XERO Ltd

.png)

XRO Details

1H16 depicting ongoing subscriber’s growth: XERO FPO NZ (ASX: XRO) reported a total revenue growth of 71% year on year (yoy) to $92.86 million in first half of 2016 and reported a subscription revenue rise by 72% yoy to $89.75 million. Gross margin improved to 74% during the period as compared to 67% in prior corresponding period (pcp) and 72% in 2H15. The group reported a paying subscriber’s base increase of 60% yoy to 593,000 during the first half. The total Australian subscribers and New Zealand subscribers rose by 66% and 37% to 262,000 and 163,000 respectively. The group crossed 100,000 paying subscribers in United Kingdom during 1H16, which rose by 67% yoy to 102,000. Xero also enhanced its North American subscribers by 114% yoy to 47,000 in 1H16. Although the group’s overall subscriber churn was stable at 1.3%, it fell across international markets indicating the group’s sustainable performance. Xero also invested heavily in R&D ($22.5 million) to maintain competitive advantage while its product design and development costs increased by 90% yoy to $50.5 million during 1H16. Moreover, the group reiterated its subscription revenue estimate to be more than NZ$200 million for 2016 fiscal year (as per June 2015 FX rates).

Financial Achievements (Source: Company Reports)

The group also earlier forecasted that its recurring revenue model which is implemented in 2016, would generate a year over year growth of 71% in annualized committed monthly revenue of $159.3 million in 2016 fiscal year. The shares of XRO has delivered year to date returns of 13.49%, and surged over 17.02% (as of November 17, 2015) from the last four months alone. We remain bullish on the stock given its growth potential and accordingly reiterate our “BUY” recommendation at the current price of $18.20

Graincorp Ltd

.png)

GNC Dividend Details

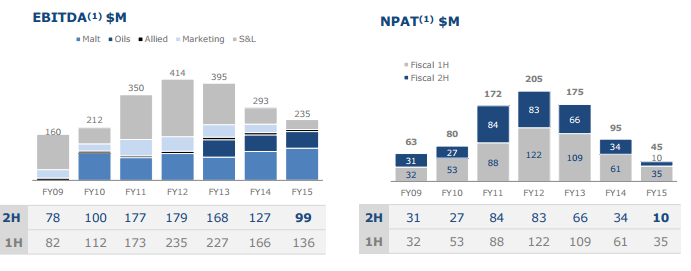

Poor marketing result and intense competition: Graincorp Ltd (ASX: GNC) reported its results with underlying NPAT of $ 45 million and statutory NPAT of $ 32 million as well as underlying EBITDA of $ 235 million with regards to FY15. Managing director and CEO Mark Palmquist said that it was pleasing that the processing business had contributed to a significant part of the year’s expected earnings. The results have been affected by continuing challenges in the global grain market which is only be partly offset by opportunities in storage and logistics. The company expects to report sales volume for Marketing of 6 mmt, full-year EBITDA loss of $ 2 million compared to the first half gain of $ 8 million, and full-year PBTDA loss of $ 16 million compared to the first half loss of $ 1 million. The FY15 earnings depict a blatant difference in the grain supply chain and trading businesses (with combined PBT loss of $29.7m) and its processing divisions (with combined EBIT of $142m). The grain supply chain and trading divisions’ seems to be affected by the competitive pressures in the industry. Further, lower grain production in eastern Australia is reported to have resulted in intense competition. The position was exacerbated by lower fuel costs and ocean freight rates which reduced the freight advantage that Australia has in exporting to major markets. The performance of Storage and Logistics was modest even in a tough environment because of improvements in cost management and a strong sorghum export program.

Earnings Profile (Source: Company Reports)

The harvest update from forecasters is 16.1 mmt of winter crop for eastern Australia. The eastern Australian harvest is now underway and the company has already received 1.4 mmt mostly in Queensland and northern New South Wales. Hot and dry conditions prevailed in Victoria and southern New South Wales in September and October which may affect grain production forecasts relating to FY 2016. The company saw its share price sliding on the announcement of the expected results because of the decline in the earnings. Wheat futures have also said to be declined by 14% on the Chicago Board of Trade and global inventory expected to climb to the highest level in almost 30 years. We believe that the expected profit growth for FY 2016 combined with the expectation of FY 2015 does not warrant the price at which the stock is now trading. GNC may also be affected by the upcoming largest competing port (Quattro Grain JV at Port Kembla) set to be open in May 2016.

Overall, we find the stock to be expensive at the moment.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people.Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation.Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product.The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2014 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.

AU

AU

Please wait processing your request...

Please wait processing your request...