Highlights

- Financial services are shifting from standalone platforms to embedded digital experiences

- Digital wallets act as centralized interfaces for payments, security, and financial tracking.

- Neobanks emphasize simplicity, speed, and mobile-first financial access.

- Embedded finance integrates banking functions directly into non-financial platforms.

- The future of finance is increasingly driven by usability, integration, and ecosystem partnership.

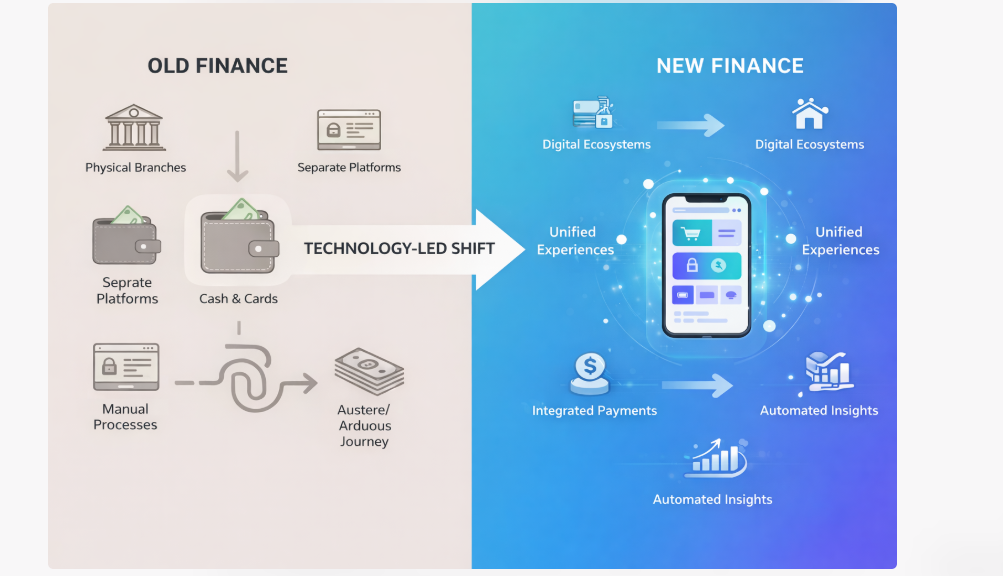

The global financial ecosystem is undergoing a structural shift driven by technology-led models rather than traditional banking boundaries. Digital wallets, neobanks, and embedded finance are redefining how individuals and businesses access, use, and experience financial services. Instead of finance being confined to physical branches or standalone platforms, it is increasingly integrated into digital environments where daily activity already occurs. Understanding these developments provides insight into how financial services are becoming more accessible, modular, and user-centric across the global economy.

Digital Wallets: Redefining How Money Is Stored, Moved, and Secured

Digital wallets represent the shift from physical money management to software-driven financial interaction. At their core, digital wallets allow users to store payment credentials securely and execute transactions electronically, using devices such as smartphones, tablets, or computers. Rather than carrying cash or cards, users rely on encrypted digital interfaces to pay, receive, and manage money.

A key strength of digital wallets lies in convenience. Payments can be completed within seconds, whether for online purchases, in-store contactless payments, or peer-to-peer transfers. By consolidating multiple payment methods—cards, bank accounts, and sometimes even digital assets—into a single platform, digital wallets reduce friction in everyday financial activity.

Digital wallets can be grouped based on how they store and move value. Closed wallets operate within a single platform and are mainly used for purchases or refunds. Semi-closed wallets work across a network of partnered merchants but usually do not allow cash withdrawals.

Open wallets, often linked with regulated financial institutions, support broader functions such as transfers, bill payments, and withdrawals. In addition, crypto wallets are designed to store and manage digital assets, enabling users to send, receive, and safeguard cryptocurrencies independently of traditional banking systems.

Modern digital wallets are built with layered security mechanisms, including encryption, tokenization, and user authentication. Sensitive information is not shared directly during transactions, lowering exposure to fraud while maintaining a smooth user experience. This balance between speed and security has been central to their widespread adoption.

Digital wallets are increasingly evolving beyond simple payments. Many now support bill payments, subscriptions, loyalty programs, and financial insights, positioning themselves as everyday financial companions rather than standalone payment tools.

Neobanks Redefining Banking Through Digital-First Models

Neobanks are financial institutions that operate exclusively through digital platforms, offering banking services without relying on physical branch networks. Their growth has accelerated in recent years as customers increasingly seek faster, simpler, and more accessible ways to manage their finances. By operating entirely online, neobanks are able to design services around digital-first customer behaviour rather than traditional branch-based models.

A defining feature of neobanks is their emphasis on convenience and user experience. Most services—from opening accounts to transferring funds—are designed to be completed through mobile applications or web platforms.

Neobanks commonly provide products such as savings accounts, payment services, and basic investment tools, supported by modern technology that enables real-time transactions and streamlined account management. Features like automated savings tools and competitive interest structures further distinguish them from traditional banking models.

The appeal of neobanks lies largely in their simplicity. Customers can monitor balances, track spending patterns, and move funds quickly without the administrative processes often associated with branch-based banking.

This digital efficiency resonates particularly with users who prefer managing finances through a limited number of intuitive platforms rather than navigating complex banking systems. As a result, neobanks align closely with changing consumer expectations around speed, transparency, and ease of use in financial services.

Embedded Finance: Bringing Financial Services Closer to Daily Transactions

Embedded finance refers to the integration of financial services directly into non-financial products, platforms, and digital experiences. Instead of accessing banking or payment services through a separate financial institution, users can carry out financial activities within applications and services they already use in their daily lives. This model shifts financial interactions closer to where purchasing, usage, and engagement naturally occur.

Through embedded finance, activities such as payments, lending, insurance, or account services become part of a broader digital journey rather than standalone processes. This reduces the need for customers to switch between multiple platforms to manage financial tasks, creating a more streamlined and intuitive experience. As a result, financial services are increasingly becoming an invisible but integral layer within digital ecosystems.

The rise of embedded finance has also enabled non-financial brands to expand their offerings without becoming financial institutions themselves. By partnering with specialized providers, these platforms can integrate regulated financial capabilities while focusing on their core products and customer experience. This approach allows brands to enhance user engagement and deliver added value without managing the regulatory and operational complexity traditionally associated with financial services.

Embedded finance reflects a broader shift toward convenience-driven financial access, where banking functions are woven into everyday digital interactions rather than confined to dedicated financial platforms.

Image Source: © 2026 Krish Capital Pty. Ltd.

The Evolving Architecture of Modern Finance

The rise of digital wallets, neobanks, and embedded finance signals a broader transformation in how financial services are delivered and consumed. Rather than replacing existing institutions outright, these models are reshaping financial access by prioritizing speed, integration, and usability.

Traditional financial infrastructure continues to play a foundational role, while new digital layers redefine customer interaction and distribution. Together, these developments illustrate a future where finance is less about where banking happens and more about how seamlessly it fits into everyday digital life. As financial ecosystems continue to evolve, adaptability and integration will remain central to their long-term relevance

Please wait processing your request...

Please wait processing your request...