A2 Milk Company

.png)

A2M Details

Focus on high margin and differentiated business: A2 Milk company (ASX: A2M) is focused on building a high margin and differentiated business supported by its integrated IP portfolio. The Group’s outstanding success of a2 platinum infant formula (China and Australia) provides long-term growth potential and is significant contributor to earnings. Furthermore, its strategic investment in USA and UK provides exciting platform for future growth. Recent China’s favorable regulations would also support the stock in the coming months.

.png)

Operating result by segment (Source: Company Reports)

Continuing the growth momentum of first half of FY16, the management expects to end FY16 with sales revenues of NZ$ 335 million – 350 million (FY15: NZ$155.1 million) and EBITDA of NZ$ 45 million – 49 million (FY15: NZ$3.1 million). A2M was also added in S&P/ASX 300 as per the S&P Dow Jones Indices’ March quarter review. Accordingly, over a period of six months, the stock has rallied 131.69% (as on May 06, 2016) while we give a “Hold” on the stock at the current price of $1.64

.PNG)

A2M Daily Chart (Source: Thomson Reuters)

Metcash Limited

.png)

MTS Details

Steady sales:Metcash Limited (ASX: MTS) sales have been growing at a positive rate over the past five years with enhancement to its liquidity with plenty of interest coverage at 7.4x in H1FY16. The Group’s gearing ratio is at 25.4% in H1FY16. Additionally, Metcash had been in news that group was planning to acquire WOW’s Home hardware business.

Market sees merit in a Metcash acquisition of WOW’s Home Timber & Hardware chain in view of the synergies with MTS’s Mitre 10 business but the same is subject to a decision from Australia’s antitrust regulator. Management also indicated for steady financial performance in FY16. We give a “Hold” on this stock at the current market price of $1.81

.PNG)

MTS Daily Chart (Source: Thomson Reuters)

Woolworths Ltd

.png)

WOW Details

Restructuring efforts to deliver growth:Woolworths Ltd (ASX:WOW) has taken various initiatives like repositioning the Woolworths brand with the launch of “low price always” and relaunch of Woolworths reward program in supermarket segment. In petroleum segment, it widened the network by opening five new petrol sites taking the number to 521 and has plans to add another 10 new sites in H2FY16. Its liquor group is doing well along with good progress reported from the newly acquired Summergate/Pudao business in China. It further plans to grow network by seven stores in second half of FY16 with 4 new stores in New Zealand supermarket. We believe the Group would benefit from this restructure strategy and be able to deliver planned $500 million cost-savings by end of FY16.

.png)

Q3 Sales (Source: Company Reports)

WOW’s Q3 sales report indicated 0.4% rise in food and liquor sales hitting $10.7 billion on the previous year while petrol sales declined 8.7%. Standard and Poor’s has also downgraded its rating on WOW from BBB+ (outlook negative) to BBB (outlook stable).

However, WOW remains committed to a solid investment grade rating and the stock has surged 1.46% on May 09, 2016 with the announcement of a new director. We maintain our “Buy” recommendation on WOW at the current market price of $21.52

.PNG)

WOW Daily Chart (Source: Thomson Reuters)

Treasury Wine Estates Ltd

.png)

TWE Details

Strong result combined with strategic initiatives are paying off: Treasury Wine Estates Ltd (ASX: TWE) reported impressive 42% jump in net profit on 22% rise in net sales for the first half of FY16. Its branded portfolio delivered 15% growth while its supply chain initiatives delivered $1.13 per case COGS benefits during the period. The company has also declared interim dividend of 8 cents. The acquisition of Diageo Wine is in integration process and would add to group’s priority brands. The group is extending the market reach by launching priority brands in Australia, New Zealand, Asia, and Europe markets.

.png)

Treasury Wine Estate performance (Source: Company Reports)

The management has guided FY16 EBITS (pre – Diageo Wine acquisition) to be towards upper end of $270 million - $290 million. Accordingly, TWE had already rallied over 37.09% (as of May 06, 2016) in the last six months placing the stock at high P/E and at a low dividend yield. We believe the stock is “Expensive” at the current market price of $10.23

.PNG)

TWE Daily Chart (Source: Thomson Reuters)

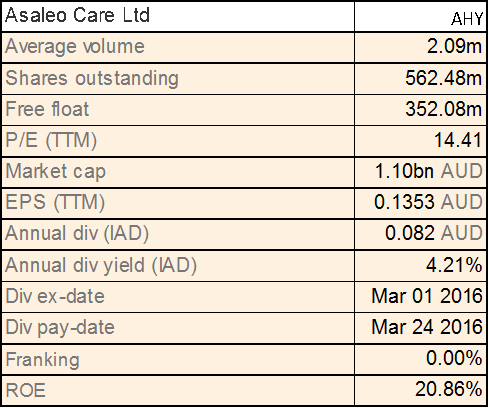

Asaleo Care Ltd

AHY Details

Dollar movement and commodity prices weigh on performance: Asaleo Care Ltd (ASX: AHY) reported EBITDA growth of 3.1% to $145.2 million while underlying net profit grew 5.3% to $76.1 million for FY15. The Group declared dividend of 10 cents for the year. Meanwhile, AHY has taken various steps to improve its performance through product innovation, extending the range of products, improving distribution and cost reduction. Despite that, the management is cautious for FY16 performance and guided steady underlying EBITDA and net profit along with low to mid-single digit EPS.

On the other hand, the strengthening Australian dollar coupled with recovering commodity prices drove the stock by 16.07% in the last three months (as of May 06, 2016). We give a “Hold” recommendation on the stock at the current market price of $2.02

.PNG)

AHY Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2016 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.

AU

AU

Please wait processing your request...

Please wait processing your request...