Highlights

- Tokenisation digitises ownership of real-world assets using distributed ledger technology.

- It expands access to investment opportunities through fractionalised ownership.

- Technology promises more transparent, efficient and affordable transactions.

- Challenges remain around regulation, cybersecurity and market infrastructure.

- Retail investors in emerging markets stand to benefit from increased accessibility.

Digital assets and tokenisation represent technology-driven solutions that are becoming increasingly ubiquitous, creating greater opportunities for investor personalisation and customisation. Technology is reshaping how investors access opportunities, widening the scope of available investments, and enabling portfolios tailored to short-term or long-term needs. However, this transformation also brings risks, with new investors exposed to hype amplified by social media, while regulatory frameworks adapt to rapidly changing environments.

Recent developments in US regulation following the GENIUS Act have placed digital assets back in the spotlight. While the focus has largely been on digital currency, the next phase centers on asset tokenisation, an innovation seen as more transformative for global finance than cryptocurrencies.

In a digital world, financial markets are experiencing a quiet yet significant revolution aimed at making investing more accessible, faster, cheaper and more transparent.

Hybrid models of tokenisation are also emerging, depending on which parts of an asset’s value chain are captured on-chain. Examples include:

- Assets completely off-chain, such as publicly listed stocks

- Fully digital assets like bitcoin, existing entirely on a digital ledger

- Investment funds accessed through digital tokens but still holding traditional assets

Each token acts as a digital ownership certificate or a claim to a portion of a real-world asset. These tokens can be traded peer-to-peer on blockchain-based systems, potentially around the clock and across borders.

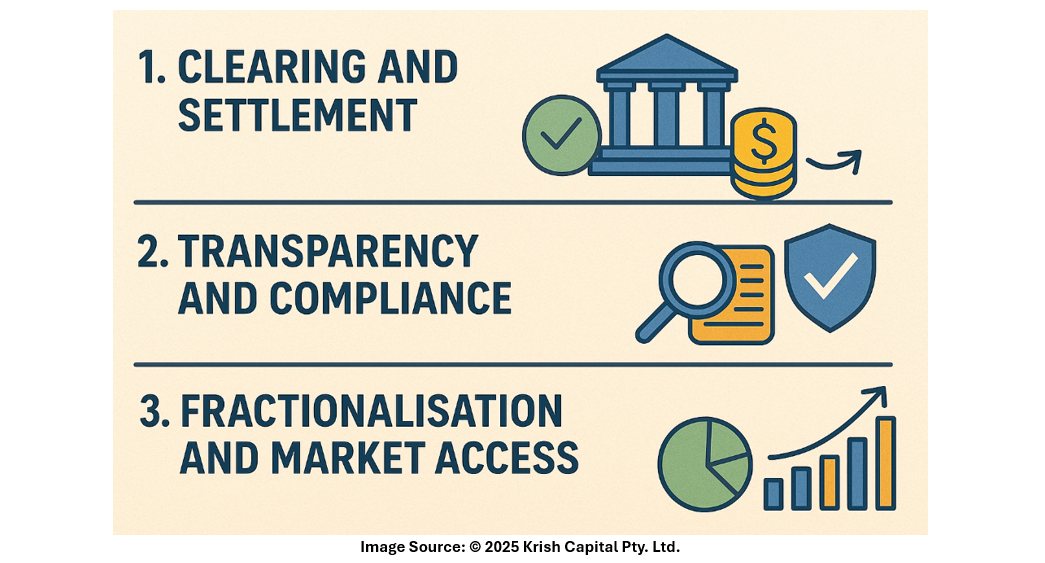

The Value Proposition of Tokenisation

Tokenisation purports to improve several critical functions within financial markets. Its value proposition can be grouped under three key areas:

- Clearing and Settlement

Smart contracts automate tasks such as compliance checks, dividend payments and settlement. This reduces multiple layers of intermediaries that traditionally make transactions costly, complex and slow. The result is:

- Near-real-time settlement, especially valuable in cross-border transactions

- Reduced human error and operational expense

- Transparency and Compliance

Blockchain technology provides a shared, immutable system of record. Every transaction and ownership change is logged and verified by the network. This offers:

- Improved visibility into asset provenance

- Easier auditing and real-time compliance monitoring

- Lower risk of fraud or manipulation

- Fractionalisation and Market Access

Tokenisation enables fractional ownership, reducing capital requirements and lowering barriers to investment. This expands access to asset classes previously limited to institutional or wealthy investors, such as real estate or private equity. It opens opportunities particularly for:

- Retail investors

- Individuals in emerging economies with limited access to traditional finance

With just a smartphone and internet connection, new investors can participate in assets that were once out of reach.

Democratising Financial Access

One of the most powerful aspects of tokenisation is its potential to level the playing field. Instead of requiring full ownership of a high-value asset, investors can purchase smaller, more affordable units through tokens.

For example, an individual can buy a fraction of a commercial building rather than the entire property. Such democratisation supports wealth creation across broader populations and offers global investment participation without geographic limitations.

In emerging markets, tokenization can serve as a bridge to financial inclusion. It allows individuals to bypass legacy constraints while still benefiting from investor protections. This shift in accessibility may bring new groups into the investing ecosystem.

Cheaper, More Efficient and Faster Transactions

Traditional market processes rely on multiple intermediaries and involve administrative delays, especially when operating across borders or time zones. Tokenisation simplifies these processes through smart contract automation, allowing:

- Faster reconciliation

- Lower operational costs

- More flexible asset custody solutions

Investors can choose self-custody through digital wallets or rely on third-party custodians, depending on personal risk tolerance.

Building Trust Through Transparency

Blockchain’s inherent auditability enhances trust among market participants. Every transaction becomes part of a distributed ledger where:

- Ownership structures are clear

- Information is readily traceable

- Double-spending risks are significantly reduced

This reduces information gaps between market participants, allowing decisions to be made with better visibility into risks and asset health.

Challenges and Considerations Ahead

Despite its potential, tokenisation faces several significant hurdles that must be addressed for mainstream adoption:

- Limited interoperability between blockchain systems and legacy infrastructure

- Regulatory uncertainty around digital asset classification and oversight

- Liquidity constraints in secondary trading markets

- Cybersecurity and privacy concerns

- Questions about the appropriateness of offering easier retail access to private markets

These uncertainties contribute to a still-developing market infrastructure. Financial institutions and policymakers continue working toward standardized frameworks and solutions that support safe implementation and scale.

Conclusion

Asset tokenisation is reshaping market access and the mechanics of financial transactions. By digitizing ownership and enabling fractionalisation, it offers accessibility, efficiency and transparency that traditional finance has struggled to deliver. Although regulatory challenges, infrastructure limitations and cybersecurity risks must still be navigated, tokenisation continues to evolve as a pivotal force in the future of investing, broadening participation in global markets while maintaining the core principles of ownership and value.

Please wait processing your request...

Please wait processing your request...