Cochlear Limited

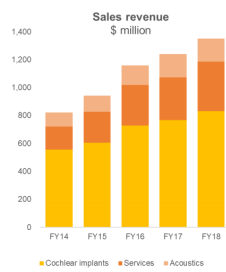

Retain Market Leadership Position: Cochlear Limited (ASX: COH) is into the sale and manufacturing of Cochlear implant systems with the market capitalisation of ~A$11.46 Bn (as at 29 May 2019). On 10th May 2019, the company, by release, announced that it had hosted analysts to its annual capital markets day and highlighted about strategic priorities and innovation pipeline. In the release, the company mentioned that investment in R&D strengthens its market leading technology position. It had continued its R&D investment of ~12% of revenue. Moreover, since listing, COH had made an investment of more than $1.7Bn in R&D and maintained net profit margin over the period. The company mentioned the key growth drivers of revenues, which includes Cochlear implants,Services and Acoustics.With respect to Cochlear implants, there isgrowing awareness and uptake by adults and seniors.

Sales Revenue Growth (Source: Company Reports)

The company is investing its operating cash flow to drive growth. It is investing to grow and is creating awareness and access to its products. By disciplined investment, it would maintain the net profit margin. It aims to maintain a strong balance sheet position. Adding to that, it continues to target a dividend payout ratio of circa 70% of net profit.

Upgrade revenue witnessed a rise of 26% in CC (constant currency) and there is strong uptake of Nucleus® 7 Sound Processor. The Cochlear implant units increased by 5%.Post expansion of indications and funding, the company witnessed strong growth in Japan. The company is investing to grow on track and is increasing focus on the standard of care initiatives. Its focus is on deployments towards R&D to advance long-term technology development pipeline. The company stated that the robust cash flow generation is supporting an 11% increase in the interim dividend.

What to Expect from COH: The company is maintaining net profit projection in the range of $265-$275Mn for the full year 2019. The revenue growth would be driven by the services business, with strong uptake of the Nucleus 7 sound processor mainly in the first half. It anticipates a lower rate of Cochlear implant growth throughout the developed markets for FY 2019. The company is expecting a weighted average AUD/USD exchange rate of 72 cents for FY19 in comparison to 77 cents in FY18. It is forecasting AUD/EUR of 0.63 EUR in FY19.

Stock Recommendation: The company is planning to continue its investment to hold market leadership and to drive long-term market growth along with the target of maintaining the net profit margin. The emerging market growth rates over the time would continue to be strong but annual growth rates could be variable due to the timing of tender based activity and macro-economic conditions.

With respect to stock’s past performance, it had witnessed a rise of 8.50%, 16.45% and 17.88% in the time span of one-month, three months and six months, respectively. As per the Australian Securities Exchange, the company’s stock price is trading slightly towards the 52-week higher levels of $221.440 with higher PE multiple of 43.38x. Hence, considering the above factors and the current trading level, we uphold our “Expensive” recommendation on the stock at the current market price of A$198.460 per share (down 0.045% on 29 May 2019) and suggesting investors to wait for few more trading sessions to get the better entry level.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...