Highlights

- Smart Beta strategies combine elements of both active and passive investing through rule-based factor selection.

- These funds use attributes like value, momentum, and quality to determine portfolio weights instead of market capitalisation.

- Factor-based approaches aim to capture persistent drivers of return while maintaining lower costs than traditional active funds.

- Risks include factor cyclicality, crowding, and tracking differences versus standard benchmarks.

- Smart Beta funds are increasingly used within diversified or multi-factor portfolios to enhance efficiency and risk control.

In recent years, the gap between active and passive fund management has narrowed through the emergence of Smart Beta strategies. These funds combine the transparency and rule-based nature of passive investing with selective exposure characteristics typical of active management.

Smart Beta, also referred to as factor-based investing, follows systematic approaches that seek to capture long-term risk premiums associated with specific market factors. These include metrics such as value, quality, volatility, momentum, size, and yield.

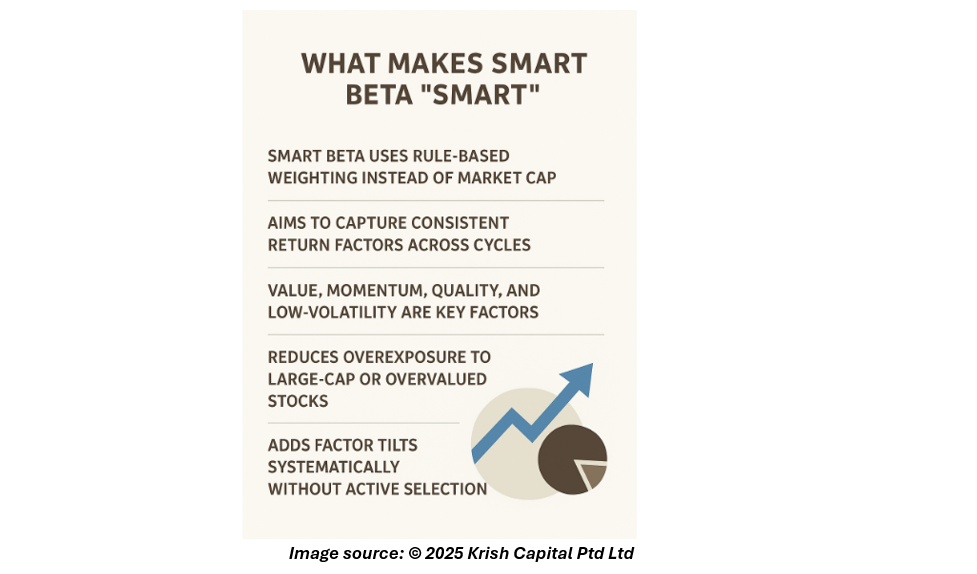

What Makes Smart Beta “Smart”

Traditional index-tracking funds allocate portfolio weights according to market capitalisation, leading to a higher concentration in large-cap stocks. This structure can increase exposure to overvalued companies during extended bull markets.

Smart Beta funds instead assign portfolio weights based on predefined quantitative rules linked to one or more factors. The approach is designed to exploit persistent drivers of return observed across market cycles.

For example, value-oriented Smart Beta strategies focus on securities with low price-to-book or price-to-earnings ratios, while momentum strategies target stocks that have demonstrated recent positive price performance.

Low-volatility strategies select stocks with historically stable price movements, aiming to moderate portfolio fluctuations. Quality-based approaches tilt toward companies with strong balance sheets and reliable earnings.

Through such methodologies, Smart Beta funds systematically introduce factor tilts into portfolios without relying on discretionary security selection

Relevance in Today’s Market

Relevance in Today’s Market

Smart Beta funds have grown rapidly as market participants seek greater efficiency in capturing specific sources of return while maintaining lower fees compared with traditional active funds.

They are often structured as exchange-traded funds (ETFs), offering intraday liquidity and cost transparency. Many institutional allocators use them as portfolio building blocks to align with strategic or tactical allocation goals.

In environments characterised by higher volatility or interest rate uncertainty, factor-based approaches may help align portfolio exposures with desired objectives such as yield enhancement or downside mitigation.

Key Risks and Constraints

Smart Beta approaches are not without limitations. Factor performance tends to be cyclical—certain factors outperform in specific phases of the economic cycle while lagging in others.

Concentration in popular factors can also lead to crowding risk, where similar strategies produce correlated outcomes and reduce diversification benefits.

The complexity of index construction, rebalancing frequency, and weighting methodology can further influence realised returns.

Tracking differences between Smart Beta indices and standard benchmarks may occur due to unique selection and weighting criteria, resulting in performance deviations.

Role in Portfolio Construction

Smart Beta funds are commonly integrated within diversified portfolios to balance risk and return characteristics. They can be combined with traditional market-cap-weighted holdings under a core-satellite framework, allowing targeted exposure to chosen factors.

Multi-factor funds, which blend several attributes such as value, quality, and momentum, have become popular for their potential to reduce performance volatility across economic cycles.

The systematic and evidence-based nature of Smart Beta strategies aligns with broader trends in quantitative portfolio management and data-driven allocation design.

Outlook

Smart Beta funds now represent a significant and growing segment of the global ETF market. Continuous innovation is leading to the development of ESG-integrated and AI-enhanced Smart Beta indices aimed at improving risk control and sustainability alignment.

As the fund management landscape evolves, Smart Beta strategies continue to bridge the traditional divide between active and passive methods, offering structured exposure to well-researched factors that influence long-term asset performance.

Please wait processing your request...

Please wait processing your request...