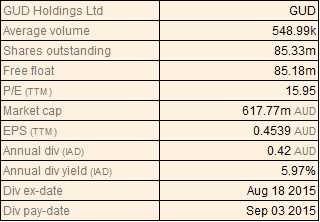

GUD Holdings Ltd

GUD Dividend Details

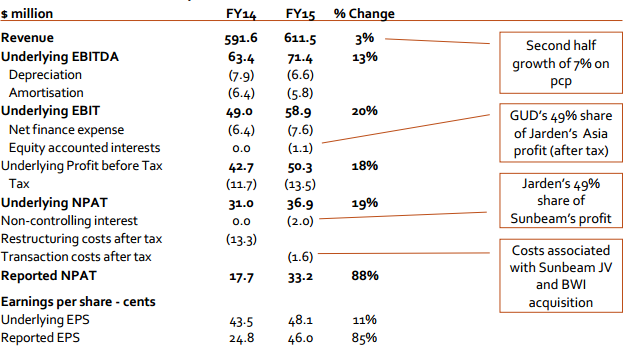

Weak consumer sentiment to impact business despite growth efforts: GUD Holdings Limited (ASX: GUD) reported that its revenues rose to $611.5 million in fiscal year of 2015, as compared to $591.6 million in fiscal year of 2014 driven by the improved performance across all of its segments (except Sunbeam). Accordingly, GUD’s attributable profit rose by 88% year on year (yoy) to $33.2 million. GUD acquired Brown & Watson to enhance its activity automotive aftermarket business and hence rose $101.5 million in new equity. GUD’s Sunbeam segment made a joint venture with Jarden Consumer Solutions to enhance its business in over 20 countries ranging from India to New Zealand in 2015.

Financial Summary (Source: Company Reports)

However, with the ongoing subdued consumer sentiment, GUD’s business might get affected during the spring selling season and Christmas trading season of the year impacting its FY16 outlook. Moreover, falling Australian dollar would also pose further pressure to the group. During its AGM, the group announced that its FY16 underlying EBIT is expected to be around $90 million which is little lower than the consensus value. The shares of GUD plunged over 20.48% (as of November 13, 2015) in the last four weeks and we believe the negative sentiment in the stock to continue in the coming months. Also, the stock is trading at a very high P/E ratio of 15.28x. Based on the foregoing, we give an “Expensive” recommendation to the stock at the current price of $7.03

GUD Daily Chart (Source: Thomson Reuters)

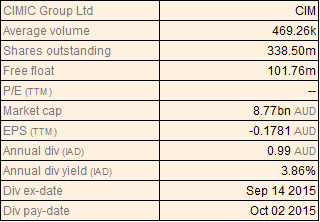

Cimic Group Ltd

CIM Dividend Details

Improvement in cash flow and margins: Cimic Group Ltd (ASX: CIM), which is a construction giant (formerly called Leighton) insists that it is not rejecting its history in spite of the name change which comes in the midst of allegations of corruption overseas. The company will now be known as CIMIC Group and the new name stands for Construction, Infrastructure, Mining and Concessions. There have been a number of calls for a Senate enquiry against Leighton Holdings, Leighton Offshore and Thiess. Nonetheless, CIM is all set to deliver gas infrastructure for QGC in Queensland’s Surat Basin in view of the recent contract win worth $250 million in revenues.CIM has also repurchased approximately 16.5 million shares at an average weighted price of $13.94 under its buy-back program. Then the off-market takeover offer by CIM for all the ordinary shares of Devine Limited at $0.75 cash per share is yet to see the light of the day.

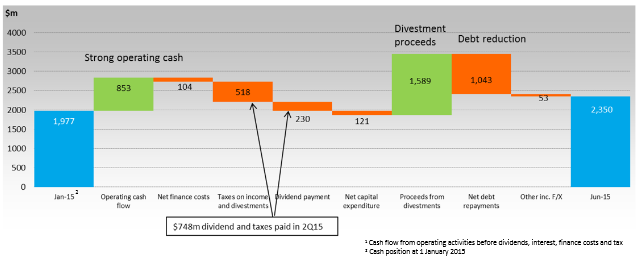

Cash Flow (Source: Company Reports)

The company has announced a significant improvement in operating cash flow, margins and profit for the nine months to 30 September 2015. The highlights of the results include strong NPAT up 25% over the previous year, operating cash flow of $ 1.35 billion for the year to date and new work for the year to date of $ 11.34 billion with total work in hand of $ 28.8 billion. EBIT of $ 650 million was up 13.7% over the previous period. EBIT and NPAT margins were 6.2% and 3.8%, respectively, representing increases over the previous period of 160 and 130 basis points. The increases in the third quarter were up 170 and 210 basis points, respectively, over the same quarter of the previous year. Of the operating cash flow, $ 500 million came in the third quarter while net capital expenditure for the three quarters was reduced by $ 331 million compared to the same period of the previous year. During the third quarter, net debt (including operating leases) improved from $ 215 million with a gearing of 5.3% as of 30 June 2015 to net cash position of $ 108 million as of 30 September 2015. New work improved significantly in the third quarter increasing by $ 4.34 billion and, in addition, the company is participating in tenders of approximately $ 10 billion which are expected to be awarded in the fourth quarter of 2015. The company is also confirmed that, subject to market conditions, the guidance of NPAT for FY 2015 in the range of $ 450 million - $ 520 million continues.

Executive chairman and CEO Verdes said that the growing profit during the third quarter reflects the ongoing transformation of the group. The company is delivering steady and sustainable increases in margins and continuing its focus on cash collection, the reduction of net debt and improving the working capital position. In construction, the company was selected as the preferred contractor for the new $ 5 billion MS motorway in Sydney in a joint venture and was awarded contracts for level crossing removals in Victoria and the design and construction of improvements on State Highway 1 in New Zealand. The company has continued to diversify winning a nickel mining project for BHP Billiton and has launched FleetCo, an international mining equipment business offering Australia’s most diverse range of mining equipment hire.

Though the increase in margins and the size of the order book look impressive, we believe that the stock is expensive at the current price.

CIM Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people.Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation.Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product.The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2014 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.

AU

AU

Please wait processing your request...

Please wait processing your request...