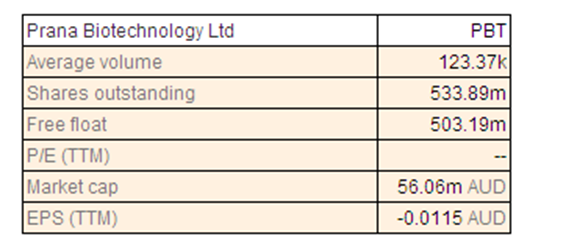

Prana Biotechnology Ltd

PBT Details

Portfolio development on high but tumbled 47.50% this year to date: Prana Biotechnology Ltd (ASX: PBT) stock has fallen 47.50% this year to date (as at December 14, 2015) even while having a good product pipeline. The portfolio of the company consists of PBT2 for Huntington disease, PBT2 for Alzheimer's disease, PBT434 for Parkinsonian diseases and the MPAC library. PBT2 has completed four phase 1 trials and four phase 2 trials with good recruitment, high retention and completion rates. It was reviewed by the Independent Data Safety Monitoring Board and no safety concerns were identified for changes to the protocols. Based on this robust safety profile, a robust safety monitoring plan for future trials in HD is being developed for the FDA. However, despite the clinical safety demonstrated to date, the FDA has placed a Partial Clinical Hold based on non-clinical findings in dog studies. The response to FDA based on reports from specialist clinical safety physicians should be submitted in early 2016. PBT2 has been granted Orphan Drug designation for Huntington’s disease by both the US FDA and the European Commission. With this designation, the company gets an extended seven years of market exclusivity in the US and 10 years in Europe with reduced fees in applying for market approval. The need for treatments for neurodegenerative diseases continues to be critical and the company remains committed to further development of its portfolio.

The cash position continues to be satisfactory with $ 33 million in cash at hand as of 30 September 2015. However, we do note that the company reported a 51% drop in the full year revenue for FY15. We believe that there is more to be done for developments to justify the current high price of the stock and would therefore regard the stock as “expensive” at the moment.

PBT Daily Chart (Source: Thomson Reuters)

Mesoblast Ltd

MSB Details

Pricing notification for TEMCELL® received: Mesoblast Ltd (ASX: MSB) The company has announced that its licensee in Japan, JCR Pharmaceuticals Co Ltd, got the notification from the Japanese government’s National Health Insurance body for formally setting the price for the mesenchymal stem cell product TEMCELL®. The licensee announced that the product for the treatment of acute graft versus host disease (aGVHD) is anticipated in February 2016. Under the agreement, the company is entitled to receive royalties and other payments at predefined thresholds of cumulative net sales. The company expects reimbursement for treatment course of the product in an adult Japanese patient at $ 156,000 or up to $ 234,000. In the United States, the company believes that it is well positioned to have the first industrially manufactured allergenic cell-based product approved with its product candidate for the treatment of steroid refractory aGHVD in children.

.jpg)

% Responder Rate (Source: Company Reports)

The company seeks to complete recruitment for its open-label 60 patient phase 3 trial in the fourth quarter of 2016 and the interim analysis may support a Biologics License Application regulatory filing by the end of 2016. The company has also announced that the board and management are committed to delivering the Tier 1 product milestones set out in the F-1 registration statement using the existing cash reserves including the proceeds raised by listing on NASDAQ.

We are convinced that the company is showing satisfactory progress in developing its products and the recent NASDAQ listing should broaden the appeal of the stock. The stock has corrected about 67.95% this year to date (as at December 14, 2015) and this may be an opportunity for investors having an appetite for risk. In view of a long term potential, we would recommend a “Buy” at the current price of $1.55

MSB Daily Chart (Source: Thomson Reuters)

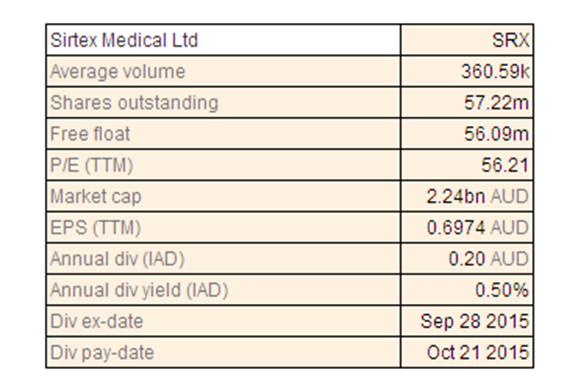

Sirtex Medical Ltd

SRX Dividend Details

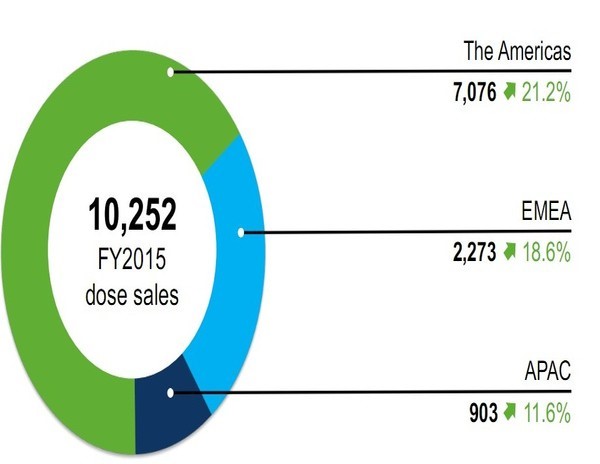

Compelling shareholder return: Sirtex Medical Ltd (ASX: SRX) stock is trading close to its 52 week high price and has returned about 36.55% this year to date (as at December 14, 2015). The stock has also been added in the S&P /ASX 100 Index as per the S&P Dow Jones’ December 2015 quarterly rebalance of S&P /ASX Indices. FY 2015 has been an important year in the history of the company and represents another 12 months of substantial delivery of results. The company achieved record growth in dose sales of SIR-Spheres® Y-90 present microsphere product in addition to record revenues, record operating cash flows and record profits. Primarily, dose sales surged 19.8% to 10,252 units while total revenue rose by 36.1% to $ 176.1 million with net profit after tax rising by 69% to $ 40.3 million.

FY15 Dose Sales (Source: Company Reports)

The company has been creating value for its shareholders and the total shareholder return for FY 2015 (with dividends) was 72.9% while the average annual return including dividends to shareholders over the last five years has been a substantial 69%. Also, the market capitalisation surged above the $1 billion value. SRX’s SIRFLOX study has demonstrated that SIR-Spheres Y-90 when combined with standard chemotherapy could curb growth progression of life tumours by an additional 7.9 months compared to chemotherapy alone. Expansion of manufacturing capacity with a tripling of capacity at the Boston facility and the construction of the newest facility in Frankfurt set to supply commercial doses during FY 2016 embark a good start for FY16.

Even the global sales are said to be tracking slightly ahead of expectations and in September, the company recorded the first ever monthly sale of more than 1000 doses. Given the current trading scenario and the above developments, we rate the stock as a “Hold” at the current price of $39.12

SRX Daily Chart (Source: Thomson Reuters)

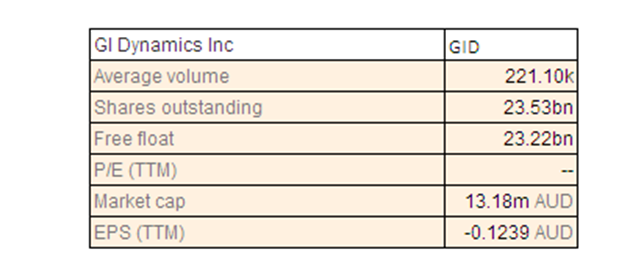

GI Dynamics Inc.

GID Details

Disappointing quarterly result: GI Dynamics Inc. (ASX: GID) stock plummeted 80.69% in the last six months (as at December 11, 2015). The company, developer of EndoBarrier, reported its quarterly results announcement for the quarter ended 30 September 2015 with revenue dropping to US$ 175,000 compared to US$ 609,000 for the same period of the previous year. While figures for the nine months ending 30 September 2015 are US$ 1.1 million as compared to US$ 2.3 million of pcp. Research and development expenses were of the order of US$ 3.9 million for the quarter compared to US$ 6.8 million for the same period last year. GID’s net loss was of the order of US$ 8.1 million for the quarter compared to US$ 12.1 million for the same period last year.

The company expects that the current cash balances will be good enough to meet the anticipated cash requirements to fund operations through December 2016. However, we believe that considering the potential for stock price growth, the stock looks to be overvalued at the current price and thus “expensive”.

GID Daily Chart (Source: Thomson Reuters)

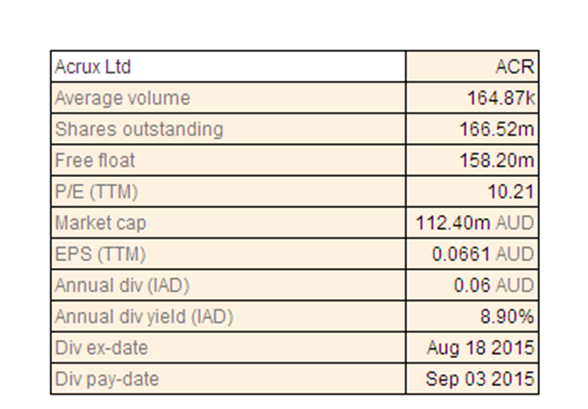

Acrux Ltd

ACR Dividend Details

Improvement in sales for Axiron: Acrux Ltd (ASX: ACR) stock plunged 48.30% this year to date while consolidating 13.22% in the last three months (as at December 14, 2015). The company recently stated that Eli Lilly reported global net sales of Axiron (based on ACR’s technology) of US$ 41.4 million in its financial results for the quarter ending 30 September 2015, which is a 28% growth compared to sales for the previous quarter to 30 June 2015. Compared to the quarter ended the 30 September 2014, sales rose by 14%. Sales for the total year to date 2015 reached to US$ 112.9 million indicating an improvement.

.jpg)

Axiron Net Sales (Source: Company Reports)

At the annual general meeting, the company announced that ACR achieved $ 11.1 million in its sixth consecutive profitable year with $ 23.1 million in cash reserves as on 30 June 2015 and Eestradiol approval in Europe triggering FY 2016 with a milestone payment of US$ 2 million. The company has identified the topical generic pipeline portfolio. Further, $ 1.02 per share has been the total capital returned to shareholders over the past five years. However, for FY 2015, revenue came to $ 25.4 million from $ 53.9 million in the previous year owing to the milestone revenue of $ 28.7 million in FY 2014 compared to nil in FY 2015. Further, EPS worked out to 6.7 cents per share, compared to 16.8 cents per share in the previous year and dividends were 6 cents per share, compared to 20 cents per share in the previous year.

We note the improvement in sales in the September quarter, but would need more conclusive evidence about the future prospects of the company. As such, we believe that the stock is “expensive” at the current price levels.

ACR Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people.Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation.Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product.The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2014 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.

AU

AU

Please wait processing your request...

Please wait processing your request...