Metcash Limited

.JPG)

MTS Details

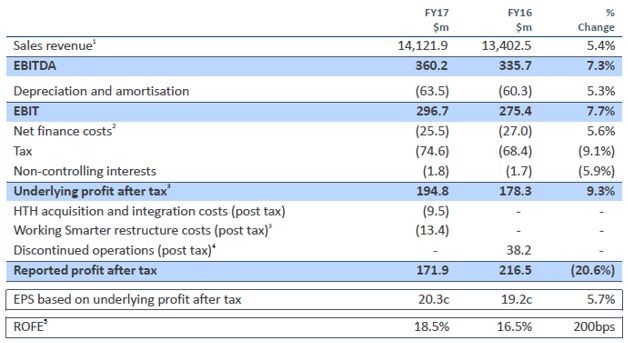

· Weak profit after tax in FY 17: Metcash Limited (ASX: MTS) has announced that Jeff Adams would succeed Ian Morrice as the company’s Group Chief Executive Officer. Mr. Morrice had notified the company of his intention to retire in 2018, after the completion of five years in the role. Mr. Adams will join MTS in September and, after a comprehensive orientation of the business, and would work with Mr. Morrice to ensure a smooth transition into the role. He will succeed Mr. Morrice as Group Chief Executive Officer after the completion of the transition in December. Mr. Morrice will then act as an adviser to Mr. Adams and the Board through to June 2018. On the other side, in FY 17, MTS has reported 5.4% growth in the group sales revenue to $14.12bn and 9% increase in the underlying net profit after tax to $194.8m. The group EBIT grew by 8% to $296.7m (including 53rd trading week and acquisition of HTH. However, the reported profit after tax fell by 20.6%. Additionally, in Liquor segment, there is a modest industry growth, due to the consumer habits, that is shifting to less volume consumption but higher quality. There is an elevated level of competition due to the large retailers and there are difficult trading conditions in Western Australia. But MTS is trying to take initiatives to help minimize the impact of difficult market conditions including price deflation, cost inflation

FY 17 Financial Performance (source: Company Reports)

· Stock performance: Overall, in Liquor market, MTS is expecting moderate growth and is focusing on building and improving the quality of its IBA bannered network. In Hardware segment, the market is competitive. Masters stock liquidation had negatively affected the hardware market in late 2016. The segment is on track to get synergy benefits at upper end of $15-$20m (annualized) target range by end FY18, after sharing benefits with retailers. FY18 will also include a full year of earnings from HTH. Further, in Food, the sales are impacted by the competitive pressure and unfavorable economic conditions in Western Australia in the first six weeks trading of FY18, and it is expected that these external economic conditions will continue. MTS stock has risen 15.4% in the last four weeks as on July 17th, 2017 and we believe investors could leverage this rise as a profit booking opportunity. We give an “Expensive” recommendation on the stock at the current price of $2.52

.jpg)

MTS Daily chart; (Source: Thomson Reuters)

Qantas Airways Limited

.JPG)

QAN Details

· Domestic market pressure: Qantas Airways Limited (ASX: QAN) senior unsecured debt and backed senior unsecured bank credit facility ratings got upgraded by Moody to Baa2 from Baa3. As part of the action Moody's has also upgraded QAN' senior unsecured MTN program ratings to (P)Baa2 from (P)Baa3. The outlook on all ratings is stable. However, Moody would consider downgrading the ratings if QAN deviates from its financial framework or if debt to EBITDA exceeds 3.0x on a sustained basis. On the other hand, QAN has confirmed that it expects to report a full-year Underlying Profit before Tax in the range of $1.35 billion to $1.40 billion. Moreover, in the third quarter, QAN has reported 1.4% fall in the group revenue to $3.96 billion and the Group Unit Revenue declined 1.8%. In the third quarter, there is 4.6% growth in the Group Domestic Unit Revenue as compared to the prior corresponding period. The Group Domestic capacity fell 3.7% majorly from the resource sector whose capacity fell 19%. The International market has recovered slightly from the tough conditions, however the downward trend in Group International Unit Revenue is moderating due to the slow capacity growth in the broader market. In the third quarter, there is fall of 5.6% in Unit Revenue year-on-year and there is 2.2% growth in the Group International capacity. Despite an increase in the capacity of Qantas International by 4.8 per cent, this is rise is capped by the impact of previously announced routes servicing the growing Asian market. The capacity of Jetstar International fell by 1.8 per cent. The decline in Unit Revenue for Group International is expected to continue to moderate in the fourth quarter, due to the fall in the competitor capacity growth to around 5 per cent for the second half from the elevated levels experienced in the first half of financial year 2017. In addition, as at 1st May 2017 the fall in bond yields from 31st December 2016 would have an adverse non-cash impact on the estimated full year Underlying Profit Before Tax of $25 million. We believe investors could book profits in the stock as it has already generated 53.7% returns in the last six months as on July 17th, 2017. Accordingly, we give an “Expensive” recommendation on this 2.6% dividend yield stock at the current price of $5.49

QAN Daily chart; (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...