.png)

Stocks’ Details

WiseTech Global Limited

WTC Cleared Wrong Claims Report by J Capital Research Limited:WiseTech Global Limited (ASX: WTC) is a leading developer and provider of software solutions to the logistics execution industry globally. Recently, the company rejected claims of financial impropriety and irregularity released in a second short-seller report by J Capital Research Limited.WTC, in order to avoid any manipulation in the company’s share price, requested for trading halt for its securities. The company confirmed its FY20 guidance of revenue to come in between $440 Mn - $460 Mn with a growth range of 26% - 32%. FY20 EBITDA guidance has been estimated in the range of $145 Mn - $153 Mn with EBITDA growth range of 34% - 42%.

FY19 Key Highlights for the period ended June 30, 2019:Total revenue increased by 57% to $348.3 Mn, mainly due to the increased transaction and user growth within the existing customer base; new customers won in the year and strategic acquisitions completed in FY19. Net profit attributable to equity holders increased by 33% to $54.1 Mn. The Board of Directors declared a fully franked final dividend of 1.95 cps, with record date and payment date on September 9, 2019 and October 4, 2019, respectively.

.png)

FY19 Income Statement (Source: Company Reports)

Stock Recommendation:WTC’s share generated a positive YTD return of 58.31%. Its EBITDA margin and net margin for FY19 stood at 31.0% and 15.5%, better than the industry median of 25.7% and 15.1%, respectively. Its current ratio for FY19 stood at 1.92x, better than the industry median of 1.75x. However, the stock has corrected by 29.34% from its 52-week high level of 38.800 (September 6, 2019). We would like to see the further implications of such clarifications with respect to FY20 guidance and how things pan out from hereon. Hence, we have a wait and watch view on the stock at the current market price of $27.500, up 2.003% on November 8, 2019.

Appen Limited

Decent H1FY19 Top-Line and Bottom-Line Performance:Appen Limited (ASX: APX) is involved in the provision of quality data solutions and services for machine learning and artificial intelligence applications for global technology companies, auto manufacturers and government agencies. Recently, the company issued 7,033 new shares as a result of vesting performance rights.

H1FY19 Key Highlights for the period ended June 30, 2019:Revenue for the period increased by 60% to $245.1 Mn. Underlying EBITDA increased by 81% to $46.3 Mn and statutory EBITDA increased by 48%. Underlying EBITDA margins improved from 16.8% to 18.9%. Underlying NPAT increased by 67% to $29.6 Mn and statutory NPAT increased by 33% to $18.6 Mn. The Board has declared an interim dividend of 4.0 cents per share, partially franked, in-line with the same period last year.

.png)

H1FY19 Key Financial Metrics (Source: Company Reports)

What to expect:The Company’s ongoing investment in technology positions it to meet the market’s demand for high volumes of quality data at speed across multiple data types for a growing number of use cases.

Stock Recommendation:APX’s share generated a positive YTD return of 56.17%. Its gross margin and EBITDA margin for H1FY19 stood at 40.8% and 16.6%, better than the H1FY18 result of 36.2% and 16.2%, respectively, implying improving financials for the company. Its debt to equity ratio for H1FY19 stood at 0.07x, lower than the industry median of 0.53x. Its EV/Sales multiple on TTM basis stands at 4.7x, slightly lower than the industry median of 4.9x. Hence, considering the company’s decent top-line and bottom-line performance, improving profitability margins, and current trading levels, we recommend a “Buy” rating on the stock at the current market price of $20.70, up 3.552% on November 8, 2019.

Afterpay Touch Group Limited

APT Responds Over Possible Regulatory Developments by RBA:Afterpay Touch Group Limited (ASX: APT) is involved in providing technology-driven payment solutions for customers and businesses through its Afterpay and Pay Now services and businesses. Recently, the company announced the issuance of 10,000 shares at a value of $7.68 per share, which will be issued upon exercise of 10,000 options issued to senior executives of the company under the company’s plan.In another update, media reports highlighted the possible regulatory developments following the Reserve Bank of Australia’s (RBA) 2020 review of payments regulation, including “surcharging” practices in Australia. Over this report, APT responded by stating that it is currently not subject to an RBA inquiry or review process, however, it welcomes the opportunity to engage with the RBA as part of its broad based, periodic review of the payments industry next year.

FY19 Key Highlights for the period ended June 30, 2019:Global underlying sales increased by 140% to $5.2 Bn. Active customer’s numbers at the end of FY19 increased by 130% to 4.6 Mn. Active merchants at the end of FY19 increased by 101% to 32,300. Statutory loss before tax for the period came in at $43.8 Mn, mainly impacted by one-off and non-cash items (including share-based payment expenses and the initial application of new accounting standards).

.png)

FY19 Key Metrics (Source: Company Reports)

What to expect:As per the release, the company is executing its mid-term strategy and capturing the significant addressable global market opportunity in its current markets in order to meet its FY22 target of $20 Bn++ of Gross Merchandise Value (GMV) and Net Transaction Margin (NTM) of ~2%.

Stock Recommendation:APT’s share generated a positive YTD return of 118.67%. Its gross margin for FY19 stood at 77.4%, better than the industry median of 76.2%. Its current ratio for FY19 stood at 5.78x, better than the industry median of 2.81x. However, its EBITDA margin and net margin declined in FY19 as compared to FY18. The stock declined ~28.25% from its recent made fresh 52-week high level of $37.410 (October 15, 2019). Hence, considering the company’s mixed financial performance, current trading levels, and the recent media and analyst report commenting on possible regulatory developments following the Reserve Bank of Australia 2020 review of payment regulation and its impact, in case, such developments take place in favour of APT, we put our wait and watch stance on the stock at the current market price of $26.970, up 2.782% on November 8, 2019.

Altium Limited

Overvalued Position at the Current Juncture:Altium Limited (ASX: ALU) is involved in the development and sales of computer software for the design of electronic products. Recently, the company’s director Samuel Weiss acquired 1,000 shares at USD $23,340 (including brokerage), taking the final holdings to 1,901,207 shares, effective from October 15, 2019.

FY19 Key Highlights for the period ended June 30, 2019:Revenue growth across all business units and all key regions increased by 23% to US$171.8 Mn in FY19. Net profit after tax for the period was reported at US$52.9 Mn. The period witnessed a record growth in new Altium Designer seats and subscription base to more than 43,600 subscribers at 27% and 13%, respectively. The Board of Directors declared an unfranked final dividend of AUD 18 cents per share, with record date and payment date on September 4, 2019 and September 25, 2019, respectively.

.png)

FY19 Key Metrics (Source: Company Reports)

What to Expect:The company aims to become a leader in the PCB design software market and achieve US$200 Mn in revenue by 2020. It is determined to achieve market dominance by 2025 and to enroll 100,000 subscribers by then.

Stock Recommendation:ALU’s share generated a positive YTD return of 49.88%. Its gross margin and net margin for FY19 stood at 36.9% and 30.6%, better than the industry median of 25.7% and 15.1%, respectively, which implies decent fundamentals of the company. Its ROE for FY19 stood at 31.4%, better than the industry median of 12.6%. However, on valuation front, EV/Sales multiple on TTM basis stands at 15.1x, higher than the industry median of 4.9x, indicating an overvalued position at the current juncture. Currently, the stock is trading towards its 52-week levels of $38.49 with PE multiple of 55.99x. Hence, considering the aforesaid facts and current trading levels, we recommend an “Expensive” rating on the stock at the current market price of $32.530, up 0.432% on November 8, 2019.

Xero Limited

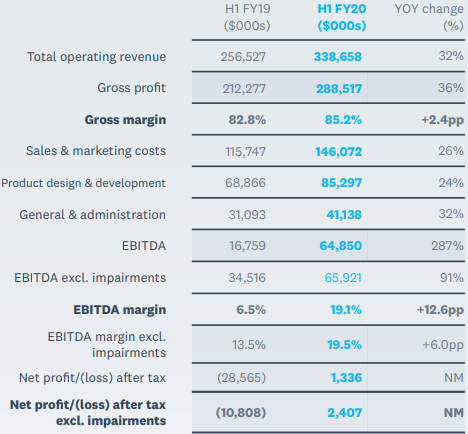

XRO Reported First Time Interim Net Profit of $1.3 Mn:Xero Limited (ASX: XRO) is involved in the provision of an online business platform to small businesses and their advisors.

H1FY20 Key Highlights for the period ended September 30, 2019:Operating revenue growth for the period increased by 32% on y-o-y basis and 33% on constant currency basis, primarily driven by subscriber growth across all the markets. EBITDA for the period improved to $48.1 Mn on y-o-y basis. Company reported first-time interim net profit of $1.3 Mn as compared to loss of $28.57 Mn in the previous corresponding period.

H1FY19 Income Statement (Source: Company Reports)

What to expect:Company’s free cash flow in FY20 is expected to be a similar proportion of total operating revenue to that reported in the FY19.

Stock Recommendation:XRO’s share generated a positive YTD return of 76.28%. Its gross margin, EBITDA margin and net margin for H1FY20 stood at 85.2%, 19.5% and 0.4%, respectively, better than H1F19 results, however, lower than the industry median. Its current ratio for H1FY20 stood at 5.50x, better than the industry median of 1.72x. As on 08 November 2019, the stock made a new 52-week high and closed at $75.710. Hence, considering aforesaid facts along with current trading levels, we recommend an “Expensive” rating on the stock at the current market price of $75.710, up 2.38% on November 8, 2019.

.jpg)

Comparative Price Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...