Hims & Hers Health, Inc

Hims & Hers Health, Inc (NYSE: HIMS) offers a consumer-centric platform designed to meet a wide range of health and wellness needs. The platform features access to a network of healthcare providers, a clinically driven electronic medical records system, digital prescription services, cloud-based pharmacy fulfillment, and advanced personalization tools.

Positive Growth Aspects

- Robust Revenue and Profit Growth: Hims & Hers delivered an impressive 111% year-over-year revenue increase in Q1 2025, reaching USD 586 million, up from USD 278.2 million in Q1 2024. This growth was driven primarily by a 115% surge in online revenue, underscoring the strength of the company's digital-first platform. Net income also expanded significantly to USD 49.5 million, more than quadrupling the USD 11.1 million recorded a year earlier. This momentum reflects strong product-market fit and scalable operations within the health and wellness space.

- Strong Subscriber and ARPU GrowthThe company's subscriber base rose 38% year-over-year to 2.4 million by the end of Q1 2025. Additionally, the average monthly online revenue per subscriber increased by 53% to USD 84, up from USD 55 in the prior-year period. This indicates not only growing reach but also improved monetization per user, aided by enhanced personalization and broader service offerings. Over 1.4 million subscribers now use personalized solutions, showcasing a successful pivot toward tailored care at scale.

- Improved Cash Flow and Profitability Metrics: Hims & Hers posted strong operational cash flow of USD 109.1 million in Q1 2025, a fourfold increase from USD 25.8 million a year ago. Free Cash Flow also rose significantly to USD 50.1 million. Adjusted EBITDA grew from USD 32.3 million in Q1 2024 to USD 91.1 million in Q1 2025, reinforcing management’s disciplined execution and the high operating leverage in its business model. These trends support long-term financial sustainability and provide ample flexibility for reinvestment and expansion.

- Ambitious Long-Term Vision and Upgraded Guidance: Management reaffirmed its full-year 2025 revenue guidance of USD 2.3–USD 2.4 billion and raised its Adjusted EBITDA target to USD 295–USD 335 million. Furthermore, it introduced aggressive 2030 financial targets of at least USD 6.5 billion in revenue and USD 1.3 billion in Adjusted EBITDA. These projections, backed by consistent past performance, reflect confidence in continued expansion across specialties, geographies, and service depth. The company’s evolving ecosystem, driven by personalized, accessible care and strategic partnerships, positions it well for future industry leadership.

Growth Challenges

- Decline in Gross Margin: Despite revenue and profitability gains, gross margin declined notably to 73% in Q1 2025 from 82% in the same quarter last year. This erosion may reflect increased cost of goods sold, rising customer acquisition costs, or deeper investments in personalized care services. If not stabilized, the margin compression could limit future earnings growth and signal pricing or operational pressures amid scaling efforts.

- Stagnant or Declining Wholesale Business: The wholesale revenue segment dropped by 7% year-over-year, falling from USD 10.4 million to USD 9.6 million. While this is a relatively small portion of total revenue, the decline may suggest reduced demand from third-party retailers or a deprioritization of B2B distribution. The company appears increasingly reliant on its direct-to-consumer model, which, while scalable, exposes it to digital advertising volatility and consumer behavior shifts.

- Q2 Revenue and Profit Expectations Below Q1: Guidance for Q2 2025 anticipates revenue between USD 530 million and USD 550 million, which is lower than Q1's USD 586 million figure. This sequential dip may raise concerns over growth momentum and seasonal volatility. Additionally, Q2 Adjusted EBITDA is expected to decline to USD 65–USD 75 million from Q1’s USD 91.1 million. This suggests increased short-term investments or operational costs that may pressure near-term profitability.

- High Long-Term Targets Could Be Challenging: While the 2030 targets are ambitious and inspiring, achieving USD 6.5 billion in revenue and USD 1.3 billion in Adjusted EBITDA requires sustaining a high growth trajectory for five more years. This level of sustained expansion demands flawless execution, strategic agility, and resilience against regulatory, competitive, and macroeconomic risks. Any disruption in subscriber growth, margin stability, or partner collaboration could impede the path toward these goals.

Hims & Hers Health, Inc. reported a strong Q1 2025, with revenue soaring 111% year-over-year to USD 586 million and net income quadrupling to USD 49.5 million, driven by rapid subscriber growth and increased average revenue per user. The company also raised its full-year Adjusted EBITDA guidance and introduced ambitious 2030 targets, reflecting confidence in its scalable, personalized care model. However, the decline in gross margin from 82% to 73%, a drop in wholesale revenue, and lower sequential guidance for Q2 highlight potential near-term pressures and execution risks. Overall, while growth prospects remain compelling, margin pressures and ambitious long-term goals warrant cautious optimism.

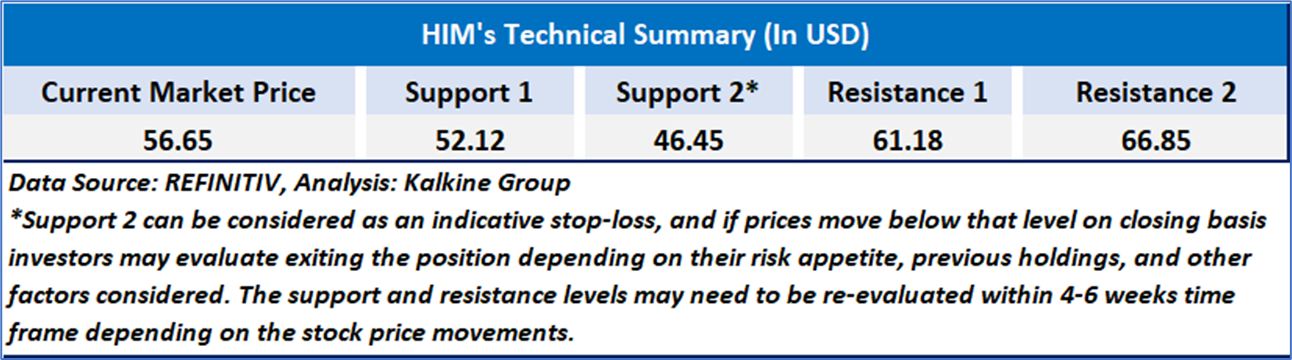

As per the above-mentioned price action, recent key business and financial updates, momentum in the stock over the last month, and technical indicators analysis, a ‘Watch’ rating has been given to Hims & Hers Health, Inc (NYSE: HIMS) at the current market price of USD 56.65 as of July 24,2025 at 9:10 am PDT.

Individuals can evaluate the stock based on the support and resistance levels provided in the report in case of keen interest taking into consideration the risk-reward scenario.

Markets are trading in a highly volatile zone currently due to certain macro-economic issues and prevailing geopolitical tensions. Therefore, it is prudent to follow a cautious approach while investing.

Related Risk: This report may be looked at from a high-risk perspective and a recommendation is provided for a short duration. This report is solely based on technical parameters, and the fundamental performance of the stocks has not been considered in the decision-making process. Other factors which could impact the stock prices include market risks, regulatory risks, interest rates risks, currency risks, social and political instability risks etc.

Note 1: Past performance is not a reliable indicator of future performance.

Note 2: The reference date for all price data, currency, technical indicators, support, and resistance level is July 24,2025. The reference data in this report has been partly sourced from REFINITIV.

Note 3: Investment decisions should be made depending on an individual's appetite for upside potential, risks, holding duration, and any previous holdings. An 'Exit' from the stock can be considered if the Target Price mentioned as per the Valuation and or the technical levels provided has been achieved and is subject to the factors discussed above.

Note 4: Target Price refers to a price level that the stock is expected to reach as per the relative valuation method and or technical analysis taking into consideration both short-term and long-term scenarios.

Note 5: ‘Kalkine reports are prepared based on the stock prices captured either from the New York Stock Exchange (NYSE), NASDAQ Capital Markets (NASDAQ), and or REFINITIV. Typically, all sources (NYSE, NASDAQ, or REFINITIV) may reflect stock prices with a delay which could be a lag of 15-20 minutes. There can be no assurance that future results or events will be consistent with the information provided in the report. The information is subject to change without any prior notice.

AU

AU

Please wait processing your request...

Please wait processing your request...