Nine Entertainment Co Holdings Limited

.png)

NEC Details

Refinancing of Corporate Debt Facilities: Nine Entertainment Co. Holdings Limited (ASX: NEC) is primarily engaged in broadcasting and program production throughout Free to Air television as well as metropolitan radio networks in Australia. The market capitalisation of the company stood at $3.27 Bn as on 31st January 2020. Recently, the company announced that it has inked binding agreements to refinance its existing corporate debt facilities. The company added that the new facilities would comprise three and four year revolving cash advance facilities amounting to $545 million. This facility also includes a 1 year $80 million working capital facility. It was also mentioned in the release that these new facilities replace the current facilities of $650 million, which will be expiring between February 2020 and February 2023. The company would also be releasing its 1H FY20 results on 26th February 2020. The following picture showcases growth in EBITDA from FY18 to FY19:

.png)

EBITDA Growth (Source: Company Reports)

What to Expect: The company mentioned that the Metro Free to Air business has achieved a leading revenue share of 39.8%, while the market witnessed a fall of 6.4% on last year. The company is anticipating the FTA market to experience a fall of mid-single digits throughout the full financial year 2020. As a result, FY20 pro forma group EBITDA is expected to witness low single-digit growth.

Valuation Methodology: EV/Sales Based Valuation

.png)

EV/Sales Based Valuation (Source: Thomson Reuters)

Note: All forecasted figures have been taken from Thomson Reuters, NTM: Next Twelve Months.

Stock Recommendation: On the back of its audience performance in CY19, the company is optimistic about share gain in Metro Free to Air business during the second half. We have valued the stock using EV/Sales based relative valuation approach, and for the purpose, we have taken peers such as Seven West Media Ltd (ASX: SVM), Gtn Ltd (ASX: GTN), QMS Media Ltd (ASX: QMS) etc., and arrived at a target price, which is offering an upside of lower double digit (in percentage terms). Therefore, in light of 10% growth in EBITDA, leading revenue share of 39.8% achieved by the Free to Air business, and valuation, we give a “Buy” recommendation on the stock at the current market price of $1.875 per share, down by 2.344% on 31st January 2020.

.jpg)

NEC Daily Technical Chart (Source: Thomson Reuters)

Pro Medicus Limited

.png)

PME Details

Signing of Contract by Subsidiary: Pro Medicus Limited (ASX: PME) is engaged in the development and supply of software and IT solutions to the public and private health sectors. The market capitalisation of the company stood at $2.48 Bn as on 31st January 2020. In the recent release, the company mentioned that Visage Imaging, Inc (US Subsidiary of PME) has inked a 5-year, multi-million-dollar contract with Nines, a Palo Alto-based company. The contract would provide an outcome in the form of base revenue of more than $6 million over the life of the contract with the potential for significant upside. The following picture provides an idea of EBIT margin expansion for the period covering FY14- FY19:

.png)

EBIT Margins (Source: Company Reports)

Outlook:During FY20, the company is expecting more opportunities because of improved prospects in North America as well as continued commercialisation and launch of new technology RIS platform namely, Visage RIS. The company is also anticipating a continuing improvement in operational results in FY20.

Stock Recommendation: Net margin for PME stood at 38.0% in FY19, up 8.6% on yoy, reflecting that the company has improved its position to convert its top-line into bottom-line. Current ratio of the company stood at 3.77x in FY19 with YoY growth of 8.4%. This reflects that the company possesses a decent liquidity position. The stock of PME has provided returns of 99.07% in one year and 7.18% on YTD basis. Thus, considering the improvement in net margin, returns in the past period, signing of a contract by subsidiary company, and decent outlook, we give a “Buy” recommendation on the stock at the current market price of $24.000 per share, up 0.46% on 31st January 2020.

.jpg)

PME Daily Technical Chart (Source: Thomson Reuters)

Appen Limited

.png)

APX Details

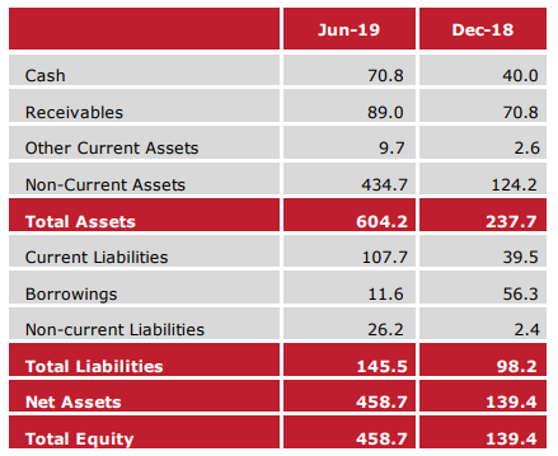

APX Revises Earnings Guidance: Appen Limited (ASX: APX) is involved in the provisioning of quality data solutions as well as services for machine learning and artificial intelligence applications for auto manufacturers, global technology companies and government agencies. The company recently announced that it would be releasing its results for the full year ended 31st December 2019 on 25th February 2020. On the financial front, the company experienced a rise in receivables to $89 million in June 2019 from $70.8 million in Dec 18. This rise has been driven by an increase in revenue volumes as well as the acquisition of Figure Eight.

Financial Metrics (Source: Company Reports)

Guidance for FY19:For the year ended 31st December 2019, the company is expecting underlying EBITDA in the ambit of $96Mn to $99Mn as compared to the previous guidance of $85Mn - $90Mn. This increase in earnings guidance has been generated by the rise in monthly relevance revenues and margins, primarily from existing projects with existing customers. The company is anticipating ARR (Annual Recurring Revenue) in the vicinity of $30Mn - $35Mn.

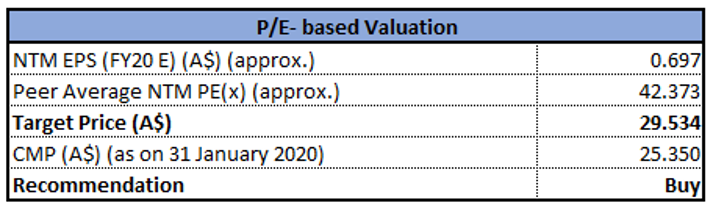

Valuation Methodology: P/E Multiple Multiple Approach

P/E Based Valuation (Source: Thomson Reuters)

Note: All forecasted figures have been taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation:During 1HFY19, the existing customers of the company supported revenue growth with repeat buying for existing and new projects. The company also experienced strong customer relationship because of high-quality data and service. We have valued the stock using P/E based relative valuation method and for the purpose, we have taken peers such as WiseTech Global Ltd (ASX: WTC), Link Administration Holdings Ltd (ASX: LNK), Iress Ltd (ASX: IRS), etc., and arrived at a target price with an upside of lower-double digit (in % terms). Hence, considering a robust balance sheet in 1HFY19, the rise in cash balance by $39.9 million, and increase in earnings guidance, we give a “Buy” recommendation on the stock at the current market price of $25.350 per share, down 0.158% on 31st January 2020.

APX Daily Technical Chart (Source: Thomson Reuters)

National Australia Bank Limited

NAB Details

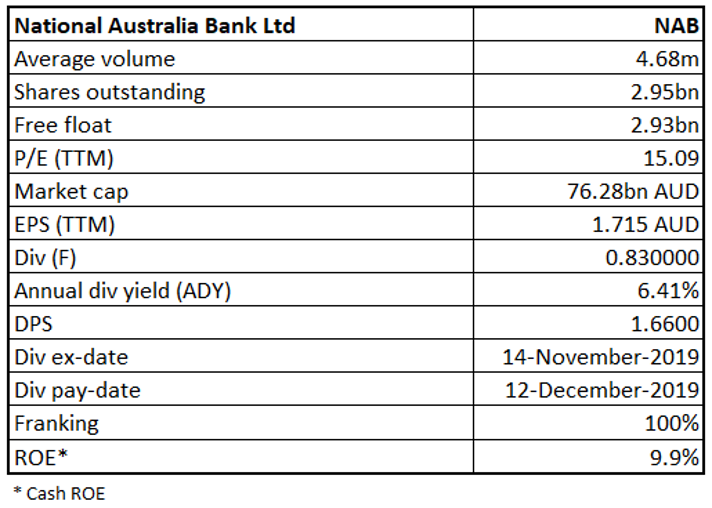

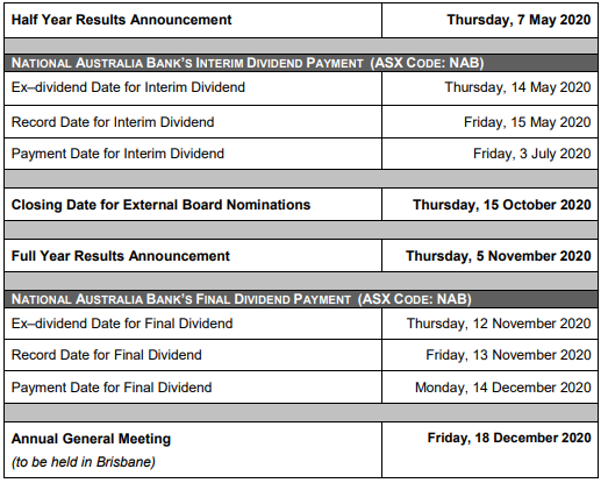

Resignation of Assistant Company Secretary:National Australia Bank Limited (ASX: NAB) is a well-known bank in Australia, which provides banking, financial and related services. The market capitalisation of the bank stood at $76.28 Bn as on 31st January 2020. The bank through a release announced that Kelly Patterson has stepped down from the role of assistant company secretary of National Australia Bank Limited (NAB), which came into effect on 28th January 2020. On 13th February 2020, the bank would be releasing its trading update for Q1 FY20. The following picture depicts an overview of key dates for the 2020 financial calendar.

2020 Financial Calendar (Source: Company Reports)

Forecast of Continuous Growth: As per the key personnel of the bank, the fundamentals for the Australian and New Zealand economies is sound mainly in Australia, with 28 years of continuous growth. The bank continues to strengthen its technology environment for delivering better experiences.

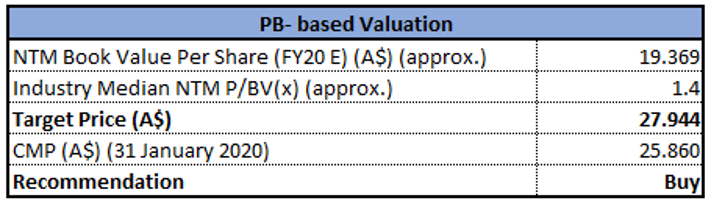

Valuation Methodology: P/B Multiple Approach

P/B Based Valuation (Source: Thomson Reuters)

Note: All forecasted figures have been taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: During FY19, the bank has improved its financial settings as well as its capital position. Moreover, it currently stands above the strong capital requirement for January 2020 by APRA (Australian Prudential Regulation Authority). We have valued the stock using P/B based relative valuation approach and arrived at a target price, which is offering an upside of high single-digit (in percentage terms). Thus, considering the decent valuation and strong capital position, we give a “Buy” recommendation on the stock at the current market price of $25.860 per share, down 0.077% on 31st January 2020.

NAB Daily Technical Chart (Source: Thomson Reuters)

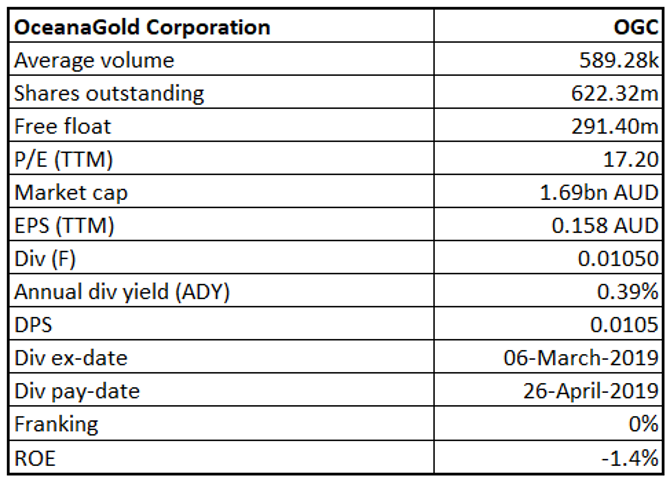

OceanaGold Corporation

OGC Details

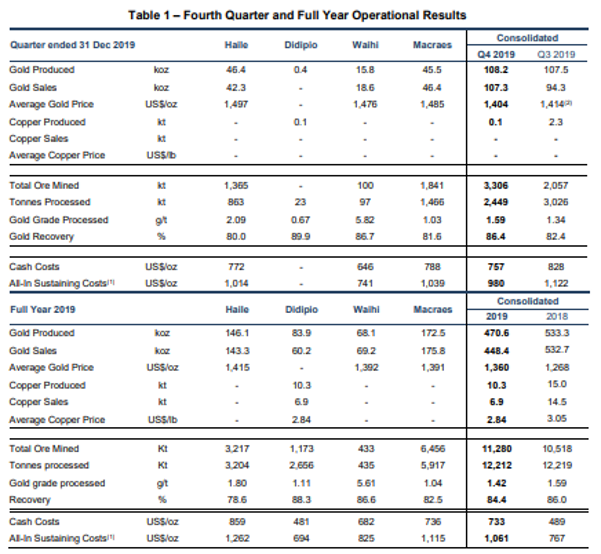

A Look at Operational Results for Q4 FY19: OceanaGold Corporation (ASX: OGC) is a gold mining company having operations in the Philippines, New Zealand and the USA. The market capitalisation of the company stood at $1.69 Bn as on 31st January 2020. The company would be releasing its 2019 audited financial and operational results on 20th February 2020. The company stated that the full year 2019 All-In Sustaining Costs stood at $1,061/oz, which includes $980/oz for Q4 FY19, against 2019 revised AISC guidance range of $1,040 to $1,090 per ounce sold. Moreover, the company has achieved a total recordable injury frequency rate of 3.6 per million hours worked in 2019, when compared to 4.5 per million hours worked in 2018.

Full Year Operational Results (Source: Company Reports)

Forecast for Gold Production:The company is expecting to produce around 12,000 ounces of gold in Q1 FY20 with an additional 8,000 ounces in the Q4 FY20, from the Waihi operations. The company also added that Waihi district study is currently in progress and is anticipated to wrap up in 1H FY20.

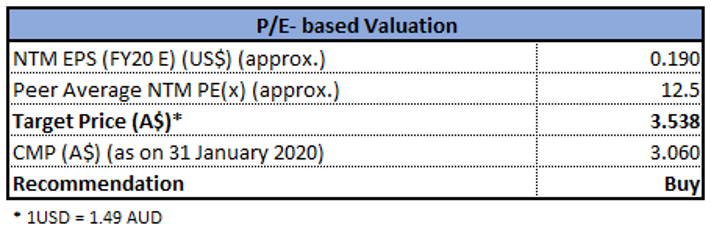

Valuation Methodology: P/E Multiple Approach

P/E Based Valuation (Source: Thomson Reuters)

Note: All forecasted figures have been taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: Cash costs for full-year 2019 stood at $733 per ounce sold, which included $757 per ounce sold in Q4FY19.We have valued the stock using P/E based relative valuation approach and for the purpose, we have taken peers such as Northern Star Resources Ltd (ASX: NST), Evolution Mining Ltd (ASX: EVN), Regis Resources Ltd(ASX: RRL), etc., and arrived at a target price, which is offering an upside of lower-double digit (in percentage terms). Also, the company has experienced a rise of around 26% in gold production from the Haile operations during Q4 FY19. Hence, considering the aforesaid facts, together with a decent outlook, we give a “Buy” recommendation on the stock at the current market price of $3.060 per share, up 12.915% on 31st January 2020, taking cues from the release of 4th quarter operational results.

OGC Daily Technical Chart (Source: Thomson Reuters)

Hub24 Limited

HUB Details

Significant Increase in FUA: Hub24 Limited (ASX: HUB) provides investment and superannuation portfolio administration services, licensee services to financial advisers. The company also provides software license and IT consulting services. The company has recently announced that it will release its interim results for FY20 on 25th February 2020. The company has recently released its quarterly report for December 2019 wherein it stated that net inflows witnessed an increase of 67% on pcp and stood at $1,259 million. In the same time span, Funds Under Administration came in at $15.8 billion, representing an increase of 58% on pcp.

.png)

Average Monthly Net Inflows and FUA (Source: Company Reports)

What to Expect: The company is well-positioned for growth and has upgraded its FUA guidance for FY21 and expects it to be in the range of $22 billion to $26 billion. The company will benefit from the market opportunity as it is expanding its distribution footprint nationally.

Valuation Methodology: EV/Sales Multiple Approach

.png)

EV/Sales based Valuation (Source: Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: As per ASX, the stock of HUB is trading close to its 52-week low of $9.890, offering a decent opportunity for accumulation. Over the last 4 years, the company witnessed a CAGR of ~35% in total revenue and a CAGR of ~65% in gross profit. During FY19, Return on Equity of the company was 11.7%, higher than the industry median of 6.2%. This indicates that the company is well deploying the capital of its shareholders and is capable of generating profits internally. Considering the trading levels, CAGR in revenue and gross profit, and decent growth opportunities, we have valued the stock using EV/Sales based relative valuation method and have arrived at a target upside of lower double-digit (in percentage terms). Hence, we recommend a “Buy” rating on the stock at the current market price of $10.960, up by 0.828% on 31 January 2020.

HUB Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...