.png)

Stocks’ Details

THE A2 MILK COMPANY LIMITED (ASX: A2M)

Accelerated new product development: The Company lately issued 2,500,000 of ordinary shares (500,000 partly paid ordinary shares and full payment of 2,000,000 partly paid ordinary shares). The issue price for the 500,000 ordinary shares was NZ$0.55 per share of which NZ$0.0055 per share had been paid previously; and for 2,000,000 ordinary shares, the issue price was NZ$0.64 per share of which NZ$0.0064 per share had been paid previously on issue as partly paid ordinary shares. Nutritional products have been developed by the group that will be launched in FY2018 and will include a2 Platinum pregnancy formula. It will also increase its investment in marketing across Asia and Northeast USA. It is assessing its expansion opportunities in other markets, particularly in Asia. The Company entered a comprehensive strategic relationship with Fonterra Co-operative Group Limited and will supply A1 protein-free nutritional products in bulk. A2M granted strategic customer rights with committed capacity arrangements with offtake flexibility while Fonterra granted an exclusive licencing arrangement for the launch of a2 Milk branded fresh milk in New Zealand which will cover its production, distribution, sale and marketing. The Revenue and Gross margin for 1HY18 was 70 per cent and 82 per cent higher as compared to 1HFY17. It is now expected that marketing investment will exceed in 2H18 by ~NZ$35 as compared to 1H18, which will be driven by an increase in expenditure in China and USA. The stock prices were up by 139 per cent in the past six months and by 11.62 per cent in the past one week.While the stock looks “Expensive” at the current price of $12.9 we keep an eye on any substantial price dip.

.png)

Revenue Performance (Source: Company Reports)

BELLAMY'S AUSTRALIA LIMITED (ASX: BAL)

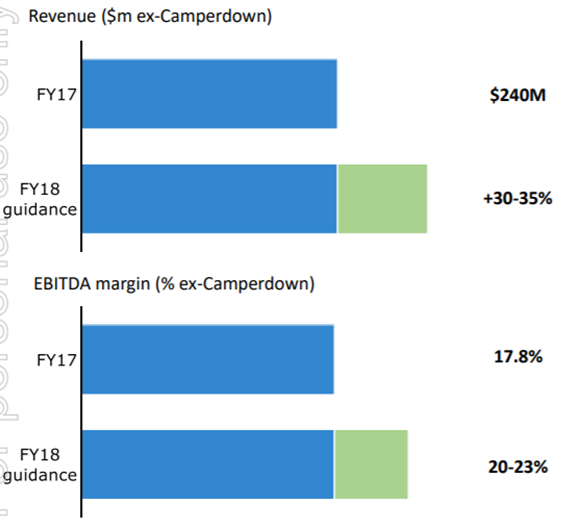

Focusing on long-term growth plan: Bellamy’s has been performing well lately and was added to S&P / ASX 200 Index and S&P / ASX All Australian 200 Index effective March 19, 2018. Meanwhile, Delta Partners, LP, a substantial holder of Bellamy’s changed its holding from 9.68 per cent of interest to 10.14 per cent. Bellamy’s turnaround remained on track and the underlying health of the business continued to strengthen the performance. The Revenue and Gross Profit for 1HFY18 was $170 million and $63 million whereas in 1HFY17 Revenue and Gross Profit was $118.3 million and $46.8 million, respectively. The overheads were down as compared to the prior year which was driven by lower inventory levels, logistic rates and restructuring of logistic network. It upgraded the forecast of FY18 revenue growth and EBITDA margin that is now between 30-35 per cent and between 20-23 per cent, respectively. Its focus is to obtain CFDA license and to execute a long-term growth plan. The share prices were up by 176 per cent in the past six months and by 6.13 per cent in the last week. We give a “Hold” recommendation at the current market price of $21.03

FY18 Guidance (Source: Company Reports)

BLACKMORES LIMITED (ASX: BKL)

Supply challenges impacting the Performance: Blackmore’s balance sheet is in a strong position with a 63 per cent of improvement in cash generated from the operations as compared to the same time last year that was driven by the improved working capital management. Net Debt was $66 million, that is increased by $21 million since June 2017 and this increase was due to the purchase of shares related to Blackmores first three-year executive long-term incentive awards. Gearing levels were at 27 per cent and Blackmores maintains a conservative level of headroom against all bank covenants. The Board declared an interim dividend of 150 cents per share fully franked, which is an increase of 15% as compared to the prior corresponding period and will be paid on 22 March 2018. Continuity of supply has been a challenge in the second quarter as suppliers have struggled to respond to its increased requirements. This is expected to impact the second half of 2018. Group’s first half revenue was up by 9 per cent as compared to the same period in the prior year. However, net Debt increased by $21 million since June 17. The stock price was up by 13.5 per cent in the past six months but declined by 15.7 per cent in the past one month. Despite the decline, the stock looks “Expensive” at the current market price of $135.91

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...