Magellan Financial Group Ltd

.png)

MFG Details

Strong financials and dividend: As of March 31, 2016, Magellan Financial Group Ltd (ASX: MFG) recorded A$39.3 million in total funds under management compared to A$38.8 million in year ago period. In the month of March, MFG recorded net inflows of $1,222 million which included net retail inflows into Global equities strategies of $167 million and net institutional inflows of $1,017 million.

.png)

MFG Financials (Source: Company reports)

The company has a strong balance sheet with cash and liquid assets of $312.9 million and no debt. Interim dividend for first half financial year 2016 stood at 51.3 cents per share.

With a strong dividend yield, MFG has recorded a gain of 9.17% (As of April 22, 2016) in the last six month trading session. Based on the foregoing, we believe that the stock has further room for growth and thus we recommend a "BUY" rating at the current share price of $22.62

.PNG)

MFG Daily Chart (Source: Thomson Reuters)

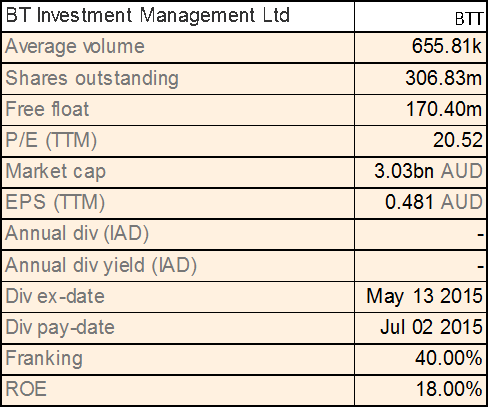

BT Investment Management Ltd

BTT Details

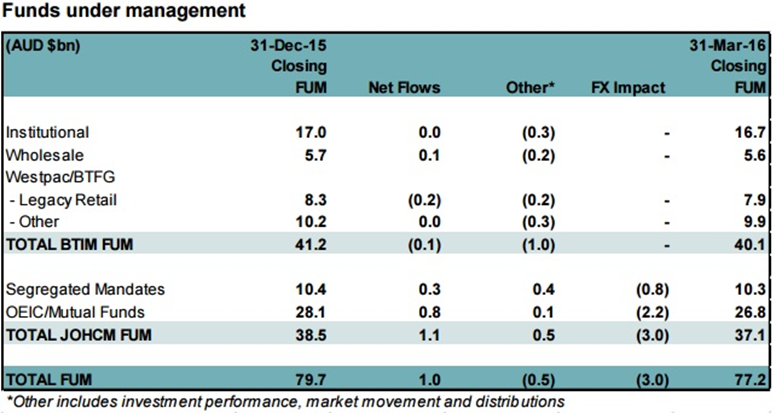

Falling FUM: For the quarter ended March 31, 2016, BT Investment Management Ltd.’s (ASX: BTT) funds under management stood at AUD 40.1 billion compared to AUD 41.2 billion as of December 31, 2015. Meanwhile, JOHCM funds under management decreased to AUD 37.1 billion from AUD 38.5 billion. Recently, the company announced the establishment of an Australian-based Global Equities boutique with a new strategy to expand and complement the group's existing range of global equities strategies.

Funds under management (Source: Company reports)

The establishment of the Global equities boutique requires an investment of $3 to $4 million on an annualized basis upon full implementation of the strategy. BTT is currently trading at a high P/E ratio. Given the above, we rate the stock "Expensive" at the current share price of $10.06

BTT Daily Chart (Source: Thomson Reuters)

K2 Asset Management Holdings Ltd

.png)

KAM Details

Stable FUM: In its recent monthly FUM and Fund performance, K2 Asset Management Holdings Ltd (ASX: KAM) recorded total net outflow of AUD 21.6 in its total funds and funds under management stood at AUD 748.8 million as of April 01, 2016 compared to AUD 745.4 million as of March 01, 2016. KAM is trading at a strong dividend yield and had declared an interim dividend of 1.0 cent per share for half year ended 31 December 2015.

.png)

FUM and Fund Performance (Source: Company reports)

Also, the company has a moderate P/E ratio and has corrected almost 29.10% in the last three month trading session (as of April 22, 2016). In the past 5-day trading, KAM has gone up 5.56% (as of April 22, 2016) and we believe that the stock price may witness further upside and thus we recommend a "Speculative Buy" rating at the current share price of $0.475

KAM Daily Chart (Source: Thomson Reuters)

Wam Capital Ltd

.png)

WAM Details

Stable investment portfolio and dividend growth: In its recent investment update, WAM Capital Limited (ASX: WAM)recorded 3.7% monthly growth in its investment portfolio as of March 31, 2016 compared to 4.7% growth in the S&P/ASX All Ordinaries Accumulation Index. Meanwhile, net tangible assets after tax as of March 31, 2016 stood at 186.12 cents compared to 182.21 cents as of February 2016. Looking ahead, the company believes that its above average cash weighting positions will allow it to capitalize on current market conditions. WAM's stock price has recorded a 6.54% rise (as of April 22, 2016) in the past three month trading session.

.png)

WAM performance as of March 2016 (Source: Company reports)

Trading at a good dividend yield, the company declared an interim dividend of 7.25 cents per share, an increase of 3.6% from prior period. WAM has a reasonable P/E ratio, while the stock price is currently hovering around its 52-week high levels. Based on the foregoing, WAM is expected to increase further and thus the "Hold" rating at the current share price of $2.28

.PNG)

WAM Daily Chart (Source: Thomson Reuters)

Contango Microcap Ltd

.png)

CTN Details

Strong dividend growth: Contango Microcap Ltd (ASX: CTN)recorded net tangible assets of investments before tax of $1.102 as of March 31, 2016 as opposed to $1.056 as at February 29, 2016. NTA after tax for the same period stood at $1.038 against prior month’s $1.004. Interim dividend paid for FY16 stood at $0.026 per share with sufficient company's dividend reserve to pay proposed dividends into FY17.

.png)

Net Tangible Assets March 2016 (Source: Company reports)

The company paid final dividend for FY16 at 3.7 cents per share. In the past three month trading session, the company has recorded a gain of 1.63% (as of April 22, 2016) with a strong dividend yield. Based on the company strong fundamentals, we rate the stock a “BUY” at the current share price of $0.935

.PNG)

CTN Daily Chart (Source: Thomson Reuters)

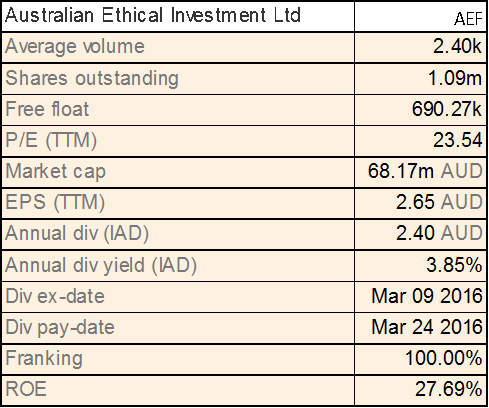

Australian Ethical Investment Ltd

AEF Details

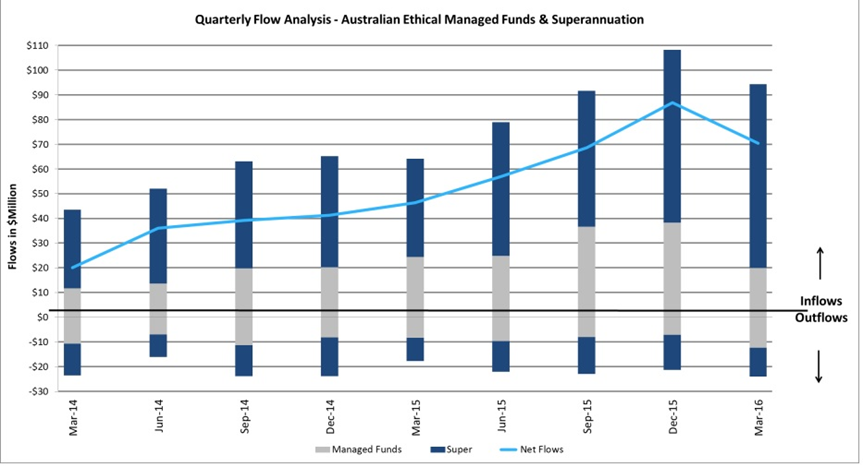

Marginal growth and high valuations: Australian Ethical Investment Limited (ASX: AEF) recorded funds under management of $1,428.0 million for the quarter ended March 31, 2016, an increase of 1.9% from the quarter ended December 31, 2015. The company executive commented that AEF recorded marginal growth over the quarter despite negative market movements due to the significant market volatility through the quarter.

Quarterly cash flow (Source: Company reports)

Also, net flows to the managed funds were impacted by cautious investor sentiment. Net inflows to superannuation fund continued to grow with a 13.1% increase from the prior year quarter. AEF is currently trading at a high P/E ratio and is also close to its 52-week high levels. Based on the above, we rate the stock "Expensive" at the current share price of $62.30

AEF Daily Chart (Source: Thomson Reuters)

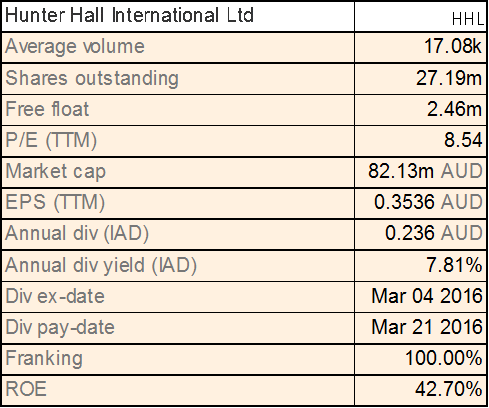

Hunter Hall International Ltd

HHL Details

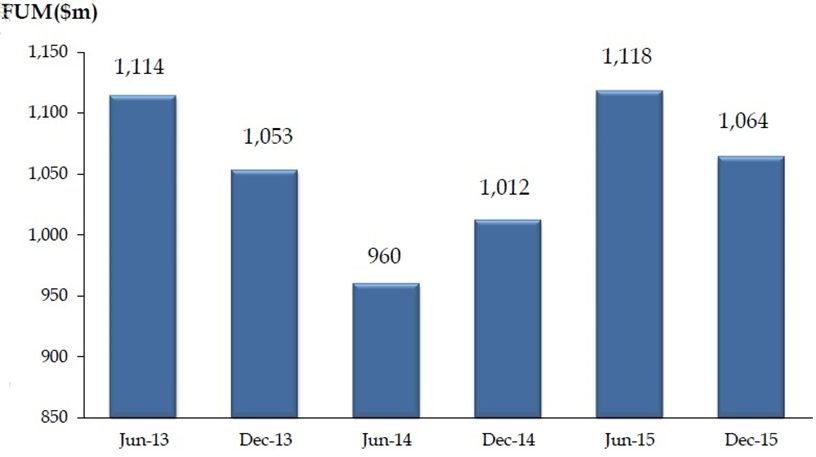

Lower outlook and falling FUM: Hunter Hall International Ltd (ASX: HHL) recorded quarterly funds under management of $1,072.2 million as of March 31, 2016 compared to $1,091 million as of December 31, 2015. For the six months ended December 31, 2015, HHL funds under management rose 5.1% to $1,064 million from year ago period. Operating revenue was up 10.1% in the same period while net profit after tax also surged.

Funds under management (Source: Company reports)

Dividend per share increased to 14.1 cents from prior year period. Looking ahead, operating profit before tax from investment management for six months ending June 30, 2016 is estimated to be 25% lower from the six months ended December 31, 2015 given weak equity market and cost for various initiatives.

HHL reached its 52-week high levels in February 2016 and in the last six month trading session the stock has recorded a 26.02% gain (as of April 22, 2016). Currently trading around its year high levels and a negative outlook, we rate the stock as "Expensive" at the current share price of $3.10

HHL Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2016 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.

AU

AU

Please wait processing your request...

Please wait processing your request...