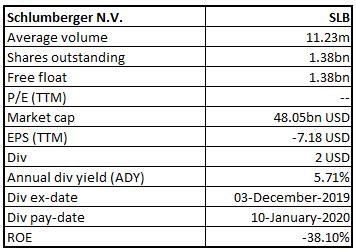

Schlumberger N.V.

SLB Details

Top-line Growth on the Face of Macro Challenges:Schlumberger N.V. (NYSE: SLB) is the world’s leading provider of technology for reservoir characterization, drilling, production, and processing to the oil and gas industry. The company deals with a wide range of products and services, from exploration through production and integrated pore-to-pipeline solutions that optimize hydrocarbon recovery to deliver reservoir performance.

Recent Updates:During Q3FY19, SLB issued EUR 500 million of 0.00% Notes due 2024, EUR 500 million of 0.25% Notes due 2027, and EUR 500 million of 0.50% Notes due 2031. The company repurchased $783 million of its outstanding 3.000% Notes due 2020 and $321 million of its outstanding 3.625% Notes 2022.

Dividend Distribution:SLB announced a quarterly cash dividend of $0.50 per share of outstanding common stock, payable on January 10, 2020.

Q3 Financial Highlights for FY19 for the period ended 30 September 2019:SLB announced its third-quarter result for FY19, wherein the company reported total revenue of $8,541 million as compared to $8,504 million in Q3FY18. The company reported a net loss of $11,383 million as compared to a profit of $644 million in the previous corresponding period. The reported loss was mainly due to the inclusion impairment and other charges of $12,692 million. International revenue came in at $5.6 billion, increased 3% sequentially, while North America revenue stood at $2.8 billion, increased 2% on q-o-q basis.

The company reported net income, excluding charges & credits at $596 million, down 7% on $644 million in the prior corresponding period, while up 21% on a sequential basis. Diluted EPS, excluding charges & credits, came in at $0.43, increased 23% sequentially, however, declined 7% on Y-o-Y basis.

.png)

Q3FY19 Income Statement (Source: Company Reports)

On Q-o-Q basis, the SLB’s international segment was led by the Europe/CIS/Africa area, where revenue increased 9% on Q-o-Q basis, aided by peak summer activity in the Northern Hemisphere and commencement of new projects in Africa.Within the International segment, the business witnessed double digit growth in Asia, and a 9% decline on q-o-q basis in Argentina and Mexico.

Outlook:Going forward, underpinned by the elements of its strategy, the company is favorably positioned to achieve superior margin expansion, increased return on capital, and growth in free cash flow. The company expects FY19 full-year CAPEX within $1.6 billion to $1.7 billion.

Stock Recommendation:The stock of SLB is quoting at $34.71, with a market capitalization of $48.05 billion. The EBITDA margin of SLB stood at 20%, higher than the industry median of 17.3%. Despite macro- environment challenges and lower CAPEX allocation from the oil manufacturers across North America, the company delivered a sequential growth of 3% in its top-line. SLB reported high single-digit international revenue growth during the quarter, underpinned by international investment levels. The stock is available at the enterprise value (EV) to sales multiple of 1.9x on trailing twelve months (TTM) basis as compared to the industry median of 2.0x. Considering the top-line growth, expansion in adjusted net income, better than industry margins, business prospects and current valuations, we recommend a “Buy” rating on the stock at the current market price $34.71, down 0.91% as on 14 November 2019.

SLB Daily Technical Chart (Source: Thomson Reuters)

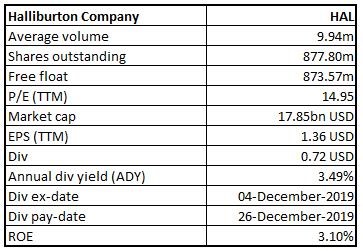

Halliburton Company

HAL details

Operational Efficiency Lead to Higher Profitability:Halliburton Company (NYSE: HAL) is one of the world's largest providers of products and services to the energy industry. The company repurchased approximately 4.5 million shares of common stock under the share repurchase program at a total cost of $100 million.

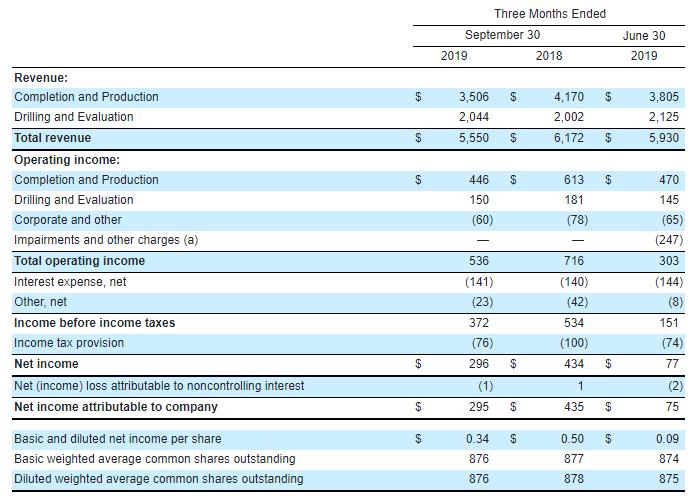

Q3FY19 Operating Highlights for the period ended 30 September 2019: HAL announced its third-quarter results, wherein the company reported revenue of $5,550 million as compared to $6,172 million in Q3FY18. Net income stood at $296 million as compared to $77 million in 2QFY19, on account of improved operational efficiency.HAL reported activities within the business segments were significantly affected by lower spending on upstream exploration, development and production programs by the clients. Lower worldwide consumption of oil and natural gas led to lower business activity. During the quarter, the company reported $3,506 million of revenue from the completion and production segment as compared to $4,170 million in the previous corresponding period. Drilling and Evaluation reported revenue of $2,044 million as compared to $2,002 million in Q3FY18.

Q3FY19 Income Statement Highlights (Source: Company Reports)

Guidance:The company expects FY19 capital expenditures at ~$1.6 billion, a 20% decline from FY18, with most of the reduction coming from North America. As per the management commentary, the company is likely to reduce its capital expenditures further in FY20. The company is observing the current demand scenario, and it is expected to alter its capital investment accordingly.

Stock recommendation:The stock of HAL is quoting at $20.33, with a market capitalization of $17.845 billion. HAL generated ROE of 3.1% in 3QFY19, higher than the industry median of 0.8%. The stock is available at an EV/Sales multiple of 1.2x on TTM basis as compared to the industry median of 2.0x. The company is seeking additional ways to become one of the most cost-efficient service providers in the industry by optimizing costs, maintaining capital discipline and leveraging the scale and breadth of operations. HAL is looking to collaborate with engineering solutions to maximize the asset value of its clients. Considering the return ratio, current valuations, and operational efficiencies, we recommend a ‘Buy’ rating on the stock at the current market price of $20.33, down 1.41% as on 14 November 2019.

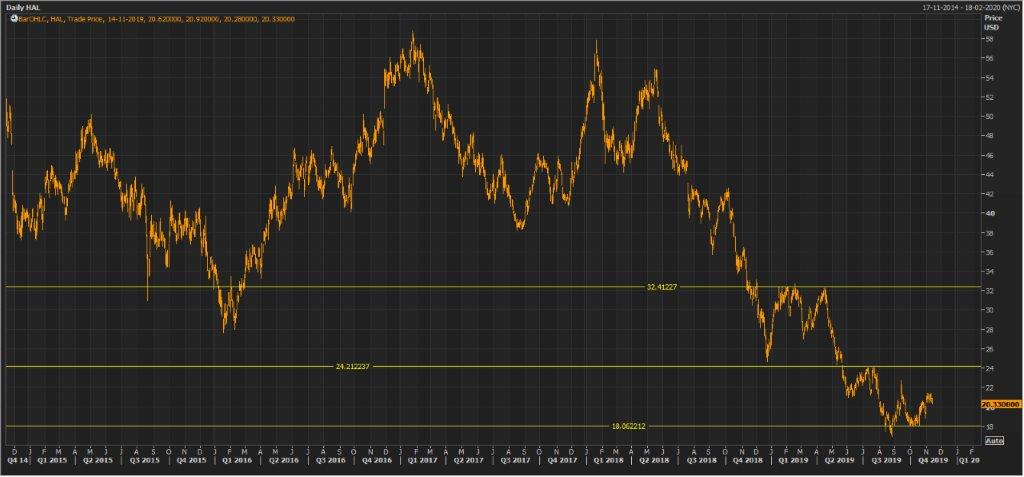

HAL Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...