Japara Healthcare Ltd

.png)

JHC Details

Strong operational performance: Japara Healthcare Ltd (ASX: JHC) reported for the Australian Government 2015 Aged Care Approvals Round’s (ACAR) outcome regarding allocation of 313 new residential aged care places under the 2015 process to JHC. This with 472 allocations from the previous ACAR round and 204 non-operational licences already held, JHC now holds 989 resident places under its greenfield and brownfield development program. The company also reported strong result for first half of 2016 with revenue rising by 13.4% to $155.9 million and EBITDA by 10.6% to $28.2 million. The company’s focus on high quality care and service delivery drove its performance during the period. Accordingly, Japara is also keen on making strategic investment in new capacities to leverage the rising demand from ageing population. The company is currently expanding its capacity by over 900 new beds, which is strongly supported by healthy balance sheet with net RAD inflow of $30.1 million while the net bank debt is just $1 million. Moreover, age-care industry is also supported by government with confirmed commitment to sustainable aged care funding in 2016-17.

The company recently acquired Profke with four facilities and 587 places in QLD and NSW for $77million. For second half of FY16, the management expects strong performance to continue while Profke would contribute over $ 4 million to EBITDA for FY16. Based on the foregoing, we issue a “Buy” rating on this dividend yield stock at the current market price of $2.74

JHC Daily Chart (Source: Thomson Reuters)

Aveo Group

.png)

AOG Details

Strengthening leadership position via acquisitions: Aveo Group (ASX: AOG) operates in the Australian retirement community through 95 retirement communities and is running about 17,000 homes. The Group is focusing on expanding further capacity and have confirmed its commitment to acquire Freedom Aged Care, which has 15 aged care communities with 1004 units and pipeline of 533. The group is likely to offer $215.5 million to be paid as shares and cash while the acquisition is expected to be EPS accretive from FY17.

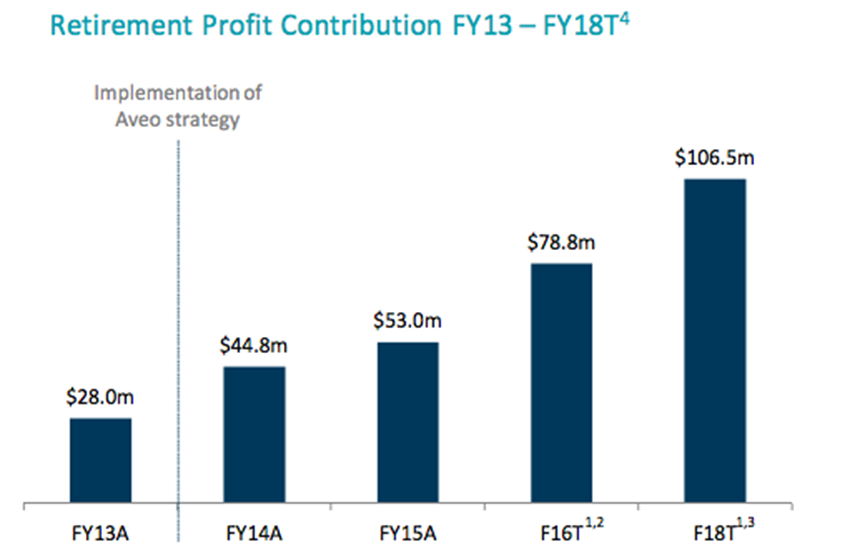

Strategy impact on retirement profits (Source: Company reports)

Meanwhile, AOG expects FY16 underlying profit after tax of over $ 80 million, return of retirement assets of 6%-6.5% and dividend of 8 cents per share. In April, the group increased its interest in Retirement Villages Group fund to 73%, wherein the portfolio consists of over 3400 units in 28 retirement villages. The acquisitions are 1.5% EPS accretive for FY17 and FY18, and accordingly the group upgraded its EPS growth guidance to 7.5% in FY17 and FY18. We recommend a “Hold” on the stock at the current market price of $3.34

AOG Daily Chart (Source: Thomson Reuters)

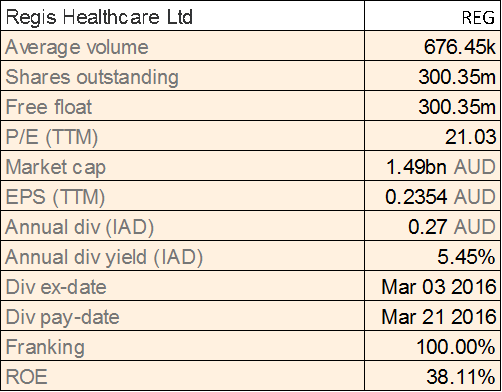

Regis Healthcare Ltd

REG Details

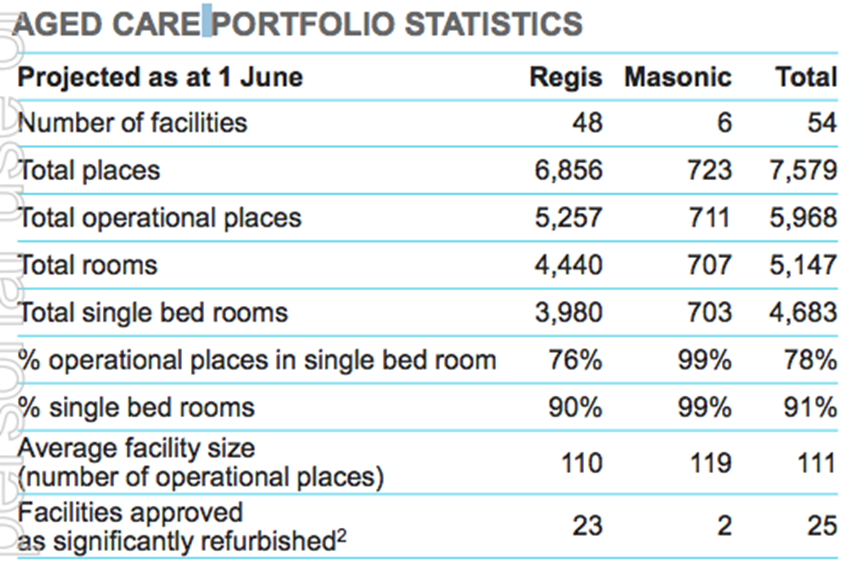

Asset acquisition:Regis Healthcare Ltd (ASX: REG) is acquiring assets from Masonic Care Queensland for an investment of $163 million. This acquisition will expand Regis capacity by 14% with 711 operational places and RAD Pool of $50.1 million. The transaction would complete by June 01, 2016 and would be EPS accretive in FY17. On the other hand, the group reported that the acquisition cost would impact its FY16 earning. Accordingly, REG stock fell over 4.83% in the last three months (as of May 27, 2016).

Aged care portfolio (Source: Company Reports)

REG expects the acquisition benefit to flow in FY17 and would impact EBITDA in the range of $10-$12 million in FY17 and net profit by circa $1-$2 million. The company plans capital expenditure of $115 -$135 million in FY17.

The company has guided FY16 EBITDA in the range of $87-$92 million while NPAT of $45 -$47 million. Following the execution of existing development pipeline, Regis will have a circa of 6,900 operational places by the end of FY19. Trading at higher P/E, we believe that the stock is “Expensive” at the current market price of $4.93

REG Daily Chart (Source: Thomson Reuters)

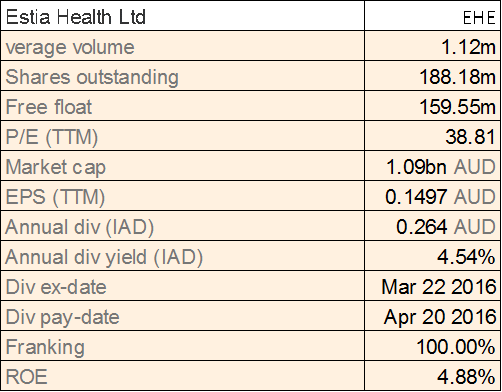

Estia Health Ltd

EHE Details

Low margin business acquisition to impact bottom line growth: Estia Health Ltd (ASX: EHE) reported a 16% rise in net profit to $ 23 million for the first six months of FY16 while revenue growth has been strong at 43% to $196 million. The growth rate of earnings is slower than its revenues on account of Estia’s strategy of acquiring relatively low-margin businesses. The company recently purchased aged care businesses of Padman, Cookcare and Kennedy. The group has funded the expansion with debt, which has adverse impact on bottom line due to rising finance costs. Additionally, the group is highly exposed to potential regulatory change. EHE has guided NPAT growth of 25% in FY16.

It has paid interim dividend of 12.8 cents per share, noting a rise of 16% compared to previous corresponding period. The stock has generated negative returns of 24.61% in last six months (as of May 27, 2016) and is still trading at unreasonable P/E. We believe that the stock is overvalued at the current market price of $5.82

EHE Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...