Appen Limited

.png)

APX Details

APX Rides on Strong Organic Growth in FY19: Appen Limited (ASX: APX) is involved in the development of high-quality, human-annotated datasets for ML & AI. Recently, the company appointed Ms. Vanessa Liu as an independent non-executive director of the Company, effective from March 27, 2020.

FY19 Key Financial Highlights: During the year ended 31st December 2019, the company reported robust organic growth, which led to a substantial rise in revenue. Revenue for the period stood at $536 million, up 47% on a year over year basis. On a constant currency basis, revenue increased 37% year over year. Underlying EBITDA increased 42% and came in at $101 million in FY19 (up 31% on constant currency basis). Organic revenue for FY19 increased 37% year over year and came in at $498.1 million. Underlying NPAT increased 32% year over year in FY19. During the year, dividend amounted to 5 cents per share, up 25% year over year (50% franked).

.png)

Key Financial Highlights (Source: Company Reports)

What to Expect: APX is likely to boost its customer base via investments in sales and marketing, which, in turn, will result in softer margins in 1HFY20. The company expects underlying EBITDA for FY20 to be in the ambit of $125 million - $130 million, given the exchange rate of 1 AUD = 0.70 USD from Feb’20 – Dec’20.

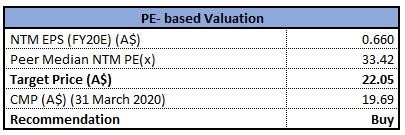

Valuation Methodology: P/E Based Relative Valuation

P/E Based Valuation (Source: Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM- Next Twelve Months

Stock Recommendation: The stock of the company gave negative returns of 4.54% over a period of six months and is currently trading below the average of its 52-week trading range of $15.7 - $32.00. The company’s China operations are growing fast with rapid pipeline expansion and the team in place. The China operations are young with modest targets, thus Appen anticipates almost negligible impact from COVID-19 outbreak on FY20 group revenue and earnings. We have valued the stock using P/E based relative valuation method and for the purpose, have taken the peer group - Infomedia Ltd (ASX: IFM), TechnologyOne Ltd (ASX: TNE) and WiseTech Global Ltd (ASX: WTC). We have arrived at a target price with an upside of lower double-digit (in percentage terms). Hence, we give a “Buy” recommendation on the stock at the current market price of $19.69, down 2.525% on 31 March 2020.

.jpg)

APX Daily Technical Chart (Source: Thomson)

Nine Entertainment Co. Holdings Limited

.png)

NEC Details

Trading Update on COVID-19 Impact: Nine Entertainment Co. Holdings Limited (ASX: NEC) is a media and entertainment company with a market capitalisation of $1.79 Bn as on 31 March 2020. Recently, the company updated the market about its necessary steps to curb the spread of COVID-19. In doing so, the company withdrew its FY20 guidance, due to the rising uncertainty owing to coronavirus outbreak. Moreover, the company remains focused on major short and long-term cost initiatives across all its businesses. The table below mostly highlights NEC’s initiatives, taken due to the global crisis for FY20.

.png)

Cost Initiatives(Source: Company Reports)

Balance Sheet Details: The company recently completed the refinancing of its corporate debt facilities. The new facilities comprise evolving cash advance facilities of $545 million over a period of 3 and 4 years, along with $80 million working capital facility for a time period of 1 year. Currently, NEC retains undrawn debt and cash of ~$300 Million.

1HFY20 Key Highlights: During the period, the company reported revenue of $1.2 Bn with EBITDA of ~$251 million, and a net profit after tax of ~$114 million on a statutory basis, pre-Specific Items. The company declared an interim dividend of 5.0 cents, fully franked.

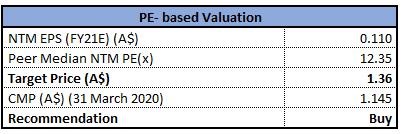

Valuation Methodology: P/E Multiple Based Relative Valuation

P/E Based Valuation (Source: Thomson Reuters)

Note: All forecasted figures have been taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: The stock of the company gave negative returns of 46.56% over a period of six months and is currently trading below the average of its 52-week trading range of $0.815 - $2.130. We have valued the stock using P/E based relative valuation method and arrived at a target price with an upside of lower double-digit (in percentage terms). For the purpose, we have taken the peer group - HT&E Ltd (ASX: HT1), TPG Telecom Ltd (ASX: TPM) and Vocus Group Ltd (ASX: VOC), to name few. Hence, considering the growth prospects, and current trading levels, we give a “Buy” recommendation on the stock at the current market price of $1.145 per share, up by 9.048% on 31 March 2020.

.jpg)

NEC Daily Technical Chart (Source: Thomson)

Challenger Limited

.png)

CGF Details

CGF Maintains its FY20 Normalised Profit Outlook:Challenger Limited (ASX: CGF) is a multi-faceted financial services company, with its primary businesses in funds management, annuities, and administration platforms. Recently, the company stated with reference to Challenger Capital Notes, that CGF will issue unsecured convertible notes worth $345 million. Asper the terms of Challenger Capital Notes, CGF may elect to convert, redeem or resell the Notes on the Optional Exchange Date, which is 25 May 2020.

Capital Position & Investment Portfolio Update: On 30 March 2020, the company stated that it will continue to maintain its normalised profit guidance for FY20, notwithstanding the substantial volatility in investment market, owing to the Coronavirus pandemic. CGF has strong financial flexibility and liquidity position, which incorporates $400 million of banking facility, which has been fully drawn and is being held in cash outside of Challenger Life.

Other Recent Update: In a recent update, the company announced that UBS Group AG and its related bodies corporate, a substantial holder of the company, has increased its voting power from 5.19% to 6.84%.

Strong Net Inflows and FUM Growth in 1HFY20: The company in its half-year ended 31 December 2019 results, reported an increase of ~10% in assets under management to $86 billion and a growth of around 3% in normalised profit before tax to $279 million.

.png)

AUM and NPBT (Source: Company Reports)

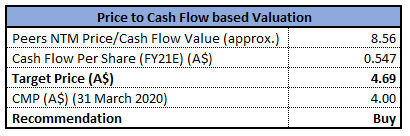

Valuation Methodology: P/CF Multiple Based Relative Valuation

P/CF Based Valuation (Source: Thomson Reuters)

Note: All forecasted figures have been taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: The stock of the company gave negative returns of 43.46% over a period of six months and is currently trading below the average of its 52-week trading range of $2.820 - $10.43. The company has proven to be robust despite the challenges in the operating environment and has the appropriate strategy to deliver long term growth. We have valued the stock using P/CF based relative valuation method and arrived at a target price with an upside of lower double-digit (in percentage terms). For the purpose, we have taken the peer group - Navigator Global Investments Ltd (ASX: NGI), Magellan Financial Group Ltd (ASX: MFG) and IOOF Holdings Ltd (ASX: IFL), to name few. Hence, we give a “Buy” recommendation on the stock at the current market price of $4.00 per share, down by 0.498% on 31 March 2020.

CGF Daily Technical Chart (Source: Thomson)

Reliance Worldwide Corporation Limited

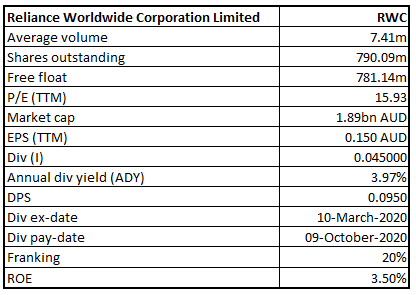

RWC Details

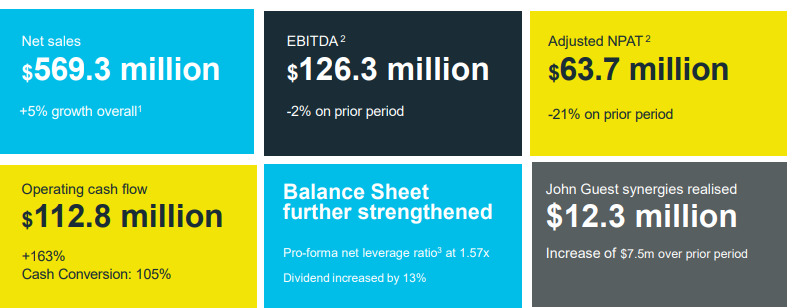

Trading and Operational Update: Reliance Worldwide Corporation Limited (ASX: RWC) is engaged in the manufacturing, designing, & supply of water flow and control products and solutions for the plumbing industry. Recently, the company provided a trading and operations update, which incorporates coronavirus impact.RWC’s sales for the month of January and February 2020 stood in-line with the expectation. In the USA, UK & Australia, the company’s manufacturing facilities and distribution centres remained fully supervised and operational. RWC continues to have substantial funding lines available in order to aid its working capital as well as cash flow needs. The company further added that all non-essential capital expenditure has been suspended to boost cash flow during the time of global uncertainty from COVID-19.

FY20 Guidance: Considering the rising uncertainty on coronavirus outbreak,RWC has suspended its guidance for FY20, which include adjusted net profit after tax range of $140 million to $150 million.

1HFY20 Key Highlights: During the period, the company reported net sales of $569.3 million with EBITDA of ~$126.3 million, and adjusted net profit after tax of ~$63.7 million. Operating cash flow for the period stood at $112.8 million, up 163% year over year.

Key Highlights(Source: Company Reports)

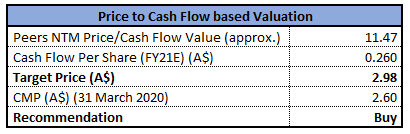

Valuation Methodology: P/CF Multiple Based Relative Valuation

P/CF Based Valuation (Source: Thomson Reuters)

Note: All forecasted figures have been taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: The stock of the company gave negative returns of 40.25% over a period of six months and is currently trading below the average of its 52-week trading range of $1.63 - $5.1. The market capitalisation of the company stood at $1.89 billion as on 31 March 2020. We have valued the stock using P/CF multiple based relative valuation method, and for the purpose, we have taken peers such as James Hardie Industries PLC (ASX: JHX), GWA Group Ltd (ASX: GWA), GUD Holdings Ltd (ASX: GUD) and arrived at a target price, which is offering an upside of lower double-digit (in percentage terms). Hence, considering sales performance in January and February 2020, strong orders, and current trading levels, we give a “Buy” recommendation on the stock at the current market price of $2.60 per share, up by 8.787% on 31 March 2020.

RWC Daily Technical Chart (Source: Thomson)

Westpac Banking Corporation

WBC Details

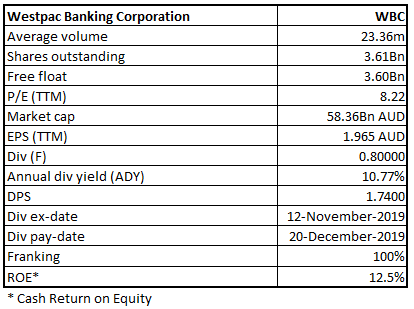

WBC to Aid ABA Business Support PackageAmid Covid-19: Westpac Banking Corporation (ASX: WBC) is engaged in providing financial services including lending, deposit taking, general finance, etc. The bank has recently declared a dividend of $0.6852 per security on Vanguard Australian Shares Index ETF (VAS) which is to be paid on 20 April 2020. In another update, the company declared dividend of $0.4724 per security, payable on 14 April 2020.

COVID-19 Update: On 30 March 2020, the company stated that it will support the Australian Banking Association’s (ABA) extended Business Support Package due to COVID-19 pandemic. In doing so, WBC expanded Business Relief Package, to suspend principal and interest repayments of authorised business loans for a period of six months, with a total lending coverage amounting to a maximum $10 million. The company alsopermitted theaccess to term deposit funds without decreasing the interest rate.

1QFY20 Capital Funding & Credit Quality Update: The bank has recently released its capital, funding and credit quality report, wherein it reported a sound credit quality with an increase of 1.7% in total provision balances. WBC also reported a common equity tier 1 capital ratio 10.8% and Level 1 common equity Tier 1 capital ratio 11.1%.

.png)

Capital Ratios (Source: Company Reports)

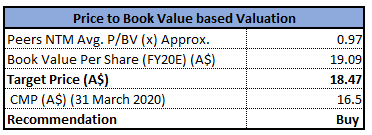

Valuation Methodology: Price to Book Based Relative Valuation

Price to Book Multiple Based Approach (Source: Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: As per ASX, the stock of WBC is trading close to its 52-week low level of $13.470, proffering a decent opportunity to enter the market. As on 31 March 2020, the market capitalization of the bank stood at $58.36 billion. While WBC may face some uncertainties in the near-term owing to global pandemic of COVID-19, medium to long-term outlook for the bank is promising due to its size and strength of its balance sheet, quality and scale of customers and financial resources. Considering the current trading levels, we have valued the stock using price to book multiple based relative valuation method and arrived at a target upside of lower double-digit (in percentage terms). For the purpose, we have taken peers such as Commonwealth Bank of Australia (ASX: CBA), National Australia Bank Ltd (ASX: NAB), Bendigo and Adelaide Bank Ltd (ASX: BEN) Hence, we recommend a “Buy” rating on the stock at the current market price of $16.5, up by 2.104% on 31 March 2020.

WBC Daily Technical Chart (Source: Thomson)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...