GDEV Inc

GDEV Inc (NASDAQ: GDEV) is a Cyprus-based global digital gaming company. It is a gaming and entertainment powerhouse, focused on growing and enhancing its portfolio of studios. The Company builds mobile, web and social games for millions of players globally, that are free of charge. GDEV’s core product - Hero Wars, offers a suite of games across mobile, social and web-based platforms.

Key Business and Financial Updates:

- GDEV Inc. Q2 and H1 2025 Financial Overview: GDEV Inc. (NASDAQ: GDEV), a prominent international gaming and entertainment entity based in Limassol, Cyprus, disclosed its financial and operational outcomes for the second quarter and first half of 2025, concluded on June 30, 2025, on September 2, 2025. The company reported a second-quarter revenue of USD 120 million, reflecting a 13% year-over-year increase, and a first-half revenue of USD 217 million, up 2% from the prior year, underpinned by growth in in-app purchase revenue despite declines in advertising bookings. Financial highlights include a net profit of USD 17 million in Q2 2025, up from USD 15 million in Q2 2024, and USD 31 million for the first half, a significant rise from USD 9 million, with Adjusted EBITDA improving to USD 22 million and USD 38 million, respectively, indicating enhanced operational efficiency.

- Detailed Financial Performance Analysis: In the second quarter of 2025, GDEV’s revenue growth of USD 14 million was primarily driven by a surge in consumable in-app purchases, though partially offset by reduced advertising bookings, with platform commissions rising 10% to USD 25 million and game operation costs remaining stable at USD 14 million. Selling and marketing expenses increased by 11% to USD 53 million due to experimental performance marketing strategies, while general and administrative expenses held steady at USD 9 million, contributing to a USD 5 million increase in Adjusted EBITDA to USD 22 million; however, cash flows turned negative at USD 10 million compared to a positive USD 11 million in Q2 2024, largely due to decreased bookings and higher marketing costs. For the first half, revenue growth of USD 4 million was similarly fueled by in-app purchases, with platform commissions dropping 2% to USD 46 million and game operation costs rising to USD 28 million from IT infrastructure investments, while selling and marketing expenses decreased 14% to USD 95 million due to a shift toward efficiency-focused user acquisition, supporting a USD 22 million Adjusted EBITDA increase to USD 38 million despite a negative cash flow of USD 4 million.

- Operational Performance and Market Positioning: GDEV’s operational metrics for the second quarter and first half of 2025 revealed a 14% and 20% decline in bookings to USD 92 million and USD 173 million, respectively, compared to USD 108 million and USD 216 million in 2024, driven by an 18% and 26% drop in monthly paying users (MPU) to 312,000 and 284,000, respectively, reflecting reduced user acquisition spending. The share of advertising bookings fell to 5.9% from 6.2% in Q2 and 6.9% in the first half of 2024, influenced by a global decline in cost-per-mille (CPM) rates, while average bookings per paying user (ABPPU) improved 5% to USD 93, indicating higher per-user revenue potential. Geographically, the company maintained a stable booking split with a slight decrease in Asia’s share to 19-20% and an increase in Europe to 32%, alongside a consistent 63% mobile platform dominance in Q2 2025, up from 58% in Q2 2024, reflecting a strategic pivot toward mobile gaming markets.

- Strategic Financial Management and Resource Allocation: The company’s robust cash position of USD 932 million as of Q2 2025 provides substantial resources for future strategic investments, bolstered by a first-half net finance income of USD 3 million compared to a USD 2 million expense in 2024, enhancing financial flexibility. Despite negative cash flows in both periods—USD 10 million in Q2 and USD 4 million in the first half—due to booking declines and marketing adjustments, the overall profit growth and Adjusted EBITDA improvement signal effective cost management and a focus on high-margin revenue streams. This financial stability, combined with a diversified revenue base, positions GDEV to navigate market volatility and pursue growth opportunities.

- Market and Competitive Dynamics: GDEV’s performance reflects a strategic response to shifting market dynamics, with the increased mobile platform share to 63% in Q2 2025 indicating a successful adaptation to consumer preferences, while the decline in advertising revenue highlights broader industry trends of softening CPM rates. The company’s ability to maintain geographic stability, with Europe’s share rising to 32% and Asia’s declining to 19-20%, suggests a balanced global presence, though the 26% drop in MPU underscores challenges in user retention amid reduced acquisition efforts. These factors, alongside partnerships and innovation in gaming, position GDEV competitively, though sustained growth will depend on reversing booking declines.

- Forward-Looking Outlook and Challenges: Looking ahead, GDEV’s leadership remains optimistic about leveraging its strong cash reserves and AI-driven gaming innovations to drive long-term profitability, with the Q2 profit increase and Adjusted EBITDA growth signaling a solid foundation despite operational cash flow pressures. The company’s focus on efficiency in user acquisition and investment in mobile platforms could enhance market penetration, though the negative cash flow and declining bookings pose short-term risks that require strategic addressal. The evolving regulatory and economic landscape, including tariff impacts and global market trends, will be critical in shaping GDEV’s trajectory as it seeks to capitalize on its entertainment and gaming leadership.

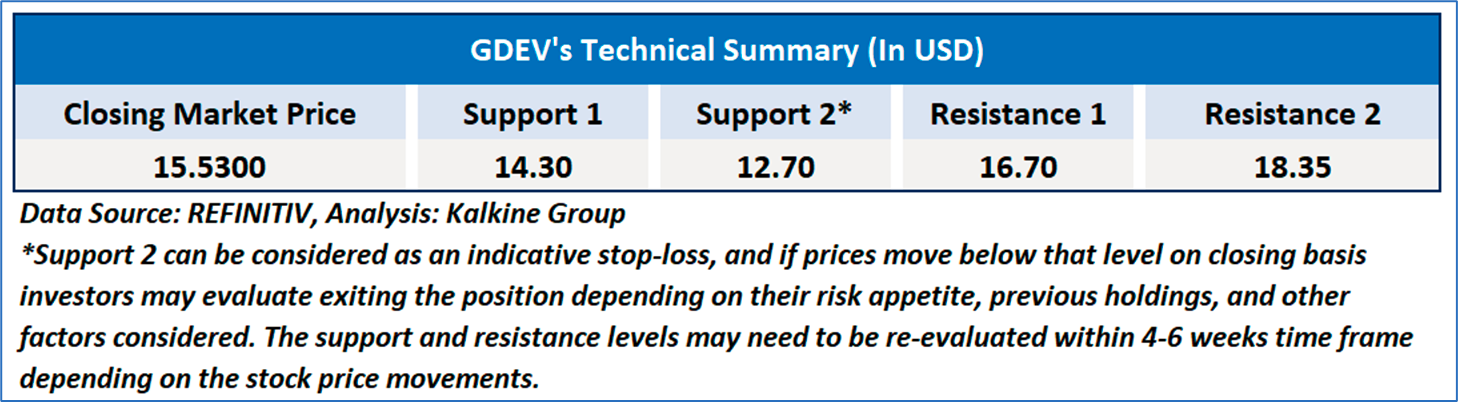

Technical Observation (on the daily chart):

The Relative Strength Index (RSI) over a 14-day period stands at a value of 57.89, upward trending, with expectations of a consolidation or a downward correction if the stock price fails to break the important resistance of USD 16.00-USD 17.00. Additionally, the stock's current positioning is above the 50-period SMA and 200-period SMA, which may serve as dynamic short to medium-term support levels.

GDEV Inc. (NASDAQ: GDEV) reported its financial and operational results for the second quarter and first half of 2025, ended June 30, 2025, with revenue increasing 13% to USD 120 million in Q2 and 2% to USD 217 million in the first half, driven by growth in in-app purchases despite declines in advertising bookings. The company recorded a net profit of USD 17 million in Q2, up from USD 15 million, and USD 31 million in the first half, up from USD 9 million, with Adjusted EBITDA rising to USD 22 million and USD 38 million respectively, though cash flows turned negative at USD 10 million in Q2 and USD 4 million in the first half due to reduced bookings and marketing adjustments. Operational metrics showed a 14% and 20% drop in bookings to USD 92 million and USD 173 million, respectively, alongside an 18% and 26% decline in monthly paying users, offset by a 5% increase in average bookings per paying user to USD 93, while the mobile platform share rose to 63% in Q2, reflecting a stable geographic split with a slight shift toward Europe, supported by a robust cash position of USD 932 million.

As per the above-mentioned price action, important resistance near USD 16.00-USD17.00, momentum in the stock over the last month, and technical indicators analysis, a ‘WATCH’ rating has been given for GDEV Inc (NASDAQ: GDEV) at the closing price of USD 15.53, as of September 02, 2025.

Individuals can evaluate the stock based on the support and resistance levels provided in the report in case of keen interest taking into consideration the risk-reward scenario.

Markets are trading in a highly volatile zone currently due to certain macro-economic issues and prevailing geopolitical tensions. Therefore, it is prudent to follow a cautious approach while investing.

Related Risk: This report may be looked at from a high-risk perspective and a recommendation is provided for a short duration. This report is solely based on technical parameters, and the fundamental performance of the stocks has not been considered in the decision-making process. Other factors which could impact the stock prices include market risks, regulatory risks, interest rates risks, currency risks, social and political instability risks etc.

Note 1: Past performance is not a reliable indicator of future performance.

Note 2: The reference date for all price data, currency, technical indicators, support, and resistance level is September 02, 2025. The reference data in this report has been partly sourced from REFINITIV.

Note 3: Investment decisions should be made depending on an individual's appetite for upside potential, risks, holding duration, and any previous holdings. An 'Exit' from the stock can be considered if the Target Price mentioned as per the Valuation and or the technical levels provided has been achieved and is subject to the factors discussed above.

Note 4: Target Price refers to a price level that the stock is expected to reach as per the relative valuation method and or technical analysis taking into consideration both short-term and long-term scenarios.

Note 5: ‘Kalkine reports are prepared based on the stock prices captured either from the New York Stock Exchange (NYSE), NASDAQ Capital Markets (NASDAQ), and or REFINITIV. Typically, all sources (NYSE, NASDAQ, or REFINITIV) may reflect stock prices with a delay which could be a lag of 15-20 minutes. There can be no assurance that future results or events will be consistent with the information provided in the report. The information is subject to change without any prior notice.

AU

AU

Please wait processing your request...

Please wait processing your request...