Robust earnings led by institutional banking division:For H1FY17, Australia's second largest lender, Westpac Banking Corporation (ASX: WBC) reported highest cash earnings, aided by a fall in bad debt coupled with sturdy growth in institutional division. The stock edged slightly higher (0.65%) on May 08, 2017 at the back of the result. Revenue from operations grew by 3% year on year (yoy) to $10.7 billion while posting 6% yoy growth in statutory net profit at $3.9 billion. However, net interest margin (NIMs) fell 7 basis points to 2.07% yoy due to increased interest rates to attract deposits, while return on equity declined by 2bps yoy to 14%. The Institutional business has reported robust growth in earnings driven by improved credit quality, customer transactions, and a strong result from markets businesses while consumer and business banking margins were affected by higher funding costs. Further, the increase in net operating income was driven by higher contribution from institutional banking division with significant customer transactions coupled with robust markets income.However, 1% growth in lending and 3% growth in deposits was mostly offset by lower net interest margins. Importantly, the decline in margins was mostly due to a lag effect of rising funding costs not being reflected in lending rates until later in the half.

.png)

Cash earnings- divisional performance (Source: Company reports)

The group has continued to witness growth in wealth and insurance, with funds on the new Panorama system increasing by over $1 billion and life in-force premiums rising 6%. General insurance gross written premiums were lower over the last six months, falling 3%, although they were 2% higher over the year. During H1FY17, given the low growth environment, evolving liquidity requirements and limits on certain types of lending, the bank focused more on enhancing returns and further strengthening the balance sheet while being targeted on loan growth. The bank is expected to raise mortgage rates across a range of products as it will increase variable home loan rate for owner occupiers by 3-8 basis points, and 23-28 basis points for property investors.

.png)

Net interest margins trend (Source: Company reports)

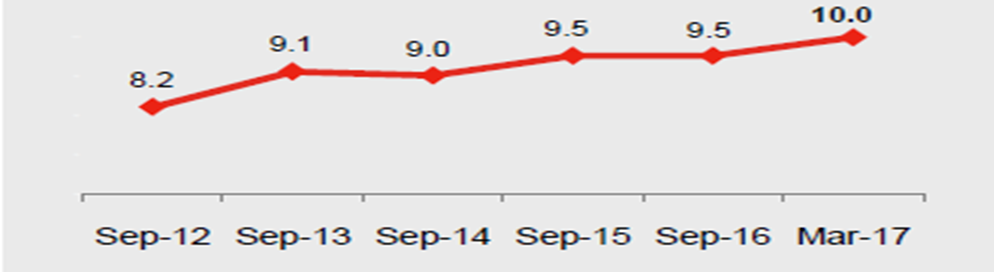

Strengthening balance sheet and liquidity position: Westpac further strengthened its balance sheet during H1FY17, with the common equity tier-1 (CET-1) capital ratio of 10.0% against 9.5% in H2FY16, which is above the group’s preferred range of 8.75% to 9.25%. Further, liquidity position has remained solid at liquidity coverage ratio (LCR) of 125%, while the new net stable funding ratio (NSFR) stood at 108%. Moreover, the group’s funding mix also strengthened with a rise in more stable funding sources (customer deposits and long term wholesale funding) and an increase in the duration of wholesale funding.

CET-1 ratios (Source: Company Reports)

Investigation against ‘Big Four’ banks: Australian government announced that it will conduct an inquiry into competition in the country's financial system, following a series of scandals in the banking sector and public allegations against the ‘Big Four’ banks of abuse of market power. Four major lenders, Commonwealth Bank of Australia, Westpac Banking Corp, Australia and New Zealand Banking Group and National Australia Bank have come under fire recently following several scams involving misleading financial advice, insurance fraud and interest-rate rigging, as well as for refusing to pass on official interest rate cuts in full. The four together control 80% of Australia's lending market and have posted record profits for years. The inquiry will consider the degree of concentration in key segments of the financial system, examine barriers to innovation in the system and consider competition in personal deposits and mortgages for households and small businesses. Notably, the productivity commission is expected to commence the inquiry on July 1, 2017, and the final report is likely to be presented to the government within 12 months.

Recommendation: The stock has moved up by 11% over the past six months as at May 05, 2017, and is trading at higher levels.We give an “Expensive” recommendation on the stock at the current price of $ 34.08

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...