.png)

Stocks’ Details

Woolworths Group Limited

Court Approval for Restructure Scheme: Woolworths Group Limited (ASX: WOW) is engaged in food, general merchandise and specialty retailing through chain store operations. As on 22 January 2020, the market capitalization of the company stood at $50.46 billion. The company has recently announced that it has received approval from the Federal Court for the Restructure Scheme to combine Woolworths Group’s drinks and hospitality businesses to create Endeavour Group. WOW intends to implement the Restructure Scheme on 2 February 2020.

During FY19, NPAT attributable to Woolworths Group shareholders went up by 9.2% and stood at $1,752 million. As a consequence of which EPS increased by 8.8% to 134.2 cents per share. The decent financial performance enabled the Board to pay dividends of 57 cents, up by 14% on the previous year.

.png)

FY19 Financial Performance (Source: Company Reports)

Growth Opportunities: Despite an uncertain consumer environment and input cost pressures, the company is energised by the material opportunities to unlock further value for customers and shareholders in F20. It expects to add 15-30 Metro stores in FY20 and will work on creating differentiation in all of its businesses. WOW expects that Endeavour Drinks will continue to evolve and will improve the digital experience, which will deliver more localised ranging and improve services and convenience.

Valuation Methodology: EV/Sales Multiple Approach

.png)

EV/Sales Multiple Approach (Source: Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: As per ASX, the stock of WOW gave a return of 6.75% in the last 3 months and a return of 6.52% in the past one month. The stock made its new 52-week high of $41.320 on 22 January 2020 and managed to close at this level. During FY19, net margin of the company stood at 2.6%, slightly higher than the industry median of 2%. In the same time span, ROE of the company was 14.4% as compared to the industry median of 13.3%. Considering the returns, trading levels, higher ROE and decent outlook, we valued the stock using the EV/Sales valuation approach and arrived at a target upside of higher single-digit (in percentage terms). For the said purposes, we have considered Coles Group Ltd (ASX: COL), JB Hi-Fi Ltd (ASX: JBH) and Harvey Norman Holdings Ltd (ASX: HVN) as peers. Hence, we recommend a “Hold” rating on the stock at the current market price of $41.320, up by 3.274% on 22 January 2020.

Sonic Healthcare Limited

Record Net Profit: Sonic Healthcare Limited (ASX: SHL) is a medical diagnostics company that provides laboratory and radiology services to medical practitioners, hospitals, community health services, and their collective patients. During FY19, the company reported an increase in revenue by 12% to $6.2 billion and a rise of 16% in net profit of $550 million. SHL continued its progressive dividend policy and paid a total of 84 cents in dividend in FY19.

.png)

Annual Revenue (Source: Company Reports)

Future Expectations: The company is well positioned for ongoing strong growth and expects EBITDA to grow by 6-8% on underlying FY19 EBITDA of $1,052 million. It also anticipates a decrease in interest expense by 5% and expects lower capital expenditure in FY20. SHL anticipates a global team of over 1,000 pathologists, more than 200 radiologists and thousands of qualified technical staff in the company’s Medical Leadership culture.

Valuation Methodology: EV/EBITDA Multiple Approach

.png)

EV/EBITDA Multiple Approach (Source: Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: As per ASX, the stock gave a return of 5.75% in the past one month and made a new 52-week high of $31.560 on 22 January 2020. During FY19, the gross margin of the company stood at 83.8%, higher than the industry median of 37.2%. In the same time span, ROE was in-line with the industry median and stood at 11.5%. Considering the returns, trading levels, higher gross margin and future expectations, we have valued the stock using an EV/EBITDA valuation approach and arrived at a downside of higher single-digit (in percentage terms). For the said purposes, we have considered Ramsay Health Care Ltd (ASX: RHC), Healius Ltd (ASX: HLS), Resmed Inc (ASX: RMD), etc., as peers. Hence, we recommend an “Expensive” rating on the stock at the current market price of $31.440, up by 1.191% on 22 January 2020.

Fortescue Metals Group Ltd

Strong Start to FY20: Fortescue Metals Group Ltd (ASX: FMG) is engaged in mining, processing and transporting of iron ore for export from the Company's deposits within the Pilbara region of Western Australia. The company has recently released its September 2019 quarterly production results, wherein it reported shipments of 42.2 million tonnes and average revenue of US$85 per dry metric tonne. The operational performance and realised price have generated exceptional operating cashflows and lowered net debt to US$0.5 billion at 30 September 2019.

.png)

Production Summary (Source: Company Reports)

What to Expect: The company gave guidance for its shipments and expect it to be in the range of 170-175 mt with a total capital expenditure of US$2.4 billion. It also expects its C1 costs to be between US$13.25 - 13.75/wmt. The company also anticipates its pay-out ratio between 50% to 80% of full-year net profit after tax.

Valuation Methodology: Price/Earnings Multiple Approach

.png)

Price/Earnings Multiple Approach (Source: Thomson Reuters), 1USD=1.46 AUD

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: As per ASX, the stock of FMG gave a return of 12.06% on the YTD basis and a return of 11.65% in the past one month. The stock is trading close to its 52-weeks’ high level of $12.810. During FY19, net margin of the company stood at 32%, higher than the industry median of 11% and ROE of the company was 31.4% as compared to the industry median of 12.3%. This indicates that the company is well deploying the capital of its shareholders and is able to generate profits internally. Considering the returns, trading levels, higher net margin and ROE and decent outlook, we valued the stock using Price/Earnings based valuation approach and arrived at a target upside of higher single-digit (in percentage terms). Hence, we recommend a “Hold” rating on the stock at the current market price of $12.690, up by 5.05% on 22 January 2020.

Nextdc Limited

Strong Growth in Customers and Connectivity: Nextdc Limited (ASX: NXT) is engaged in the development and operation of independent data centres in Australia. During FY19, revenue of the company went up by 15% to $179.3 million and underlying EBITDA witnessed an increase of 13% to $85.1 million. The company also witnessed a CAGR of 31% in customers over the span of 5 years. The strong growth in connectivity drives average interconnects per customer to 9.3 in FY19 as compared to 8.9 in FY18.

.png)

Growth in Customers and Connectivity (Source: Company Reports)

What to Expect: Solid growth in recurring data centre services revenues and a strong demand for connectivity solutions is expected to deliver revenue between $200 million to $206 million in FY20. The company also expects its underlying EBITDA to range between $100 million to $105 million, up by 17% to 23% on FY19. Continued expansion of S2 and strong growth in customer demand underpins the company’s capital expenditure expectation which is expected to be in the range of $280 million to $300 million in FY20.

Valuation Methodology: EV/EBITDA Multiple Approach

.png)

EV/EBITDA Multiple Approach (Source: Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: As per ASX, the stock gave a return of 11.04% in the past one month and made a new 52-week high of $7.540 on 22 January 2020. During FY19, EBITDA margin of the company stood at 52.4%, higher than the industry median of 26.7%. In the same time span, current ratio of the company was 7.04x as compared to the industry median of 2.51x. Considering the returns, trading levels, higher EBITDA margin and positive outlook, we have valued the stock using EV/EBITDA valuation method and arrived at a target upside of higher single-digit (in percentage terms). For the said purposes, we have considered Superloop Ltd (ASX: SLC), WiseTech Global Ltd (ASX: WTC), Xero Ltd (ASX: XF1) and Appen Ltd (ASX: APX) as peers. Hence, we recommend a “Hold” rating on the stock at the current market price of $7.480, up by 0.538% on 22 January 2020.

Ramsay Health Care Limited

Significant Rise in Revenue: Ramsay Health Care Limited (ASX: RHC) is a global hospital group that owns and operates a comprehensive range of healthcare facilities. The company has recently appointed Mr Martyn Roberts as Group Chief Financial Officer. In the recently held AGM, the Management of the company stated that revenue of the company went up by 24.4% and stood at $11.4 billion in FY19. In the same time span, Core net profit after tax increased by 2% to $590.9 million. This resulted in EPS to increase by 2.1% to 285.8 cents.

.png)

FY19 Financial Performance (Source: Company Reports)

Growth Opportunities: The company is well-positioned as a leading international healthcare service provider and it expects opportunities that will drive efficiencies and establish stronger global partnerships. In FY20, the company continues to target Core EPS growth of 2% to 4% on a like-for-like basis.

Valuation Methodology: EV/EBITDA Multiple Approach

.png)

EV/EBITDA Multiple Approach (Source: Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: As per ASX, the stock gave a return of 5.76% in the past one month and made a new 52-week high of $79.240 on 22 January 2020. During the year, gross margin of the company stood at 74.6%, higher than the industry median of $37.2%. In the same time span, ROE was 22.3% as compared to the industry median of 11.7%. Considering the returns, trading levels, higher gross margin and ROE and decent growth opportunities, we have valued the stock using EV/EBITDA multiple approach and have arrived at a target upside of higher single-digit (in percentage terms). For the said purposes, we have considered CSL Ltd (ASX: CSL), Sonic Healthcare Ltd (ASX: SHL), Healius Ltd (ASX: HLS), etc. as a peer group. Hence, we recommend a “Hold” rating on the stock at the current market price of $79.220, up by 1.577% on 22 January 2020.

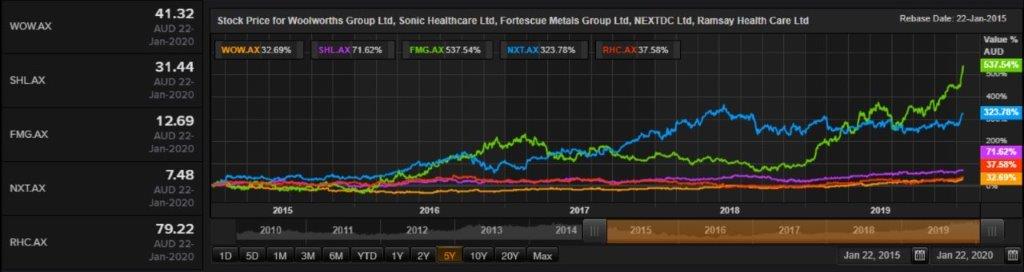

Comparative Price Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...