Harvey Norman Holdings Limited

.JPG)

HVN Details

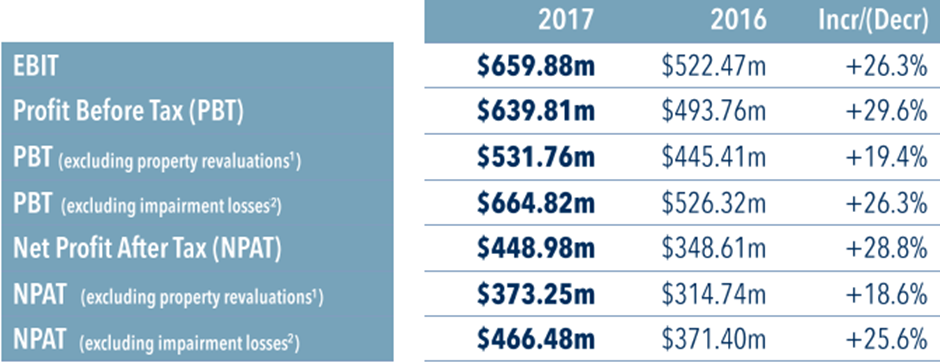

Stock tumbled on dividend cut despite solid results: Harvey Norman Holdings Limited (ASX: HVN) posted 28.8% year on year (yoy) growth in net profit after tax at $448.9 million. Profit before tax increased by 29.6% to $639.8 million; while excluding net property revaluation increments, it grew 19.4% to $531.8 million. Further, a $17.7 million (24.3% up) increase in the company-operated retail segment was reported and this was led by strong improvements in the results of retail operations in New Zealand, Singapore, Malaysia, Ireland, Northern Ireland, Slovenia and Croatia. Similarly, a $36.4 million (13.6% up) increase in the profitability of the franchising operations segment was reported. Net property revaluation increments of $108.0 million delivered an increase of $59.7 million over the net property revaluation increment of $48.4 million recognised in the previous year.

Financial performance; (Source: Company reports)

In Australia, franchisee headline aggregated sales revenue has increased by 5.4% to $5.6 billion compared to the 2016 financial year. This solid growth in franchisee sales reflecting retail spending remains above decade averages, particularly in NSW and Victoria, underpinned by strong housing sector activity, lower levels in unemployment, a net increase in overseas migration, and the wealth flow-on effect from higher home prices. The strong growth in franchisee sales contributed to a 13.6% increase in the result from the franchising operations segment to $304.5 million from $268.2 million in the previous year.

The stock has tumbled 7.5% on 31 August 2017, as the company reduced its dividend payment to 26 cents for FY17 vs 30.0 cents in FY16. Given the intensifying competition in the sector at the back of entry of retail giant Amazon, we maintain an “Expensive” recommendation on the stock at the current price of $ 4.08

JB Hi-Fi Limited

.JPG)

JBH Details

Rising headwinds due to competition: JB Hi-Fi Limited (ASX: JBH) stock dropped nearly 2% on 31 August 2017 in line with peers post the Harvey Norman Holdings results. There have been updates/ changes in substantial holdings from Challenger Ltd and UBS group. The company had reported 36.5% yoy growth in FY17 underlying profit at $207.7 million (FY16: $152.2 million) on $5.6 billion of sales (FY16: $3.95 billion) for the full year ended 30 June 2017. Total sales grew by 42.3% yoy while group EBIT was up 38.5% on the pcp to $306.3 million. However, Australian sales witnessed subdued growth at 10.9% to $4.15 billion, with comparable sales up 8.6%, led by the Communications, Audio, Cameras, Accessories, Computers and Home Appliance categories. In FY17, online sales grew 38.4% to $158.9 million or 3.8% of total sales, reflecting continuous improvement across many aspects of the business’s digital assets. Given the increasing costs to sustain the revenue and rising headwinds in the sector, we give an “Expensive” recommendation on the stock at the current price of $ 23.13

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...