Aristocrat Leisure Limited

Growth Enabling Business Model:Aristocrat Leisure Limited (ASX: ALL) is engaged in designing, developing, and distribution of gaming contents to electronic gaming machines, casino management systems, and digital social games. The headquarter of the company is situated in Sydney, Australia, and it is being currently headed by Mr. Trevor Croker – the Chief Executive Officer (CEO) and Managing Director (MD).

Legal proceedings against Ainsworth Game Technology Limited (AGT):Recently, ALL entered a legal battle with Ainsworth Game Technology Limited (“Ainsworth”) claiming infringement of intellectual property rights and breach by AGT of the Australian Consumer law. In the meantime, Ainsworth will be denying the claims made by Aristocrat in the proceedings.

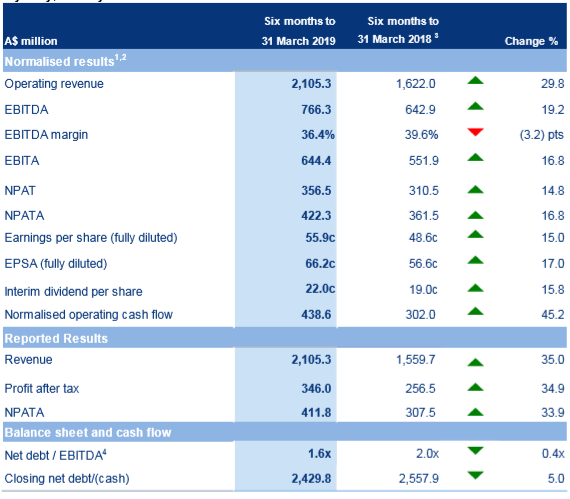

1H FY19 performance highlights: During 1HFY19, ALL posted its revenue at $2,105.3 million, up 29.8% on y-o-y basis. EBITDA came in at $766.3 million, up 19.2% on y-o-y, while EBITDA margin witnessed a fall from 39.6% to 36.4%.

During the period, NPAT stood at $356.5 million, up 14.8% as compared with $310.5 million in the prior corresponding period. ALL posted normalised operating cash flow of $439 during H1FY19 as compared with $302 million in 1H18. Gearing ratio reduced to 1.6x at 31 March 2019, from 2.0x (pro-forma). The company improved its operational efficiency along with operating cash flows, which resulted to lower leverage ratio.

1H19 Financial Highlights (Source: Company Reports)

Outlook: Revenue from North America is likely to grow at a decent pace in the coming months, followed by higher realisation from land-based Gaming segment. The Management expects growth in Digital bookings due to several new game releases. User Acquisition spend is likely to remain at around 25% to 28% of total Digital revenues. On the taxation part, the company anticipates a reduction of 100 – 150 bps from FY18. Due to a more diversified portfolio, earnings are expected to be skewed to the second half of FY19.

Stock recommendation: Stock of ALL is quoting at $28.010 with an average annual volume of~2,181,843. The stock has delivered a healthy return of 14.05% and 16.19% during the last three and six months, respectively. On YTD, the stock has gained 37.99%. On the valuation front, its EV/EBITDA, EV/Sales and Price to Cash Flow multiple (on TTM basis) stand at 13.9x, 5.0 and 16.9x, higher than the industry median of 9.5x, 1.8x, and 11.8x, respectively, indicating the overvalued position at the current juncture. Hence, considering the aforesaid facts coupled with decent returns in the recent past, and higher valuation at the current levels, we have a wait and watch stance on the stock at the current market price of A$28.010 per share (down 3.613% on 15 August 2019).

Lovisa Holdings Limited

Continued roll out of International Store:Lovisa Holdings Limited (ASX: LOV) is engaged in selling of jewellery and related items through retailing. The company has its retail presence across Australia, New Zealand, Malaysia, Singapore, Spain, France, the United Kingdom, and the USA. Currently, the company has 366 stores, which are engaged in selling fashion jewellery. The company is headquartered at Victoria, Australia.

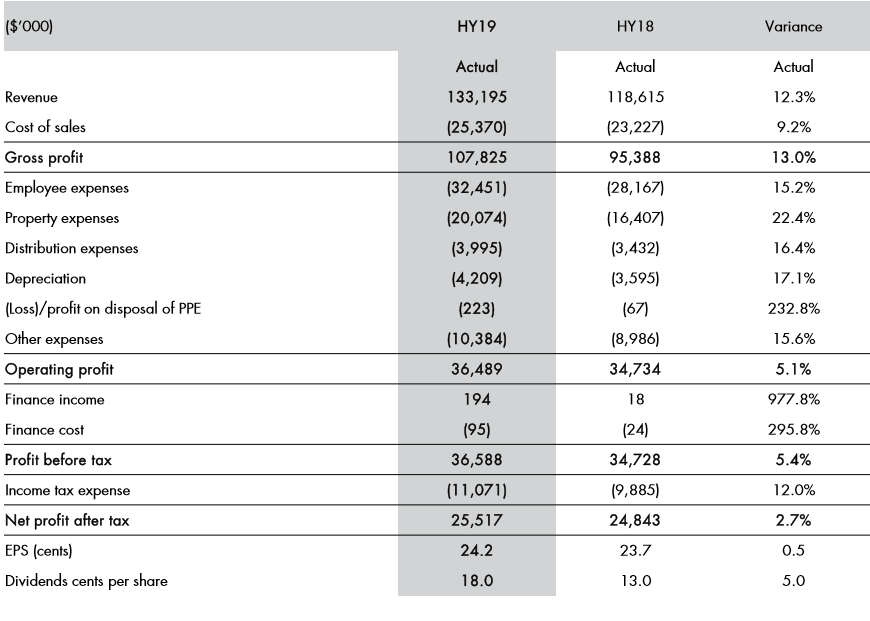

H1 FY19 performance highlights:During the first half of FY19, LUV posted revenue of $133.2 million, with yoy growth of 12.3%. Gross profit and EBITDA stood at $ 107.8 million, up by 13% and $40.69 million, up by 6.2%, respectively. Depreciation during the first half was up by 17.1%, followed by a 12% increase in taxation. PAT during H1FY19, came in at $ 25.51 million vs. $ 24.84 million a year ago. Capital expenditure stood at $12.5 million for the half year, including payments of $ 0.3 million for key money. Dividend amounted to $14.8 million was paid during H1FY19, an 84% increase on FY18 final dividend. Cash in hand stood at $ 32.28 million, a bit lower than $ 33.03 million during H1FY18. The company added net 40 stores during the first half of FY19. Gross Margin increased 60bps to 81.0% as the company continued to benefit from higher USD hedge rates during the period.

1H19 Performance (Source: Company Reports)

Growth in the European and US markets accelerated during the period, with 12 new stores in the UK, 8 stores now trading in Spain, 7 in France, and 8 in the US. South Africa performed well, with sales up 10.5% for the period aided by additional stores opened as well as comparable store sales growth.

Outlook: The Management is likely to remain focused on strong gross to be maintained with cost to be well controlled while investing in the future growth of the business. The Management also expects currency headwinds to have an impact lately in FY19 and into FY2020 as the average USD hedge rate reduces.

Stock recommendation: At the current market price of $11.10, stock of LOV is trading at P/E multiple of 31.80x against the industry median of 10.9x. EV/ EBITDA on TTM basis is at 20.3x against 6.7x of the industry average. The stock has delivered decent returns of 72.83% on YTD. Based on the results for 1H19 and the sharp gain in the recent times, we have a watch stance on the stock at the current market price of $11.100, up 0.452% as on 15 August 2019, ahead of its full-year results which are to be released on 22 August 2019.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...