Key Highlights

- Energy (XLE) is the primary market leader, driven by a 35% spike in oil prices following geopolitical tensions in the Strait of Hormuz.

- The market narrative has pivoted toward stagflation, favoring "Hard Assets" over interest-rate-sensitive sectors.

- Information Technology (XLK) is facing a valuation squeeze as rising 10-year Treasury yields punish high-growth names.

- Institutional capital is rotating into the "real economy," keeping Materials (XLB) and Industrials (XLI) in leading positions.

The US equity markets have entered a period of intense turbulence as of March 12, 2026. While the broader indices face significant pressure from climbing Treasury yields, the market exhibits a clear "stagflation-style" pricing characteristic, where certain "real asset" sectors are thriving while interest-rate-sensitive groups remain highly vulnerable.

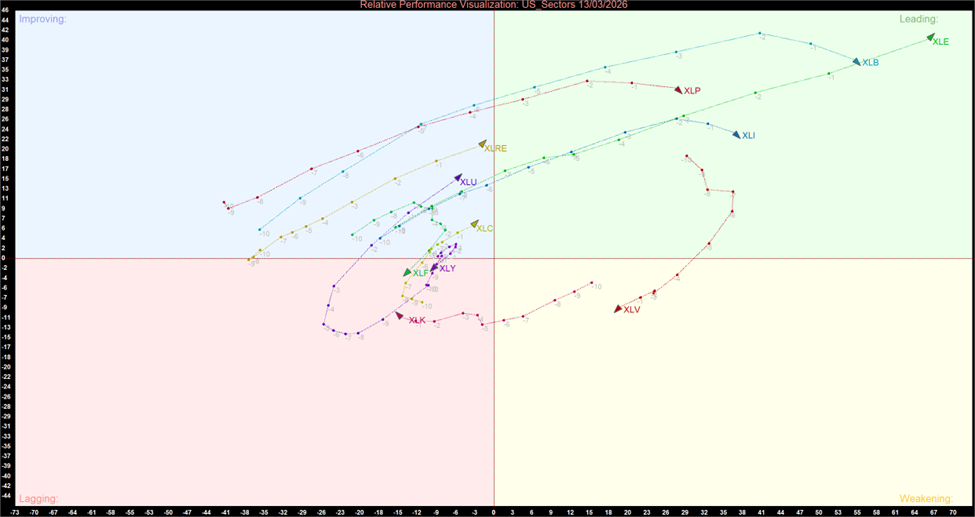

US Sector Weekly Momentum chart

US Sector Weekly Momentum Chart (at the closing price of 13th March 2026). Powered by: amibroker.com

US Sector Weekly Momentum Summary Table

Leading Quadrant: The "Real Economy" Dominance

- Energy (XLE): Positioned as the absolute market leader, Energy is accelerating furthest into the leading quadrant. This outperformance is driven by a massive "geopolitical risk premium" as crude oil prices spiked 35% in the first 12 days of March due to escalating tensions in the Strait of Hormuz.

- Materials (XLB) & Industrials (XLI): These sectors maintain firm positions in the leading quadrant. They are benefiting from a broad structural rotation into the "real economy" as institutional capital flees "paper" growth assets in favor of tangible industrial hedges.

- Consumer Staples (XLP): Acting as a preferred defensive anchor, this sector is showing resilience in the leading quadrant, outperforming on a relative basis as investors seek shelter during the broad market sell-off.

Weakening & Lagging: The Yield Victims

- Information Technology (XLK): Currently deep in the lagging quadrant, Tech is facing the sharpest negative trajectory. The sector is suffering from a "valuation squeeze" as the 10-year Treasury yield hit a five-week high of 4.25%, reducing the present value of future cash flows for high-multiple growth names.

- Consumer Discretionary (XLY): Stuck in the lagging quadrant, this sector is being hammered by soaring gasoline prices and sticky inflation, which are threatening to aggressively squeeze household spending.

- Health Care (XLV): After showing previous strength, this sector has dipped into the weakening quadrant as momentum fades and capital rotates toward more direct energy-linked hedges.

Improving Quadrant: Potential Leaders

- Financials (XLF): This sector is trending upward as markets price in a "higher-for-longer" interest rate environment. Despite some jitters in private credit markets, the hawkish tilt of the Fed is providing a relative boost to banking margins.

- Real Estate (XLRE) & Utilities (XLU): Both are attempting to stabilize within the improving quadrant. However, they remain highly sensitive "bond proxies" that are vulnerable to further structural liquidation if bond yields continue to climb.

Bottom Line

The market narrative has shifted from "soft landing" optimism to stagflation fears. For investors, the immediate path forward requires a defensive focus on "Hard Assets" like Energy and Materials while remaining extremely cautious of high-duration growth sectors that are being punished by the current yield shock.

_03_16_2026_07_57_11_233658.jpg)

Please wait processing your request...

Please wait processing your request...