Scentre Group

SCG Dividend Details

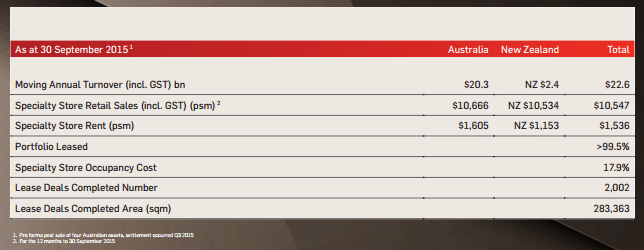

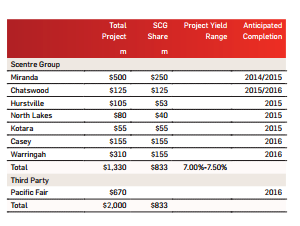

Strong growth in specialty sales: Scentre Group (ASX: SCG) recently announced its third quarter results with highlights as continued strong portfolio performance, commencement of $830 million of development starting in 2015 (new projects including North Lakes and Kotara), and introduction of several new technology initiatives and reallocated capital to higher quality assets. As at 30 September 2015, the portfolio remained more than 99.5% leased, and had specialty sales growth of 5.9% for the nine months and 5.4% for the quarter. In particular, the Footwear, Leisure, jewellery and Technology and Appliances retail categories have performed well over the period.

Operating Performance (Source: Company Reports)

The strong growth in specialty sales for the period outpaced the growth in specialty store rents, and reduced specialty store occupancy cost to 17.9%. In Australia, average specialty retail sales increased to $10,666 per square metre and comparable specialty store sales growth was 5.8% for the nine months to 30 September 2015. In New Zealand, average specialty retail sales increased to NZ$10,534 per square metre, and comparable specialty store sales growth was 6.5% for the nine months. Earlier, the Group reported AIFRS profit of $1.3 billion for the 6 months ended 31 December 2014. This profit included FFO earnings of $577.9 million (or 10.88 cents per security, on an annualised basis, in line with pro forma forecast), $648.9 million of property revaluations, $(15.8) million of tenant allowances amortisation, $96.7 million relating to the mark to market of derivatives and property-linked notes, $(18.9) million charge for deferred tax and $(6.0) million of FFO from external non-controlling interests. SCG now has FFO forecast of 22.5 cents per security indicating 3.5% growth in distribution forecast for the twelve months ending 31 December 2015.

Project Details (Source: Company Reports)

SCG is currently trading at a stock price of about $3.91. The company is currently trading at a Price to earnings ratio of 8.84x and a dividend yield of 5.25%. The 52-week high stock price of the company is 4.205 and 52 week low of 3.380. Looking at the prospects, we put a Hold recommendation for the stock at the current price of $3.91

SCG Daily Chart (Source: Thomson Reuters)

Medibank Private Ltd

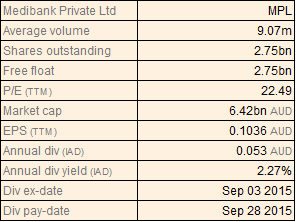

MPL Dividend Details

Sustainable Performance: Medibank Private Limited (ASX: MPL), in the past one year, has seen new members appointed to the Board, which as per the company has provided a mix of backgrounds and experience to strengthen the Board’s capacity to prepare the Company for the listing and future growth. MPL reported that its Net profit after tax (NPAT) surged by $154.5 million to $285.3 million in 2015 reflecting that $134.7 million before tax of expenses were incurred in the prior year for the write-down of goodwill, mainly associated with the Telehealth business, and for the reorganisation of Complementary Services. NPAT increased by $33.5 million or 13.3% from $251.8 million to $285.3 million on excluding the above amounts. This was principally due to the 32.5% improvement in operating profit in the Health Insurance business. This more than offset the reductions in the contribution from the Complementary Services business and net investment income.

Health Insurance business delivered strong growth during the year with operating profit increasing 32.5% to $332.2 million. While the company’s Health Insurance revenue was up 5.1%, it saw increased consumer focus on affordability contributing to cover reduction and lapse activity. The gross margin rose indicating improvements from the company’s health benefit claims management program. The company’s management expense ratio dropped down from 9.1% last year to 8.6%.

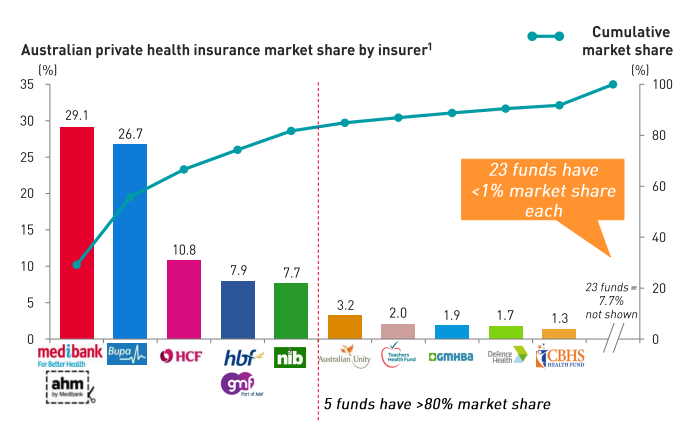

Industry Dynamics (Source: Company Reports)

As reported, the Health Insurance business operates a single health fund through two brands which are managed on an overall portfolio basis with an emphasis on Group outcomes. In 2015, 98% of Health Insurance revenue originated from resident health insurance policies sold to the retail and corporate customer segments, with the balance from overseas visitors and students health cover policies. Premium revenue surged by 5.1%. This increase was owing to government approved premium rate rises of 6.50% (effective from 1 April 2014) and 6.59% (effective from 1 April 2015). Average revenue per member increased by 4.4% reflecting sales mix changes due to greater growth in extras cover and cover reductions. The company reported that Medibank brand volumes were down marginally, but at the same time, the ahm brand continued its strong member growth and continued to grow its share of the new-to-industry segment of the market. MPL’s project DelPHI that represents the $150m investment to replace the company’s core systems is in the testing stage. The same will bring lot many changes with its roll out due over the next year.

We look forward to the management guidance for premium revenue growth above 5.5% in FY 2016 and drop in the management expense ratio to below 8% in FY17. Further, operating profit target for Health insurance is said to be above $370 million in FY 2016. MPL is currently trading at a reasonable price to earnings ratio of ~22x compared to its peers. Based on the foregoing, we put a BUY on MPL at the current price of $2.30.

MPL Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people.Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation.Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product.The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2014 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.

AU

AU

Please wait processing your request...

Please wait processing your request...