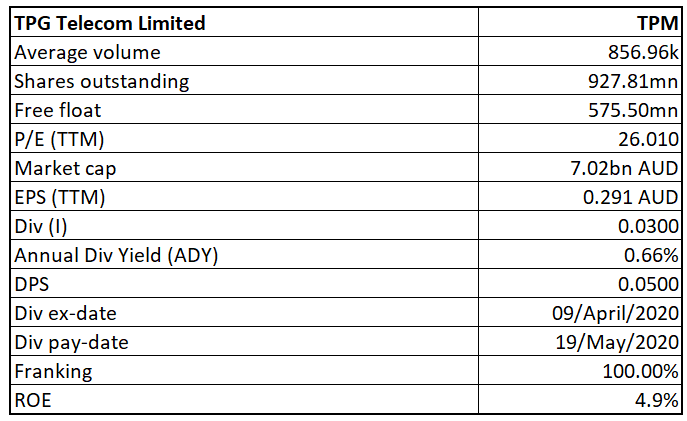

TPG Telecom Limited

TPM Details

Scheme Booklet for Merger Released: TPG Telecom Limited (ASX: TPM) is engaged in the provision of consumer, wholesale and corporate telecommunications services. The company recently provided a key update regarding the proposed merger with Vodafone Hutchison Australia Pty Limited, stating that the Scheme Booklet in relation to the proposed merger has been registered with the Australian Securities and Investments Commission. The Scheme is to be evaluated by TPG shareholders, who will then vote on the same in a meeting to be conducted on 24th June 2020. Therefore, the formation of Australia’s leading full-service telecommunications provider, is now dependent on TPG shareholder approval along with final court approval.

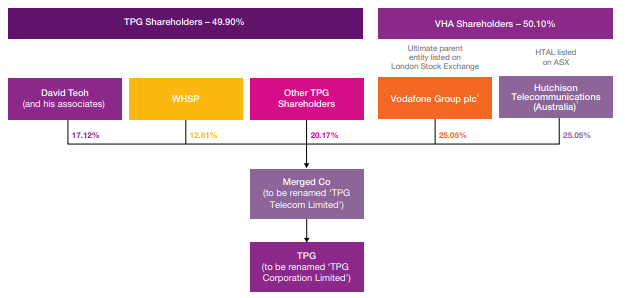

Ownership Details Post Merger:VHA is the third largest mobile telecommunications provider in Australia and operates its own 3G and 4G mobile network through its mobile sites located nationally across Australia and has commenced the rollout of a 5G mobile network. Under the scheme, 100% of TPG shares will be acquired by VHA and will be listed on ASX in the name of “TPG Telecom Limited” under the code “TPG”, with VHA shareholders owning 50.1% shares in the new group and TPG shareholders owning the remaining 49.9%. Moreover, the shareholders are also asked to pass a special resolution for the change in name of TPG Telecom Limited to TPG Corporation Limited in the same meeting.

Overview of the Merger (Source: Company Reports)

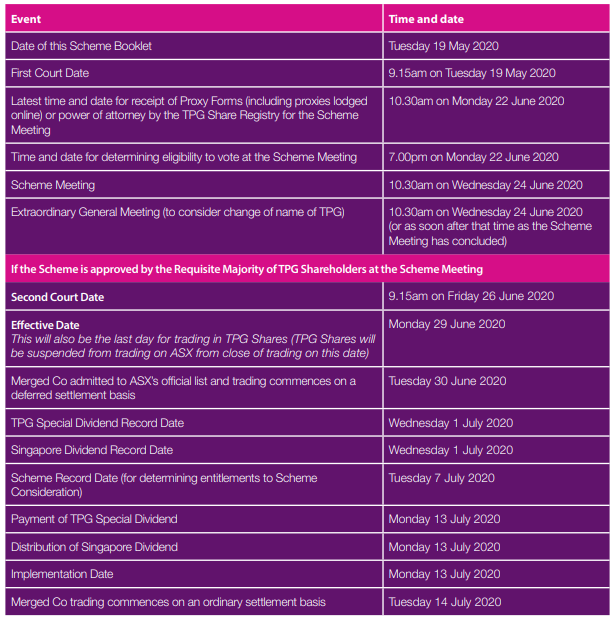

Key Events Dependent on the Scheme Becoming Effective:If approved, TPG shareholders will receive one share in the merged company for each TPG Share under the scheme. Prior to the implementation of the scheme and subject to the scheme becoming effective, TPG Board intends to pay the TPG Special Dividend as a fully franked cash special dividend to the shareholders who hold shares on the TPG Special Dividend Record Date. Also, the company will undertake a separation of its Singapore business to existing TPG shareholders through in-specie dividend distribution of one Singapore Co Share for every two TPG Shares owned as at the Singapore Dividend Record Date.

Key Dates (Source: Company Reports)

Arguments in Favour of the Scheme:

1. As per the Director of TPG, the Scheme involves a combination of two highly complementary businesses, which will join to form an enhanced network with more diverse earnings.

2. The merger group will have a comprehensive telecommunications product offering and is expected to have a broad range of customers along with mass sales channels and a strong combined distributions strategy.

3. The merger will also lead to significant synergies in infrastructure, network and transmission savings, consolidation of overlapping functions of the two businesses and economies of scale, which can be utilised to capitalise on future growth opportunities.

4. Last but not the least, the combined entity will have enhanced financial flexibility from a strong balance sheet position.

5. The entity is expected to have total annual pro forma historical revenue and EBITDA of approximately $5,909 million and $1,977 million, respectively, anticipated drawn debt at Implementation of approximately $4,771 million, anticipated net debt to pro forma historical EBITDA ratio of 2.6x times.

Key Risks:The Scheme, however, did not conceal any risks associated with the approval, and listed a few cases when an investor may not be willing to vote in favour. First and foremost, an investor may wish to confine the investment and exposure to a business with TPG’s specific characteristics and may be reluctant to a change in the investment profile. There may be a risk of complications related to the merger, which may require more time and costs to reach a meaningful level of synergies. Another risk can be an event of different or adverse tax consequences for certain TPG Shareholders. In addition, a possibility of a Superior Proposal also poses a threat to the current proposed deal with VHA.

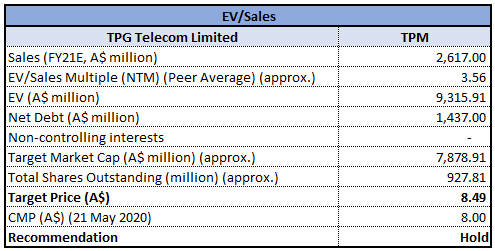

Valuation Methodology:EV/Sales Multiple Based Relative Valuation (Illustrative)

EV/Sales Multiple Based Relative Valuation (Source: Refinitiv, Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

Stock Recommendation: The stock of the company gave positive returns of 16.10% in the past 6 months and is currently inclined towards its 52-week high of $8.780.TPG Directors unanimously recommended to vote in favour of the scheme in the absence of a Superior Proposal, stating that the scheme is likely to enhance TPG shareholder value in the long run. The Scheme was also assessed by an Independent Expert, who again believed that it is in the best interest of TPG shareholders. The merger group has significant synergy potential, with increased financial scale and a strengthened balance sheet supported by strong free cash flow generation. Following the implementation of the scheme, the merged company is intended to pay a dividend to at least 50% of NPAT. We have valued the stock using EV/Sales multiple based illustrative relative valuation method and arrived at a target price with higher single-digit upside in percentage terms. For the purpose, we have considered peers like Vocus Group Ltd (ASX: VOC), Nine Entertainment Co Holdings Ltd (ASX: NEC) and REA Group Ltd (ASX: REA). Considering the above factors, we give a “Hold” recommendation on the stock at the current market price of $8.0, up 5.68% on 21st May 2020.

.jpg)

TPM Daily Technical Chart (Source: Refinitiv, Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

AU

AU

Please wait processing your request...

Please wait processing your request...