Aveo Group

.png)

AOG Dividend Details

Focusing on retirement living: Aveo Group (ASX: AOG) total retirement contribution rose 18% year on year (yoy) to $53 million during fiscal year of 2015, as the group’s retirement strategy has been paid off with the group generating over 721 of the total retirement unit sales. Consequently, Aveo reported a 30% increase of underlying net profit after tax of $54.7 million while Funds from operations rose by 88% yoy to $73.9 million, or 14.8 cents per security. Net assets per security improved by 3% to $2.85. Aveo Group has been diversifying its portfolio and built a solid pipeline of 182 new units scheduled for delivery in the next year. The group estimates a 45% increase of its underlying profit after tax during FY16 to over $80 million, and a total year distribution of 8 cents per security, representing a 60% increase on the distribution during FY15.

Aveo Group’s retirement asset returns (Source: Company Reports)

Aveo Group’s shares surged over 33.80% during this year to date (as at December 15, 2015) and we believe the stock would continue to rally in the coming months. Based on the foregoing, we give a Buy recommendation at the current price of $3.03

AOG Daily Chart (Source: Thomson Reuters)

BWP Trust

Lease terms nearing to expiry for some properties: BWP Trust (ASX: BWP) stock surged over 8.21% during this year to date (as of December 15, 2015) and recently reported a $176 million or 8.9% increase of the value of its portfolio of 82 properties to $2.158 billion for the half year ended on December 2015, as compared to the portfolio value in June 2015. BWP reported a decent FY15 performance as well and improved its total income to $144.9 million in fiscal year of 2015, against $127.4 million in prior corresponding period (pcp). However, investors need to note that around ten Bunnings lease terms would be expiring in the next three years.

Bunnings lease term expires in the next three years (Source: Company Reports)

Accordingly, the stock corrected over 2.88% in the last six months (as at December 15, 2015) and we believe the pressure in the stock would continue in the coming months. We reiterate our Expensive recommendation on the stock at the current price.

BWP Daily Chart (Source: Thomson Reuters)

Cedar Woods Properties Ltd

.png)

CWP Dividend Details

Solid dividend yield: Cedar Woods Properties Limited (ASX: CWP) stock plunged over 33.85% during this year to date (as at December 15, 2015) impacted by the subdued investor’s sentiment on Western Australia exposed firms coupled with tough market conditions for real estate. Moreover, with the initial call-in of the Upper Kedron project by the Queensland State Government further contributed to the negative sentiment. On the other hand, the Queensland Government currently approved the first 480 lots of the development to the group. CWP built a strong pre-sales of $184 million during the first quarter of 2016 and the residential property market in Western Australia, Victoria and Queensland are recovering. The group reported a net profit after tax of $42.6 million during fiscal year of 2015, which is 5.6% better than fiscal year of 2014. Management estimates its net profit after tax for FY2016 to be similar to that of FY15 net profit.

.png)

Developing a pipeline of projects leading to a better earnings visibility (Source: Company Reports)

Meanwhile, the heavy correction in the stock also placed CWP shares at very lower valuations, which is trading at a cheap P/E. CWP also has an outstanding dividend yield. Based on the foregoing, we give a Buy recommendation on the stock at the current price of $3.87

CWP Daily Chart (Source: Thomson Reuters)

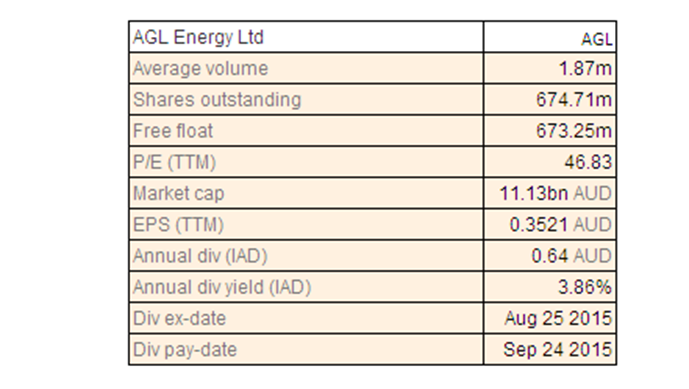

AGL Energy Ltd

AGL Dividend Details

Winning the Gas Storage Services Agreement: AGL Energy Ltd (ASX: AGL) announced that it has secured long-term gas storage rights utilising the Iona Gas Storage Facility by entering into a 15 year Gas Storage Services Agreement. The arrangement provides the ability to optimise gas supplies for storing gas during low demand periods for reuse during peak demand periods (largely in the winter). This will result in a more than 30% reduction in costs to manage seasonal demand. For the financial year 2015, the company reported a statutory net profit after tax of $ 218 million, a drop of 62% on the results for the previous year at the back of the effect of significant items including impairments and transaction costs associated with the acquisition of the Macquarie Generation power stations. For many years, the company has used underlying profit to provide more meaningful tracking of company performance and this is calculated by excluding significant items and the “mark to market” impact of the large hedging positions. The impact of the impairment of some gas assets is more notable and a number of factors contributed to the negative revaluations. There were also adjustments in reserve calculations to Gloucester. The underlying net profit after tax was $ 630 million, up 12.1% on the previous year. The fully franked final dividend of $ 0.34 per share added to the interim dividend of 30 cents per share leading to 64 cents per share fully franked. Assuming normal trading conditions, underlying profit for the year ending 30 June 2016 is expected to be in the range of $ 650 million-$ 720 million.

This is subject to factors including contribution from AGL Macquarie, residential electricity consumption and rise in new energy operating loss. The stock has delivered returns of 22.42% this year to date (as at December 15, 2015). The recent news about Executive General Manager New Energy, Marc England, leaving the company to take up the Chief Executive Officer position at Genesis Energy in New Zealand will let AGL look for a permanent replacement. We would rate the stock as a Hold at the current price.

AGL Daily Chart (Source: Thomson Reuters)

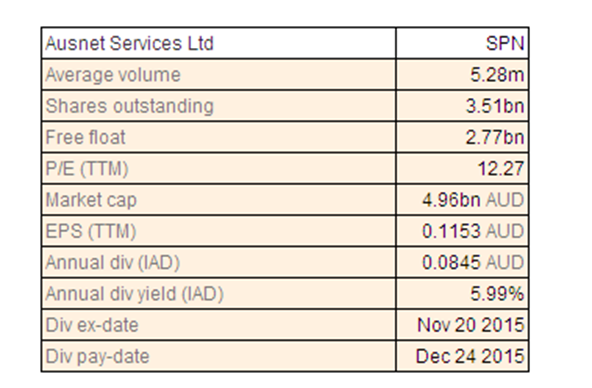

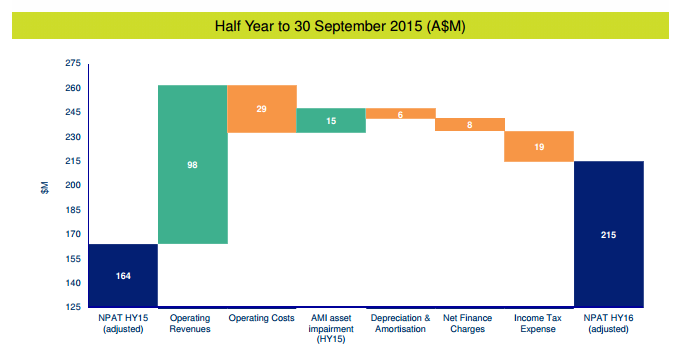

AusNet Services Ltd

AST (SPN) Dividend Details

Revenue growth driven by electricity price rise and seasonal change: AusNet Services Ltd (ASX: AST) witnessed a 10% increase in revenues to $ 1.06 billion, 22.9% in EBITDA to $ 650.4 million and a net profit after tax of $ 374.5 million for the half yearly results for the period ended 30 September 2015. Net profit after tax got an impact from tax consolidation outcome arising from legal entities restructuring amounting to $ 132 million, tax benefit relating to intellectual property dispute settlement and amounting to about $ 20 million, an impact of ATO audit settlement relating to the order of $ 143 million and Advanced Metering Infrastructure customer rebate provision of $ 38 million. Electricity distribution reported segment revenue of $ 530.6 million, up 18.5% over the pcp and EBITDA of $ 332.6 million, up 55.6% over the pcp. The volume in GWh is 4067, up 5.4% over the previous corresponding period. Connections at 685,435 are up by 1.8%.

Financial Performance (Source: Company Reports)

Revenue growth has been driven by a combination of regulated price increases for both electricity distribution and AMI and a cooler six-month period to 30 September 2015 compared to the previous year. There has been a change in the spending pattern for as a replacement with the previous year including a greater proportion of spending in the first half, compared to the forecast for the current year though this decline is offset somewhat by $ 17 million expenditure on the metering program. In terms of the future outlook, the company will continue to determine future dividends from operating cash flows after servicing all of its maintenance capital expenditure and a portion of the growth capital expenditure.

For FY 2016, the company expects to increase dividends by 2% to 8.53 cents per share and final dividend is said to be 100% franked. The stock has surged 6.79% this year to date but fallen 4.71% in the last five days (as at December 15, 2015). We consider the stock to be expensive at the current price.

AST Daily Chart (Source: Thomson Reuters)

Spark Infrastructure Group

.png)

SKI Dividend Details

Entering into new bilateral corporate debt facilities: Spark Infrastructure Group (ASX: SKI) plummeted 11.21% this year to date (as at December 15, 2015). The company along with its consortium partners under NSW electricity networks have announced the purchase of TransGrid for $10.3bn (including $134m in transaction costs). The company also announced about entering into $ 250 million of new bilateral corporate debt facilities, replacing its previous ones. The new three year and five-year facilities for $ 225 million and $ 25 million respectively, have been entered into with CBA, Westpac and Bank of Tokyo Mitsubishi UFJ. In line with previous arrangements, these facilities will provide flexibility for general corporate funding purposes. The group intends to deliver steadily growing distribution to its security holders over a period of time and consistent performance in returns from investments are based on business plans, which are sufficiently robust and flexible. The directors have provided distribution guidance for FY 2016, which is the first full year under the new regulatory periods, of 12.5 cents per share subject to business conditions.

For FY 2015, dividends per share amounted to 6 cents per share, which is a growth of 4.3% over the previous year. The stand-alone payout ratio was 87% compared to 97.3% and the look through payout ratio (post net costs) was 52.9% compared to 63.6%. Net debt to RAB at asset company level was 76.2% compared to 77.8% and the underlying net profit after tax was $ 70.8 million compared to $ 67.5 million. We think that the company’s performance has been significant and that future prospects give plenty of scope for stock price. Accordingly, we would recommend Buy for the stock at the current price of $1.86

.png)

SKI Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people.Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation.Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product.The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2014 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.

AU

AU

Please wait processing your request...

Please wait processing your request...