Village Roadshow Ltd

.png)

VRL Details

Agreement with Topgolf: Village Roadshow Ltd (ASX: VRL) has signed letter of intent with Topgolf to acquire the exclusive rights to bring the sports entertainment to Australia. Topgolf expects 13 million guests in calendar year 2016 and 17 million in 2017.

VRL reported a 12.6% jump in EBITDA to $77.9 million for the half of FY16 while there was a net loss of $3.5 million for the period given the one-off material loss of $25.5 million. VRL stock has fallen 30.3% (as of June 30, 2016) in six months opening a lucrative entry opportunity to investors. The company has a good dividend yield with 100% franking. We maintain our “Buy” on the stock at the current price of $5.27

VRL Daily Chart (Source: Thomson Reuters)

Ardent Leisure Group

.png)

AAD Details

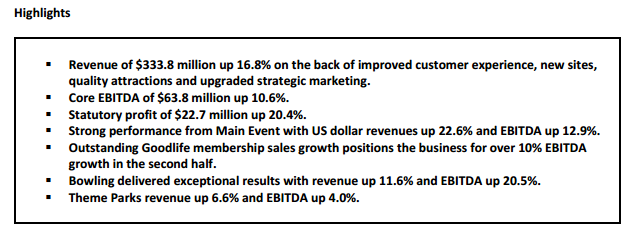

Sale process of the d’Albora Marinas: Ardent Leisure Group (ASX: AAD) rose 3.7% on July 01, 2016 and was trading ex-dividend on June 29, 2016. AAD delayed its sale process of the d’Albora Marinas which would not take place until certain capital improvements are made by the group. On the other hand, the group is focusing on its core Main event business, and forecasts over 27 centers by end of FY16, which is a 35% increase against fiscal year of 2015.

First Half Performance (Source: Company Reports)

With 24.7 conversion program for health clubs business, the group’s membership rose to over 8,300 members (for the entire first half of 2016). The group is targeting to tap further opportunity from Asia via Dreamworld. The stock has a good dividend yield and we give a “Buy” on the stock at the current price of $1.95

AAD Daily Chart (Source: Thomson Reuters)

Bellamy’s Australia Ltd

.png)

BAL Details

Leveraging China opportunity: Bellamy's Australia Ltd (ASX: BAL) is now producing at Fonterra which would increase the volume substantially by first quarter FY17 in view of the recently signed five-year agreement. Meanwhile, BAL has boosted its management team by appointing Andrew Cohen and Katherine Henry while its non-executive director has retired.

.png)

Multiple distribution channels (Source: Company Reports)

BAL is positioning itself to leverage huge China opportunity, despite the country’s recent regulations on infant formula makers. Accordingly, the group is expanding its distribution via retailers and online platforms. We maintain our “Speculative Buy” on the stock at the current price of $10.18

BAL Daily Chart (Source: Thomson Reuters)

G8 Education Ltd

.png)

GEM Details

Expanding through acquisition of centers: G8 Education Ltd (ASX: GEM) is on track to reach its objective of double digit growth in EPS for CY16, refinancing SGD$260m unsecured notes, and expansion of its acquisitions. The company recently updated about redemption of Series 001 Notes with replacement with Series 003 Notes which have been completely hedged by way of an interest rate swap.

.png)

Like for Like EBIT (Source: Company Reports)

Meanwhile, GEM declared a dividend of amount AUD 0.06 with a pay date of July 08, 2016. GEM stock has a strong dividend yield and is trading at a reasonable P/E. Accordingly, we maintain our “Buy” recommendation on the stock at the current price of $3.83

GEM Daily Chart (Source: Thomson Reuters)

Automotive Holdings Group Ltd

.png)

AHG Details

Expanding Portfolio via acquisitions: Automotive Holdings Group Ltd (ASX: AHG) is inking the city Mazda dealership in South Melbourne for a total consideration of $24.4million and the deal is expected to settle in July. In addition, AHG is acquiring Lance Dixon group of dealerships of JLR at Doncaster in Melbourne’s inner suburbs, as well as acquired Hyundai dealership at Penrith. On the other hand, the group is selling its Duncan Nissan business in Perth Victoria Park to enter into luxury vehicle segment in Victoria.

Moreover, AHG has completed the acquisition of Victorian Mitsubishi dealership at Wantirna South in Melbourne’s eastern suburbs. The company has good dividend yield and is trading at reasonable P/E, while the rebalancing of its portfolio would increase the margins. We maintain our “Buy” recommendation on the stock at the current price of $3.83

.PNG)

AHG Daily Chart (Source: Thomson Reuters)

Sirtex Medical Ltd

.png)

SRX Details

Solid American opportunity: Sirtex Medical Limited (ASX: SRX) continues to expect strong America’s dose sales growth in the range of 18-20% for the second half FY 16. But management expects lower dose sales performance in the EMEA and APAC regions during the second half. Moreover, Sirtex has revised the full year dose sales growth guidance at 15-17% as compared to the pcp versus previous guidance of 19.7%. As a result, SRX stock has fallen 36.11% (as of June 30, 2016) in the last six months. Meanwhile, SRX product SIR-Spheres Y-90 resin microspheres product has penetrated only 2% of the addressable market indicating a solid further upside potential. SIRveNIB Clinical Study has also been said to complete patient recruitment. In addition, Health Canada has granted the Medical Device Licence (MDL) for SIR-Spheres Y-90 resin microspheres.

UK National Institute for Health and Care Excellence (NICE), NHS doctors and commissioners also intend to consider SIR-Spheres Y-90 resin microspheres as an alternative to standard therapy with trans-arterial chemoembolization or sorafenib in the treatment of patients with inoperable primary liver cancer (hepatocellular carcinoma). We maintain our “Buy” recommendation on the stock at the current price of $26.31

SRX Daily Chart (Source: Thomson Reuters)

Xero Ltd

.png)

XRO Details

Boosting cash position: Xero Ltd (ASX: XRO) has been boosting its cash position with the cash usage from its operating and investing activities (including FX) reaching $86.1 million for FY16 against $88.2 million of previous year. XRO expects cash usage in FY 17 (based on FX rates at April 01, 2016) to reduce from FY16. Xero is managing to break even its cash flow within its current cash balance and improving at the operating level through automation and economies of scale.

Meanwhile, XRO has crossed $250m ACMR by adding $99m ACMR and 242k subscribers in FY16. In addition, FY16 operating revenue witnessed a growth of 67% and exceeded the subscriber growth of 51%. The company has recently released its disclosure statement relating to the giving of financial assistance to restricted share plan of the company. We maintain our “Buy” recommendation on the stock at the current price of $17.11

XRO Daily Chart (Source: Thomson Reuters)

Nearmap Ltd

.png)

NEA Details

Strong Contract wins: Nearmap Ltd (ASX: NEA) has signed a significant new one-year subscription contract with an existing customer of annual value of $1.1 million. In addition, NEA has entered a new partnership with OmniEarth to access a larger and more diverse range of customers in the US including water management, property management and insurance.

.png)

Subscription Revenue (source: Company Reports)

NEA has given key priorities for H2 FY16, which include accelerated growth in the Australian business through subscription revenue growth, customer addition and retention of existing customers and cost management, building the foundations in the US and enhancing the technology leadership. We remain bullish on the stock and maintain our “Buy” recommendation on the stock at the current price of $0.46

.PNG)

NEA Daily Chart (Source: Thomson Reuters)

Australia and New Zealand Banking Group Ltd

.png)

ANZ Details

Expanding Operational Efficiency: Australia and New Zealand Banking Group Ltd (ASX: ANZ) in the first half 2016 has reported 22% fall in statutory profit to $2.7 billion and accordingly the interim dividend is also down 7% to 80 cents per share. However, ANZ is streamlining and simplifying operations to make the bank ready for future which includes initiatives like strong expense management outcome, improving capital efficiency, restructuring and change to the application of accounting policy to accelerate software amortization.

ANZ also corrected over 6.11% (as of June 30, 2016) in the last four weeks due to fears of Brexit. However, the bank has high dividend yield and is trading at an attractive P/E and has better potential going forward. Despite short term pressure owing to Brexit, we maintain our “Buy” recommendation on the bank at the current price of $23.95

ANZ Daily Chart (Source: Thomson Reuters)

Amaysim Australia Ltd

.png)

AYS Details

Expanding subscriber base: Amaysim Australia Ltd (ASX: AYS) has surged 6.3% on July 01, 2016, and expects subscriber base to be in the range of 960,000 to 980,000 for FY16 and EBITDA to be in the range of $35m-36m including underlying Vaya contribution in 2HFY16 (excluding one-off transaction and integration costs related to Vaya acquisition).

.png)

ARPU performance (source: Company Reports)

The company is increasing its subscriber base every six months and the second half would see significant rise due to the addition of Vaya. AYS stock is added in S&P/ASX 300 index and we give a “Buy” recommendation on the stock at the current price of $1.775

.PNG)

AYS Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...