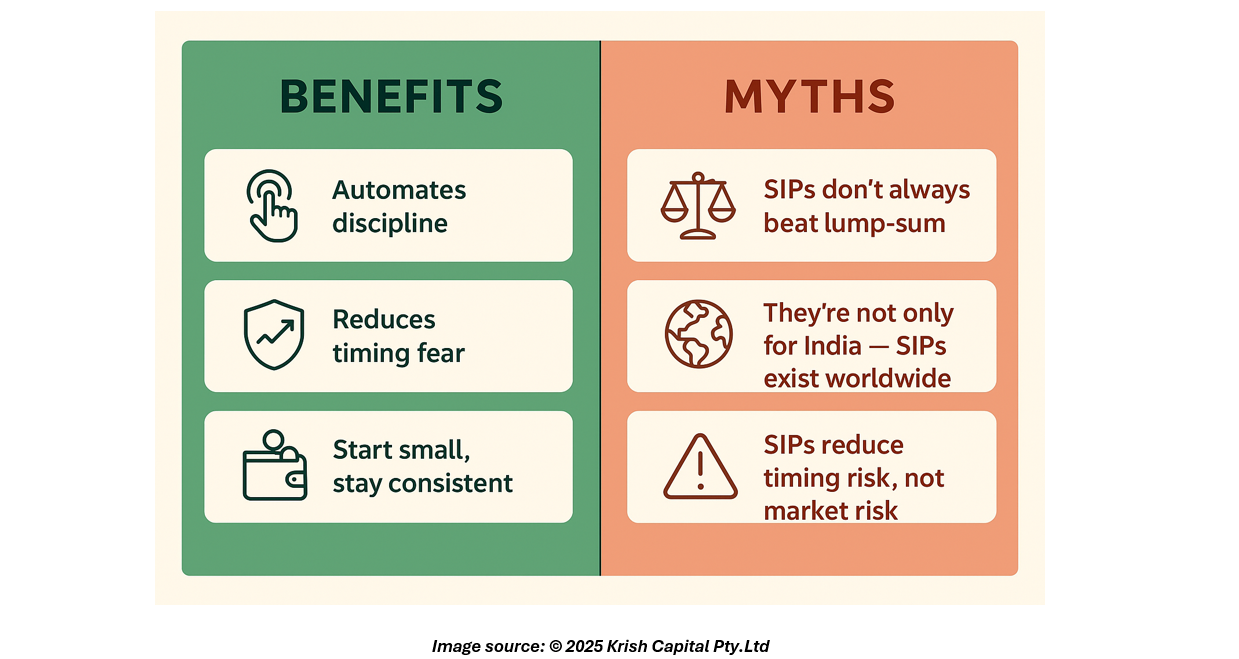

- Discipline without drama. SIPs automate investing. When money leaves your account on a schedule, you avoid deciding “is today the right day?” again and again — and that’s powerful for building long-term habits.

- Less stress about timing. Markets move up and down. Spreading purchases reduces the risk of committing a big lump when prices are high, which is reassuring for many investors.

- Access and affordability. SIPs let people start small — often with modest minimums — so becoming an investor doesn’t require a windfall. This democratizes access to funds across countries and income levels.

- Behavioral advantages. Psychology matters: SIPs guard against impulse selling, procrastination, and the urge to “time the market.” That emotional dampener can improve outcomes more than pure math predicts.

Common misconceptions — and the clearer truth

Myth 1: SIPs always give better returns than lump-sum investing.

Truth: Historically, a lump-sum invested immediately has outperformed DCA in many markets because markets generally rise over long horizons. Research shows that lump-sum often wins mathematically, though not always. The tradeoff is between potential higher returns and lower emotional/psychological risk.

Myth 2: SIPs are only for beginners or only for India.

Truth: While SIPs are extremely popular in some countries (India’s mutual-fund SIP culture is a notable example), the practice of periodic investing exists globally — think payroll contributions to retirement plans or automatic ETF purchases. SIP is a delivery method; the investing principles are universal.

Myth 3: SIPs remove all investment risk.

Truth: SIPs reduce timing risk but don’t eliminate market risk. If markets fall for a long time, the value of SIP investments can decline; what SIPs help with is steady accumulation and emotional discipline.

Myth 4: SIPs guarantee a lower average cost.

Truth: DCA can lower average costs in volatile or falling markets, but if prices rise steadily, a lump sum could beat DCA. The practical benefit of SIPs often comes from helping the investor stay invested.

Practical tips for readers

- Match frequency to your cash flow. Monthly SIPs fit most pay cycles, but weekly or biweekly might suit someone paid fortnightly.

- Pick funds with clear mandates. Know what you’re buying (equity, bond, balanced, index). Read the fund fact sheet.

- Keep costs low. Fees matter over time. Prefer low-cost index funds or check active funds’ expense ratios before committing.

- Use SIPs as part of a plan. Align SIPs with goals and time horizons — retirement, home down-payment, or education — and review occasionally.

Bottom line

SIPs are a simple, proven way to convert saving into investing while avoiding emotional missteps. They’re not a magic bullet — they trade some potential upside for steadiness and psychological ease — but for many investors, that trade is exactly what helps them build wealth consistently. Whether you’re starting small or automating long-term contributions, SIPs make investing habitual, accessible, and less stressful.

Please wait processing your request...

Please wait processing your request...