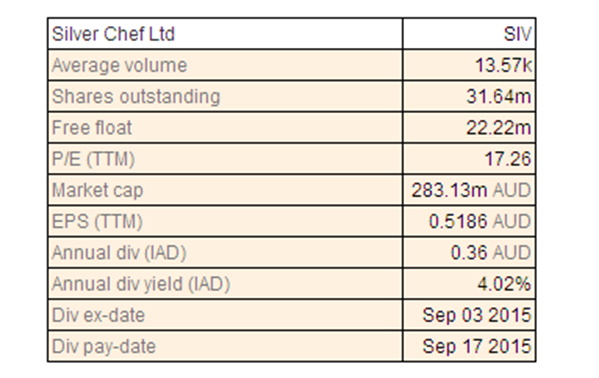

Silver Chef Ltd

SIV Dividend Details

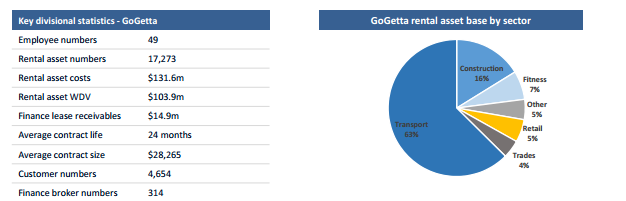

Recent Momentum in GoGetta: Silver Chef Limited (ASX: SIV), the commercial equipment leasing company, has a market capitalisation of around $ 280 million with debt of $ 166 million and cash and term deposits of $ 2.7 million as of 16 October 2015. The enterprise value is $ 443.3 million. The company value proposition for the customer is low weekly rental payments, the freeing up of working capital, the ability of trying before buying, upgrade at any time, minimum of 12 months agreement, the availability of a 75% net rental rebate on exercise of the option to purchase and simple application process without any obligation.

GoGetta Statistics (Source: Company Reports)

For FY 2015, the company reported a 22% growth in profit to $ 15.5 million on revenues which grew by 21% to $ 171 million. Both the numbers were ahead of the consensus estimates of the market. Moreover, the management decision to pay a final dividend of 20 cents per share taking the total for the year to 36 cents per share would have been welcomed by all investors. The core hospitality equipment business continued to perform well while the troubled GoGetta division seems to have turned around with revenues growing by 31%. SIV also reported that it has met its asset acquisition targets over 1Q16 and the guidance of underlying FY16 NPAT of $18.5-19.5 million, before accounting for a one-off $0.98 million after-tax item seems to be in line. In our opinion, the growth and performance have been impressive but at the same time the cyclic characteristic of the growth drivers for GoGetta (light commercial & construction) and exposure to fitness need to be thought about. We consider the stock to be overvalued at the current levels.

SIV Daily Chart (Source: Thomson Reuters)

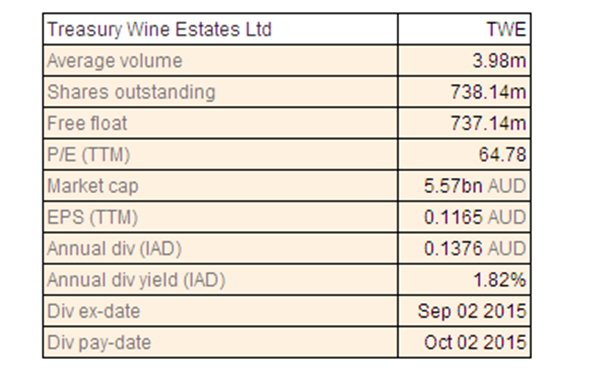

Treasury Wine Estates Ltd

TWE Dividend Details

Guidance Recapped: Treasury Wine Estates Limited (ASX: TWE) reconfirmed itsFY16 EBITS to be $270-290m excluding the impact of Diageo. The company has been able to achieve 20% rise in 1Q16 sales for the priority brands collectively. TWE is following the strategy of transforming itself into a brand and marketing led organisation. This consists of six core initiatives namely fixing the core business, realigning the portfolio, investing in brands and people, enhancing relationships with key stakeholders, optimising the capital base and driving improved financial performance. FY 2015 was therefore a reset year for the company to develop strategic, operational and cultural change. During the year, the Penfolds release date was transitioned, the supply chain optimisation initiatives were started initially identifying $ 50 million in cost savings by 2020, acceleration of the separate focus on Commercial globally, delivering on the overhead reduction program by successfully removing $ 40 million in costs from the business and identifying a further $ 15 million in savings to be achieved in FY 2016. The company also used some of the cost savings to make a change in consumer marketing investment to focus on the 15 top priority brands while optimising routes to market in China, Singapore and Korea. On a reported currency basis, net sales revenues grew by 8% and EBITDS by an impressive 22% to $ 225.1 million. The focused approach to brand building saw net sales growth in 11 of the 15 priority brands compared to 6 in the previous year. The cash flow results for a new indication of the new priorities with cash conversion above 100%. The reason behind departure of the CFO, Tony Reeves, is not very clear. At the same time, we note that TWE’s target for a ‘high teens’ EBITS margin by FY20 may be achievable at the back of savings from supply chain optimisation and other efforts. However, despite these welcomed changes in strategy and focus, we believe that the stock continues to be expensive at the current price.

TWE Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people.Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation.Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product.The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2014 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.

AU

AU

Please wait processing your request...

Please wait processing your request...