Key Highlights

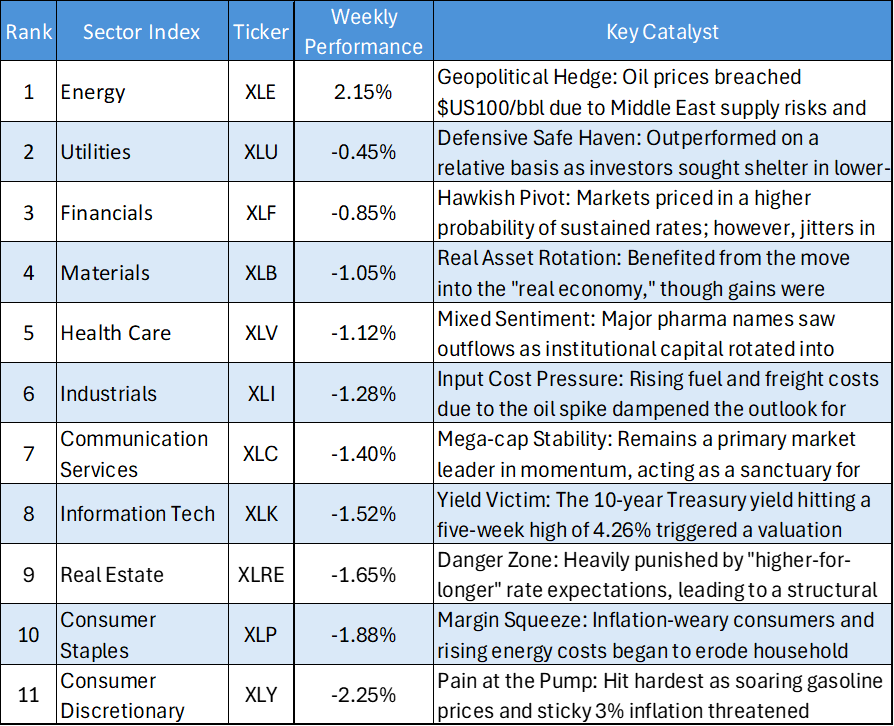

- Energy (XLE) surged as a primary geopolitical hedge while oil prices breached the $US100/bbl mark.

- The 10-year Treasury yield climbed to a five-week high of 4.26%, triggering a massive re-rating in high-growth sectors.

- Markets aggressively priced in a "higher-for-longer" interest rate environment, significantly dampening expectations for 2026 rate cuts.

- Growth-focused sectors like Information Technology (XLK) and Real Estate (XLRE) bore the brunt of rising capital costs.

The US equity markets faced a volatile and challenging period during the week ending March 13, 2026, characterized by a "geopolitical energy shock" that rattled investor confidence. While the broader indices struggled under the weight of surging inflation fears, a distinct rotation into "real assets" created a sharp divide in sector performance.

The "Hormuz" Premium and Fed Anxiety

- The defining narrative of the week was the escalation of conflict in the Middle East, with threats to the Strait of Hormuz sending Brent Crude as high as $101.59 per barrel. This spike in energy costs immediately reignited domestic inflation fears, forcing a "hawkish" shift in market sentiment.

- Investors reacted by pushing back forecasts for Federal Reserve rate cuts, with some officials now indicating that further hikes could be necessary if inflation remains sticky near 3%. This macro backdrop sent the S&P 500 plummeting 1.5% in a single session, erasing previous gains and returning the market to a state of high volatility.

US Sector Performance Breakdown

Energy (XLE): The Undisputed Alpha Leader (+14.20% YTD)

Energy remains the sole outlier and primary beneficiary of global instability.

- Integrated Majors: Exxon Mobil (XOM) and Chevron (CVX) saw heavy inflows as traders sought leveraged plays on surging commodity prices.

- Risk-Adjusted Performance: Despite high volatility, the sector maintains the highest Sharpe Ratio (0.42) in the market, suggesting genuine outperformance driven by the "geopolitical premium".

Information Technology (XLK): The High-Beta Yield Victim

As bond yields spiked, the Tech sector exhibited a classic "high-risk, low-reward" profile.

- Valuation Squeeze: High-growth software companies faced a "meltdown" as rising rates reduced the present value of future cash flows.

- Negative Sharpe Ratio: With a YTD return of -0.40% and a negative Sharpe Ratio of -0.12, investors are currently not being compensated for the extreme price swings in this sector.

Real Estate (XLRE): The Structural Liquidation Zone

Real Estate continues to be the market's "danger zone," mirroring the structural exit seen in international property markets.

- Worst Performer: The sector has posted a staggering -8.90% YTD return.

- Yield Sensitivity: A Sharpe Ratio of -0.58 reflects intense pressure on property valuations as debt servicing costs rise alongside the 10-year yield.

Financials (XLF): Bracing for Credit Jitters

The narrative for banks shifted violently as traders prepared for sustained high rates and potential liquidity issues.

- Private Credit Fears: Jitters in the $2 trillion private credit market added to interest rate

- Liquidity Concerns: Significant redemptions at private income funds, such as those seen at Morgan Stanley, sparked widespread concern over institutional stability.

Weekly Market Summary

The US market has shifted from "soft landing" optimism to a cautious defensive stance dominated by stagflation fears. While Energy and Materials thrive as hedges against geopolitical shocks, the "duration risk" posed by high yields is currently crushing growth-focused sectors. Investors are increasingly fleeing "paper" assets in favor of the "real economy," leaving interest-rate-sensitive groups highly vulnerable in the near term.

_03_16_2026_07_57_11_233658.jpg)

Please wait processing your request...

Please wait processing your request...