Highlights

- Rebalancing restores portfolio allocations without relying on market forecasts

- Asset price movements and cash flows are the main drivers of allocation drift

- Most funds use rules-based frameworks to reduce behavioural bias

- The primary purpose of rebalancing is risk control, not return enhancement

- Costs, tax, and liquidity shape how rebalancing is implemented in practice

Rebalancing is one of the least visible yet most persistent disciplines in fund management. Unlike tactical allocation or market timing, rebalancing does not attempt to predict short-term market movements. Instead, it focuses on maintaining a portfolio’s intended risk and return profile as asset prices move over time. For diversified funds, this process plays a central role in keeping portfolios aligned with stated objectives.

At its core, rebalancing involves periodically adjusting asset weights back to predefined targets. For example, an equity-heavy rally may push a balanced fund’s share allocation well above its long-term target. Without intervention, this drift can gradually alter the fund’s risk exposure. Rebalancing addresses this by trimming assets that have grown beyond their target weights and adding to those that have fallen behind.

Why portfolios drift over time

Market movements are the primary cause of allocation drift. Asset classes rarely move in unison, and sustained rallies or drawdowns can significantly change portfolio composition. In Australian multi-asset funds, extended equity rallies or sharp interest rate shifts can quickly distort the balance between equities, fixed income, and defensive assets.

Cash flows also contribute to drift. Ongoing contributions, distributions, or redemptions may be deployed unevenly across asset classes. Over time, these operational factors can compound market-driven changes, making rebalancing a necessary maintenance function rather than an optional adjustment.

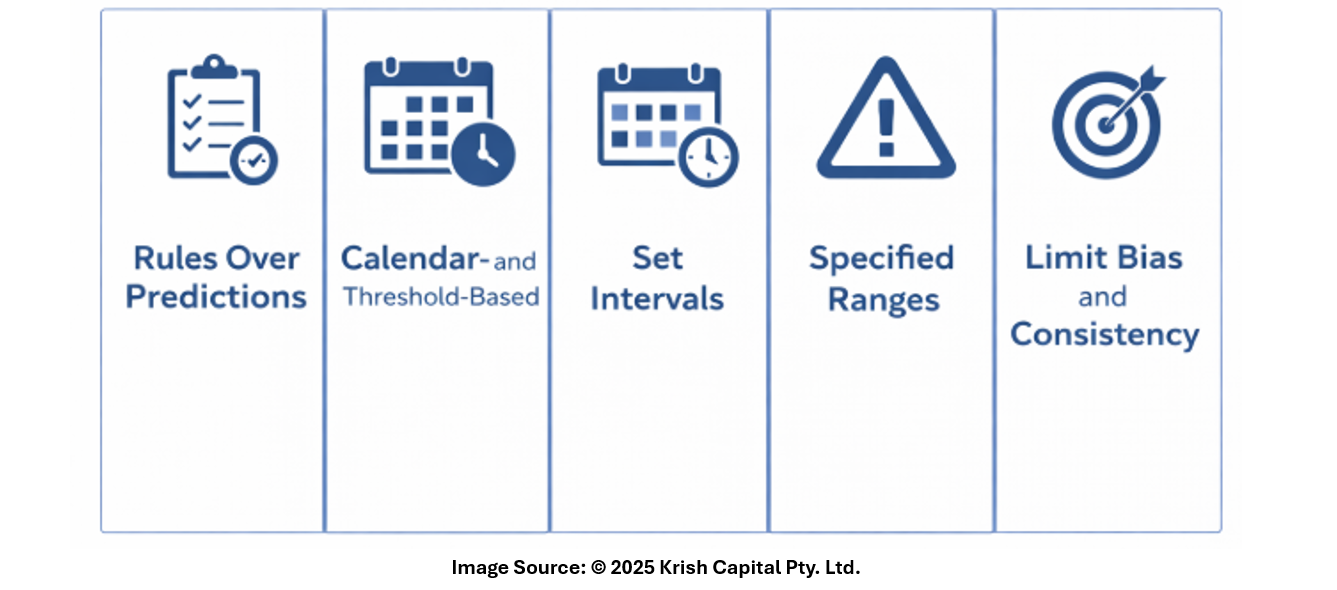

Rules over predictions

Most funds follow predefined rebalancing rules rather than discretionary calls. These rules may be calendar-based, threshold-based, or a combination of both. Calendar-based approaches rebalance at set intervals, such as quarterly or annually, regardless of market conditions. Threshold-based methods trigger adjustments only when asset weights move beyond a specified range.

This rules-based structure is designed to reduce behavioural bias. By relying on predefined parameters, fund managers avoid reacting emotionally to market volatility or headlines. The objective is consistency, not short-term optimisation.

Risk control rather than return enhancement

Rebalancing is often misunderstood as a return-seeking strategy. In practice, its primary function is risk management. By restoring target allocations, funds seek to prevent unintended concentration in assets that have recently performed well. This can be particularly relevant in periods of prolonged market momentum, when portfolios may quietly become more exposed to downside risk.

While rebalancing may incidentally result in selling assets that have risen and buying those that have lagged, this outcome is a by-product of risk control rather than a directional view on future performance.

Costs, liquidity, and implementation

Executing rebalancing trades is not costless. Transaction costs, tax considerations, and market liquidity all influence how adjustments are implemented. Large funds may stagger trades or use derivatives to manage exposure efficiently, particularly in less liquid markets.

In Australian funds, tax implications can be especially relevant for managed vehicles where realised capital gains may be distributed to unit holders. As a result, rebalancing decisions often involve balancing portfolio precision with cost and tax efficiency.

Rebalancing in stressed markets

Periods of market stress test the discipline of rebalancing frameworks. Sharp sell-offs can push asset weights rapidly outside target ranges, triggering adjustments at uncomfortable moments. However, many funds continue to apply their rules during volatility, viewing discipline as essential to maintaining long-term portfolio integrity.

Some funds may temporarily widen tolerance bands or adjust timing during extreme conditions, but wholesale suspension of rebalancing is uncommon. The emphasis remains on process adherence rather than short-term market assessment.

A quiet but structural function

Rebalancing rarely attracts attention, yet it is fundamental to how funds operate across market cycles. By focusing on structure rather than forecasts, it provides a mechanism for maintaining consistency in portfolio construction. Over time, this quiet discipline helps ensure that a fund’s realised risk profile remains broadly aligned with its stated mandate, regardless of market noise.

Please wait processing your request...

Please wait processing your request...